You might also like

- Bankers Acceptance CondensedDocument5 pagesBankers Acceptance CondensedLuka Ajvar100% (1)

- 12408original Issue Discount (OID) DefinedDocument13 pages12408original Issue Discount (OID) DefinedTheplaymaker508100% (1)

- I F A U: Nstructions or N NsecuredDocument4 pagesI F A U: Nstructions or N NsecuredLeslie Barnes100% (1)

- Bankers AcceptancesDocument36 pagesBankers AcceptancesAlexhCreditorNo ratings yet

- The Negotiable Instruments LawDocument18 pagesThe Negotiable Instruments Lawcode4sale100% (1)

- The Birth Certificate InfoDocument1 pageThe Birth Certificate InfoexousiallcNo ratings yet

- Bankers AcceptanceDocument1 pageBankers AcceptanceVarad LaghateNo ratings yet

- LOAN Defined: Deposit of Money "Promissory Note" by Customer W/ BankerDocument8 pagesLOAN Defined: Deposit of Money "Promissory Note" by Customer W/ Bankerin1orNo ratings yet

- Bill of ExchangeDocument4 pagesBill of ExchangeChetan SapraNo ratings yet

- Treasury management functions and capital vs money marketsDocument8 pagesTreasury management functions and capital vs money marketsMichelle T100% (1)

- 31 Usc 5312 We Are A Financial InstitutionDocument3 pages31 Usc 5312 We Are A Financial InstitutionMichael Focia100% (1)

- Loan Accounting Reveals True Creditor PDFDocument1 pageLoan Accounting Reveals True Creditor PDFDouglas StehlingNo ratings yet

- Holy Smoke, My Promissory Note's A Security!Document2 pagesHoly Smoke, My Promissory Note's A Security!johngault100% (2)

- Preauthorzed Letter of CreditDocument1 pagePreauthorzed Letter of Creditlakeshia1lovinglife10% (1)

- EFT ScamDocument1 pageEFT ScamTonya Banks0% (1)

- Bill of ExchangeDocument3 pagesBill of ExchangeNisot Ihdnag100% (5)

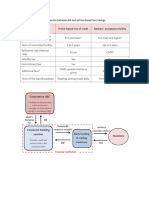

- Our Commercial Flow Chart Rev2Document1 pageOur Commercial Flow Chart Rev2Dark Heineken100% (1)

- (1874) The Currency-Specie PaymentsDocument40 pages(1874) The Currency-Specie PaymentsHerbert Hillary Booker 2nd50% (2)

- New Pacific Timber vs SenerisDocument13 pagesNew Pacific Timber vs SenerisiicaiiNo ratings yet

- Notice of DishonorDocument3 pagesNotice of Dishonorbill100% (2)

- Trust May 2011 NotesDocument3 pagesTrust May 2011 Notespaula_morrill1778No ratings yet

- US Internal Revenue Service: p1212 - 1997Document15 pagesUS Internal Revenue Service: p1212 - 1997IRSNo ratings yet

- Bailor and Bailee Relationship PDFDocument16 pagesBailor and Bailee Relationship PDFJohnnyLarson100% (1)

- Bank Draw Down Request 1031 Fedwire Definition Info The DifferenceDocument2 pagesBank Draw Down Request 1031 Fedwire Definition Info The DifferenceMikeDouglas0% (1)

- SAR Page 3 TextDocument1 pageSAR Page 3 TextMikeDouglasNo ratings yet

- 2nd LTR To LenderDocument1 page2nd LTR To LenderBob WrightNo ratings yet

- LegForms Group 4Document25 pagesLegForms Group 4SmurfNo ratings yet

- 3 Day Notice To ReportDocument1 page3 Day Notice To ReportMarsha MainesNo ratings yet

- Lawful Money Defined: What It Is and How It Differs From Fiat CurrencyDocument4 pagesLawful Money Defined: What It Is and How It Differs From Fiat CurrencyLedoNo ratings yet

- Bankers AcceptanceDocument2 pagesBankers AcceptanceKudzanai Allen Paraffin100% (5)

- Oracle Receivables Automatic Receipts and Remittance GuideDocument29 pagesOracle Receivables Automatic Receipts and Remittance GuideShagun PanjwaniNo ratings yet

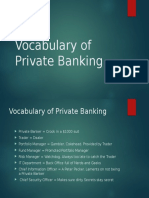

- Private BankingDocument2 pagesPrivate BankingAnwar Ludin0% (1)

- 7 Points For An AffidavitDocument1 page7 Points For An AffidavitmoNo ratings yet

- Living Trust Funding Worksheet - MarriedDocument14 pagesLiving Trust Funding Worksheet - MarriedRocketLawyerNo ratings yet

- IndorsementDocument1 pageIndorsementJason HenryNo ratings yet

- Private BankerDocument2 pagesPrivate Bankerapi-772861790% (1)

- Freedom Papers Section 2Document47 pagesFreedom Papers Section 2John Downs100% (5)

