You might also like

- Leonila Rivera MGT9Document1 pageLeonila Rivera MGT9Asvag OndaNo ratings yet

- MA PresentationDocument6 pagesMA PresentationbarbaroNo ratings yet

- Installment SalesDocument6 pagesInstallment SalesMarivic C. VelascoNo ratings yet

- Cost 1 WeekDocument45 pagesCost 1 WeekMelissa Kayla Maniulit0% (1)

- Chap 8 Responsibility AccountingDocument51 pagesChap 8 Responsibility AccountingXel Joe BahianNo ratings yet

- Seatwork - Advacc1Document2 pagesSeatwork - Advacc1David DavidNo ratings yet

- Kaladkaren Corporation Bankruptcy Liquidation StatementsDocument51 pagesKaladkaren Corporation Bankruptcy Liquidation StatementsrenoNo ratings yet

- Use The Fact Pattern Below For The Next Three Independent CasesDocument5 pagesUse The Fact Pattern Below For The Next Three Independent CasesMichael Bongalonta0% (1)

- Practical Accounti ng2: Business CombinationsDocument9 pagesPractical Accounti ng2: Business CombinationsKath SapitanNo ratings yet

- C36 Planning-W RevisionsDocument23 pagesC36 Planning-W RevisionsNicole Johnson100% (1)

- Vdocuments - MX - Advanced Financial Accounting 1Document11 pagesVdocuments - MX - Advanced Financial Accounting 1Sweet EmmeNo ratings yet

- There May Be A Property Relationship of Conjugal PDocument6 pagesThere May Be A Property Relationship of Conjugal PJunho ChaNo ratings yet

- Chapter 16 - Bus Com Part 3 - Afar Part 2Document5 pagesChapter 16 - Bus Com Part 3 - Afar Part 2Emman ElagoNo ratings yet

- CMA2011 CatalogDocument5 pagesCMA2011 CatalogDaryl DizonNo ratings yet

- Sol Man - MC PTXDocument5 pagesSol Man - MC PTXiamjan_101No ratings yet

- Acctg 303Document9 pagesAcctg 303Anonymous IsEZYR1No ratings yet

- Business Combination.: Pfrs 3Document33 pagesBusiness Combination.: Pfrs 3Reginald Valencia100% (1)

- Module 7 NPO Colleges and Universities - Ngovacc PDFDocument8 pagesModule 7 NPO Colleges and Universities - Ngovacc PDFvum preeNo ratings yet

- PROBLEMSDocument19 pagesPROBLEMSlalalalaNo ratings yet

- TX10 - Other Percentage TaxDocument15 pagesTX10 - Other Percentage TaxKatzkie Montemayor GodinezNo ratings yet

- Supporting ComputationDocument5 pagesSupporting ComputationSuenNo ratings yet

- Ia3 IsDocument3 pagesIa3 IsMary Joy CabilNo ratings yet

- This Study Resource Was: Consignment SalesDocument3 pagesThis Study Resource Was: Consignment SalesKez MaxNo ratings yet

- Case Carolina-Wilderness-Outfitters-Case-Study PDFDocument8 pagesCase Carolina-Wilderness-Outfitters-Case-Study PDFMira miguelito50% (2)

- Comp 3Document28 pagesComp 3CristineJoyceMalubayIINo ratings yet

- 208 BDocument10 pages208 BXulian ChanNo ratings yet

- Intermediate Accounting 2 Quiz #3Document4 pagesIntermediate Accounting 2 Quiz #3Claire Magbunag AntidoNo ratings yet

- "How Well Am I Doing?" Statement of Cash Flows: Managerial Accounting, 9/eDocument51 pages"How Well Am I Doing?" Statement of Cash Flows: Managerial Accounting, 9/eMARY JUSTINE PAQUIBOTNo ratings yet

- 05 Activity 1 BALADocument3 pages05 Activity 1 BALAPola PolzNo ratings yet

- Essay on Activity-Based Costing for Ingersol DraperiesDocument13 pagesEssay on Activity-Based Costing for Ingersol DraperiesLhorene Hope DueñasNo ratings yet

- Instruction: Show Your Solution. No Solution Incorrect AnswerDocument1 pageInstruction: Show Your Solution. No Solution Incorrect AnswerRian ChiseiNo ratings yet

- Ais Chapter 15 Rea ModelDocument138 pagesAis Chapter 15 Rea ModelJanelleNo ratings yet

- Tina and KimDocument3 pagesTina and KimAngelli LamiqueNo ratings yet

- P3Document18 pagesP3Rezzan Joy MejiaNo ratings yet

- Central Plain University income tax calculationDocument3 pagesCentral Plain University income tax calculationLFGS Finals0% (1)

- CH 005Document2 pagesCH 005Joana TrinidadNo ratings yet

- MASDocument7 pagesMASHelen IlaganNo ratings yet

- Midterm Exam No. 2Document1 pageMidterm Exam No. 2Anie MartinezNo ratings yet

- Consolidating Balance SheetsDocument4 pagesConsolidating Balance Sheetsangel2199No ratings yet

- MODULE 4 Relevant CostingDocument9 pagesMODULE 4 Relevant Costingsharielles /No ratings yet

- Act13 Orquia-Anndhrea Bsa-32Document3 pagesAct13 Orquia-Anndhrea Bsa-32Clint RoblesNo ratings yet

- LiabilitiesDocument2 pagesLiabilitiesFrederick AbellaNo ratings yet

- Chapter 15-Financial Planning: Multiple ChoiceDocument22 pagesChapter 15-Financial Planning: Multiple ChoiceadssdasdsadNo ratings yet

- Cost To CostDocument1 pageCost To CostAnirban Roy ChowdhuryNo ratings yet

- REVIEW MATERIALS FOR TAX102: TRANSFER AND BUSINESS TAXATIONDocument17 pagesREVIEW MATERIALS FOR TAX102: TRANSFER AND BUSINESS TAXATIONElizah Faye AlcantaraNo ratings yet

- HOBA QuestionsDocument7 pagesHOBA QuestionsKristine CorporalNo ratings yet

- Defined Benefit Plan-Midnight CompanyDocument2 pagesDefined Benefit Plan-Midnight CompanyDyenNo ratings yet

- Intangible Assets SoftwareDocument3 pagesIntangible Assets SoftwareZerjo CantalejoNo ratings yet

- Management Accounting Multiple Choice ExamDocument12 pagesManagement Accounting Multiple Choice ExamMark Lord Morales Bumagat100% (1)

- Responsibility Accounting and Reporting: Multiple ChoiceDocument23 pagesResponsibility Accounting and Reporting: Multiple ChoiceARISNo ratings yet

- Acctg. QB 1-1Document8 pagesAcctg. QB 1-1Jinx Cyrus Rodillo0% (1)

- Answer2 TaDocument13 pagesAnswer2 TaJohn BryanNo ratings yet

- Required: 1a. Assuming That The Company Has No Alternative Use For The Facilities Now Being Used ToDocument2 pagesRequired: 1a. Assuming That The Company Has No Alternative Use For The Facilities Now Being Used ToErica AbegoniaNo ratings yet

- Cost of CapitalDocument26 pagesCost of CapitalRiti Nayyar100% (1)

- Calculating WACC for Capital Structure ChangesDocument42 pagesCalculating WACC for Capital Structure Changesarmailgm67% (6)

- Problems On Cost of CapitalDocument4 pagesProblems On Cost of CapitalAshutosh Biswal100% (1)

- Lec8.Cost of CapitalDocument52 pagesLec8.Cost of Capitalvivek patelNo ratings yet

- Assignment chp10Document10 pagesAssignment chp10Aalizae Anwar YazdaniNo ratings yet

- Answers of The ProblemDocument11 pagesAnswers of The ProblemRavi KantNo ratings yet

- Cost of CapitalDocument19 pagesCost of CapitalChintan KeniaNo ratings yet

- Risk Management Practices - PakistanDocument9 pagesRisk Management Practices - PakistanBirat SharmaNo ratings yet

- 2009 Student Satisfaction SurveyDocument141 pages2009 Student Satisfaction SurveyBirat SharmaNo ratings yet

- Rotary International QuizDocument7 pagesRotary International QuizBirat SharmaNo ratings yet

- GG ApplicationDocument13 pagesGG ApplicationBirat SharmaNo ratings yet

- The Cost of Capital ExplainedDocument41 pagesThe Cost of Capital ExplainedrakeshkchouhanNo ratings yet

- Variable Types PDFDocument3 pagesVariable Types PDFArinta Riza AndrianiNo ratings yet