- TrustDocument30 pagesTrustWho moved my Cheese?100% (2)

- Bill of exchange, promissory note and cheque regulationsDocument10 pagesBill of exchange, promissory note and cheque regulationsThéotime HabinezaNo ratings yet

- Bill of Exchange and ChecksDocument8 pagesBill of Exchange and ChecksSmurf82% (17)

- Public Vs PrivateDocument1 pagePublic Vs PrivateYaw Mensah Amun RaNo ratings yet

- Banker NotesDocument134 pagesBanker NotesEdward MokweriNo ratings yet

- 3 Levels of CreditorDocument1 page3 Levels of CreditorSheldon Jungle100% (3)

- $$$$ Collect Your Own Attorney Fees$$$ - What A Private Attorney General Is AND Why It Matters.Document48 pages$$$$ Collect Your Own Attorney Fees$$$ - What A Private Attorney General Is AND Why It Matters.83jjmackNo ratings yet

- Structured Adjustable Rate Mortgage Loan Trust Mortgage Pass-Through Certificates, Series 2004-19 December 26, 2012Document33 pagesStructured Adjustable Rate Mortgage Loan Trust Mortgage Pass-Through Certificates, Series 2004-19 December 26, 2012Himanshu KhannaNo ratings yet

- 2018 Sav1455 RedemptionDocument5 pages2018 Sav1455 Redemptiondouglas jonesNo ratings yet

- How the word BIBLE relates to banking instruments, laws and equityDocument1 pageHow the word BIBLE relates to banking instruments, laws and equityKurozato CandyNo ratings yet

- Edwin Vieira, Jr. - What Is A Dollar - An Historical Analysis of The Fundamental Question in Monetary Policy PDFDocument33 pagesEdwin Vieira, Jr. - What Is A Dollar - An Historical Analysis of The Fundamental Question in Monetary Policy PDFgkeraunenNo ratings yet

- Intellectual Property Securitization: Intellectual Property SecuritiesFrom EverandIntellectual Property Securitization: Intellectual Property SecuritiesNo ratings yet

- The Feasts of Yahuah 2022Document1 pageThe Feasts of Yahuah 2022Mercury2012No ratings yet

- Discounting PDFDocument1 pageDiscounting PDFMercury2012No ratings yet

- Acts of Congress Cited by Popular NameDocument318 pagesActs of Congress Cited by Popular NameMercury2012No ratings yet

- UntitledDocument59 pagesUntitledMercury2012No ratings yet

- Discount PDFDocument1 pageDiscount PDFMercury2012No ratings yet

- Arbitrary Act or Decision PDFDocument1 pageArbitrary Act or Decision PDFMercury2012No ratings yet

- Three Elements of Jurisdiction for Valid Court RulingsDocument1 pageThree Elements of Jurisdiction for Valid Court RulingsMercury2012No ratings yet

- Money - A Fast Start PDFDocument1 pageMoney - A Fast Start PDFMercury2012No ratings yet

- Three Standards of Proof PDFDocument1 pageThree Standards of Proof PDFMercury2012No ratings yet

- Form 180.bias Invest - AllegationsDocument1 pageForm 180.bias Invest - AllegationsMercury2012No ratings yet

- Benefit Seeking PDFDocument1 pageBenefit Seeking PDFMercury2012No ratings yet

- 3 Month Training ProgramDocument8 pages3 Month Training ProgramMercury2012No ratings yet

- BreachDocument1 pageBreachMercury2012No ratings yet

- Bank Credit - Credits and Collections PDFDocument1 pageBank Credit - Credits and Collections PDFMercury2012No ratings yet

- Form 081.illegal Warrantless Search - Allegations PDFDocument1 pageForm 081.illegal Warrantless Search - Allegations PDFMercury2012No ratings yet

- Framing The Deep Issue FormulaDocument1 pageFraming The Deep Issue FormulaMercury2012No ratings yet

- The Negro Law of South Carolina (1848)Document68 pagesThe Negro Law of South Carolina (1848)Rlynne100% (7)

- Form 081.illegal Warrantless Search - Allegations PDFDocument1 pageForm 081.illegal Warrantless Search - Allegations PDFMercury2012No ratings yet

- Status, TimeDocument1 pageStatus, TimeMercury2012No ratings yet

- A Charge, Delivered To The African LodgeDocument17 pagesA Charge, Delivered To The African LodgeMercury2012No ratings yet

- City Org ModelDocument1 pageCity Org ModelMercury2012No ratings yet

- Speed of Movement PDFDocument1 pageSpeed of Movement PDFMercury2012No ratings yet

- Rights and Duties of Neutrals (1916)Document272 pagesRights and Duties of Neutrals (1916)Mercury2012No ratings yet

- Lifecycl PDFDocument1 pageLifecycl PDFMercury2012No ratings yet

- 3 Month Training ProgramDocument8 pages3 Month Training ProgramMercury2012No ratings yet

- 21 Points To Solve Commercial DisputeDocument4 pages21 Points To Solve Commercial DisputeMercury2012No ratings yet