- Kaski Workshop EducationDocument11 pagesKaski Workshop EducationBirat SharmaNo ratings yet

- District Committee Responsibilities and GoalsDocument6 pagesDistrict Committee Responsibilities and GoalsBirat SharmaNo ratings yet

- Education in NepalDocument3 pagesEducation in NepalBirat SharmaNo ratings yet

- The Abcs of RotaryDocument34 pagesThe Abcs of RotaryKanwal NainNo ratings yet

- 74-Ecuador Project PlanDocument33 pages74-Ecuador Project PlanBirat SharmaNo ratings yet

- 2009 Student Satisfaction SurveyDocument141 pages2009 Student Satisfaction SurveyBirat SharmaNo ratings yet

- Bangalore Cancer Global Grant ProposalDocument5 pagesBangalore Cancer Global Grant ProposalBirat SharmaNo ratings yet

- Reasons For Being RotarianDocument2 pagesReasons For Being RotarianBirat SharmaNo ratings yet

- Chandra Jyoti Lower Secondary School, Sagar-BakanjeDocument5 pagesChandra Jyoti Lower Secondary School, Sagar-BakanjeBirat SharmaNo ratings yet

- CS - Option Vauation IIDocument50 pagesCS - Option Vauation IIBirat SharmaNo ratings yet

- CS MGMT of MFG Indst-ProposalDocument25 pagesCS MGMT of MFG Indst-ProposalBirat SharmaNo ratings yet

- Benefits of ParkDocument2 pagesBenefits of ParkBirat SharmaNo ratings yet

- Role of Managers in Co-OperativesDocument23 pagesRole of Managers in Co-OperativesBirat SharmaNo ratings yet

- Ethical Issues in Business ResearchDocument18 pagesEthical Issues in Business ResearchHaseeb Shad50% (2)

- Introduction To Research: by Rajendra Lamsal HOD Finance & Marketing Department Lumbini Banijya CampusDocument34 pagesIntroduction To Research: by Rajendra Lamsal HOD Finance & Marketing Department Lumbini Banijya CampusBirat SharmaNo ratings yet

- Lecture 7 SamplingDocument21 pagesLecture 7 SamplingBirat SharmaNo ratings yet

- 01 Introduction RMDocument70 pages01 Introduction RMBirat SharmaNo ratings yet

- Munro Briefing 5 - Approaches To Action ResearchDocument10 pagesMunro Briefing 5 - Approaches To Action ResearchBirat SharmaNo ratings yet

- Annual Working Capital Survey - UK 2011Document24 pagesAnnual Working Capital Survey - UK 2011Birat SharmaNo ratings yet

- Risk Management Practices of Scheduled Commercial Banks: Officers' PerceptionsDocument18 pagesRisk Management Practices of Scheduled Commercial Banks: Officers' PerceptionsBirat SharmaNo ratings yet

- Parent Survey Results 2012Document7 pagesParent Survey Results 2012Birat SharmaNo ratings yet

- 13 SISME p8Document16 pages13 SISME p8Birat SharmaNo ratings yet

- Risk Management Practices of Scheduled Commercial Banks: Officers' PerceptionsDocument18 pagesRisk Management Practices of Scheduled Commercial Banks: Officers' PerceptionsBirat SharmaNo ratings yet

- Working Capital Management Practiced in Pharmaceutical CompaniedDocument12 pagesWorking Capital Management Practiced in Pharmaceutical CompaniedBirat SharmaNo ratings yet

- Financial Institutions NotesDocument12 pagesFinancial Institutions NotesSherif ElSheemyNo ratings yet

- Market Leader Ekonomski TerminiDocument6 pagesMarket Leader Ekonomski TerminipraskevichiusNo ratings yet

- Hang Seng Index: FeaturesDocument2 pagesHang Seng Index: FeaturesHaroon GorayaNo ratings yet

- SBI BC DataDocument170 pagesSBI BC DataAbhishek SinghNo ratings yet

- Blackbook Project On Ipo 1 - 163420152Document63 pagesBlackbook Project On Ipo 1 - 163420152Dipak Chauhan78% (9)

- Presentation of MATHEMATICSDocument18 pagesPresentation of MATHEMATICSJenemarNo ratings yet

- Financial Management 2E: Rajiv Srivastava - Dr. Anil MisraDocument5 pagesFinancial Management 2E: Rajiv Srivastava - Dr. Anil MisraAnkit AgarwalNo ratings yet

- Corporate Actions and Events GuideDocument28 pagesCorporate Actions and Events GuideDhwani PatelNo ratings yet

- 13 Flist 2018 Q 2Document541 pages13 Flist 2018 Q 2pelayogarnicatatianaNo ratings yet

- Callan's Annual Periodic Table of Investment Returns 2017Document2 pagesCallan's Annual Periodic Table of Investment Returns 2017CallanNo ratings yet

- Credit Suisse Hikes PH GDP Growth Forecast to 3.5Document5 pagesCredit Suisse Hikes PH GDP Growth Forecast to 3.5Iann CajNo ratings yet

- Thesis On Ghana Stock ExchangeDocument4 pagesThesis On Ghana Stock Exchangeggzgpeikd100% (2)

- ACES - Annual Report 2021Document176 pagesACES - Annual Report 2021.No ratings yet

- Guide To Global Stock ExchangesDocument199 pagesGuide To Global Stock ExchangesvipulscribdNo ratings yet

- Forecasting Stock Prices Using LSTM and Web Sentiment AnalysisDocument4 pagesForecasting Stock Prices Using LSTM and Web Sentiment AnalysisVipul SinghNo ratings yet

- Thesis On Indian Capital MarketDocument7 pagesThesis On Indian Capital MarketAsia Smith100% (1)

- Chapter 10Document30 pagesChapter 10Mahmoud Abu ShamlehNo ratings yet

- Delta Hedging QuestionsDocument3 pagesDelta Hedging QuestionsClaudia ChoiNo ratings yet

- Guardian CFD BrochureDocument12 pagesGuardian CFD BrochureChrisTheodorouNo ratings yet

- Wisdom of Great InvestorsDocument16 pagesWisdom of Great Investorsdmoo10No ratings yet

- Idx Statistic 2014Document151 pagesIdx Statistic 2014accounting nusaindahNo ratings yet

- Shareholders CorrespondenceDocument5 pagesShareholders CorrespondenceAtul KumarNo ratings yet

- Required: Method A Method B Method CDocument109 pagesRequired: Method A Method B Method CNavindra JaggernauthNo ratings yet

- In Practice The Use of The Dividend Discount Model IsDocument1 pageIn Practice The Use of The Dividend Discount Model Istrilocksp SinghNo ratings yet

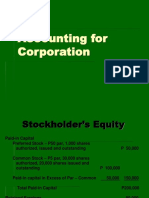

- Accounting For CorporationDocument11 pagesAccounting For CorporationMaricar D. VillarazaNo ratings yet

- Master The MarketsDocument144 pagesMaster The Marketsicm6394% (16)

- Amit Talda NotesDocument235 pagesAmit Talda Notesewrgt4rtg4No ratings yet

- Announcinu ... The 1978 Stock Trader's Almanac: NI The Facts You Need ForDocument1 pageAnnouncinu ... The 1978 Stock Trader's Almanac: NI The Facts You Need ForCopy JunkieNo ratings yet

- A Framework For Risk ManagementDocument16 pagesA Framework For Risk ManagementSimon JosephNo ratings yet

- What Is Meant by Book BuildingDocument2 pagesWhat Is Meant by Book BuildingParul PrasadNo ratings yet

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- LLC or Corporation?: Choose the Right Form for Your BusinessFrom EverandLLC or Corporation?: Choose the Right Form for Your BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Key Performance Indicators: Developing, Implementing, and Using Winning KPIsFrom EverandKey Performance Indicators: Developing, Implementing, and Using Winning KPIsNo ratings yet

- The Business of Venture Capital: The Art of Raising a Fund, Structuring Investments, Portfolio Management, and Exits, 3rd EditionFrom EverandThe Business of Venture Capital: The Art of Raising a Fund, Structuring Investments, Portfolio Management, and Exits, 3rd EditionRating: 5 out of 5 stars5/5 (3)

- Financial Management: The Basic Knowledge of Financial Management for StudentFrom EverandFinancial Management: The Basic Knowledge of Financial Management for StudentNo ratings yet

- Will Work for Pie: Building Your Startup Using Equity Instead of CashFrom EverandWill Work for Pie: Building Your Startup Using Equity Instead of CashNo ratings yet

- The McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/EFrom EverandThe McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/ERating: 4.5 out of 5 stars4.5/5 (6)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)