- Developing The Theory of The CaseDocument1 pageDeveloping The Theory of The CaseMercury2012No ratings yet

- Overview of CDocument64 pagesOverview of CMercury2012No ratings yet

- Elements to Create a Binding ContractDocument1 pageElements to Create a Binding ContractMercury2012No ratings yet

- Overview of CDocument64 pagesOverview of CMercury2012No ratings yet

- Appendix 33 - PayrollDocument1 pageAppendix 33 - PayrollRogie Apolo67% (3)

- Private Program Opportunity - Procedure - From 25K An Up + Small Cap Flash - Jan 16, 2024Document6 pagesPrivate Program Opportunity - Procedure - From 25K An Up + Small Cap Flash - Jan 16, 2024Esteban Enrique Posan BalcazarNo ratings yet

- 6-Ratios Prop Indices LogsDocument4 pages6-Ratios Prop Indices LogsPushkar0% (1)

- 2 PDFDocument5 pages2 PDFSubrat SahooNo ratings yet

- Pepsi PaperDocument6 pagesPepsi Paperapi-241248438No ratings yet

- INTERMEDIATE ACCOUNTING-Unit01Document24 pagesINTERMEDIATE ACCOUNTING-Unit01Rattanaporn TechaprapasratNo ratings yet

- Banana Production (Lakatan) Project: A Business Plan of Ecleo FarmDocument20 pagesBanana Production (Lakatan) Project: A Business Plan of Ecleo Farmmarkgil1990No ratings yet

- Annual Report of The Secretary of WarDocument1,017 pagesAnnual Report of The Secretary of Warzandro antiolaNo ratings yet

- Top Law Firm in Dubai, UAE - RAALCDocument20 pagesTop Law Firm in Dubai, UAE - RAALCraalc uaeNo ratings yet

- MBA Financial Management AssignmentDocument4 pagesMBA Financial Management AssignmentRITU NANDAL 144No ratings yet

- Executive Order 1035 Streamlines Gov't Land AcquisitionDocument5 pagesExecutive Order 1035 Streamlines Gov't Land Acquisitionahsiri22No ratings yet

- CDP CDP Complaint-1Document20 pagesCDP CDP Complaint-1Scott JohnsonNo ratings yet

- LGU-NGAS TableofContentsVol1Document6 pagesLGU-NGAS TableofContentsVol1Pee-Jay Inigo UlitaNo ratings yet

- Income Statement Format (KTV) KTV KTVDocument30 pagesIncome Statement Format (KTV) KTV KTVDarlene Jade Butic VillanuevaNo ratings yet

- Introduction To Investment MGMTDocument6 pagesIntroduction To Investment MGMTShailendra AryaNo ratings yet

- 1 Partnership FormationDocument7 pages1 Partnership FormationJ MahinayNo ratings yet

- Accountancy and Auditing 2-2011Document7 pagesAccountancy and Auditing 2-2011Muhammad BilalNo ratings yet

- Travel Agency Business Plan: Adventure Excursions Unlimited Executive SummaryDocument33 pagesTravel Agency Business Plan: Adventure Excursions Unlimited Executive SummaryjatinNo ratings yet

- Saka 1h Presentation 2019 - 2 5d67a0eea24d1 PDFDocument18 pagesSaka 1h Presentation 2019 - 2 5d67a0eea24d1 PDFAnurag RayNo ratings yet

- Tempest Accounting and AnalysisDocument10 pagesTempest Accounting and AnalysisSIXIAN JIANGNo ratings yet

- North Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth ReformDocument84 pagesNorth Carolina Tax Reform Options: A Guide To Fair, Simple, Pro-Growth ReformTax Foundation100% (1)

- Banking Legal and Regulatory Aspects Janbi Model QuestionsDocument8 pagesBanking Legal and Regulatory Aspects Janbi Model QuestionsKhanal PremNo ratings yet

- Mahmood Textile MillsDocument33 pagesMahmood Textile MillsParas RawatNo ratings yet

- The Greatest Trade of The CenturyDocument280 pagesThe Greatest Trade of The Centurysalsa94No ratings yet

- CB Insights - Fintech Report Q1 2019 PDFDocument81 pagesCB Insights - Fintech Report Q1 2019 PDFsarveshrathiNo ratings yet

- Chapter 29 PDFDocument11 pagesChapter 29 PDFSangeetha Menon100% (1)

- Walmart's $16 Billion Acquisition of FlipkartDocument2 pagesWalmart's $16 Billion Acquisition of FlipkartAmit Dharak100% (1)

- 2 Forex Question CciDocument50 pages2 Forex Question CciRavneet KaurNo ratings yet

- Final Accounts Problems and Solutions - Final Accounts QuestionsDocument20 pagesFinal Accounts Problems and Solutions - Final Accounts QuestionshafizarameenfatimahNo ratings yet

- CSEC POB June 2016 P1 With AnswersDocument8 pagesCSEC POB June 2016 P1 With AnswersJAVY BUSINESSNo ratings yet