You might also like

- Money Learning Outcomes: Meaning of Money Market. A Money Market Is A Market For Short-Term LoansDocument17 pagesMoney Learning Outcomes: Meaning of Money Market. A Money Market Is A Market For Short-Term LoanspraneixNo ratings yet

- Lecture 35Document21 pagesLecture 35praneix100% (1)

- Lecture 32Document10 pagesLecture 32praneixNo ratings yet

- Lecture 34Document10 pagesLecture 34praneixNo ratings yet

- Lecture 36Document14 pagesLecture 36praneix100% (1)

- Sixsigma FinalDocument2 pagesSixsigma FinalpraneixNo ratings yet

- Lecture 33Document26 pagesLecture 33praneixNo ratings yet

- Lecture 29Document9 pagesLecture 29praneixNo ratings yet

- Lesson - 26 Foreign Exchange - 1 Learning OutcomesDocument11 pagesLesson - 26 Foreign Exchange - 1 Learning OutcomespraneixNo ratings yet

- Lecture 21Document10 pagesLecture 21praneixNo ratings yet

- Lesson - 28 Foreign Exchange Rates Learning OutcomesDocument4 pagesLesson - 28 Foreign Exchange Rates Learning OutcomespraneixNo ratings yet

- Lecture 23Document9 pagesLecture 23praneixNo ratings yet

- Lecture 27Document15 pagesLecture 27praneixNo ratings yet

- Lesson - 19 National: Income - 1 Circular Flow and Measurement of National IncomeDocument8 pagesLesson - 19 National: Income - 1 Circular Flow and Measurement of National IncomepraneixNo ratings yet

- Lecture 12Document15 pagesLecture 12praneix0% (1)

- National Income and Circular Flow of IncomeDocument22 pagesNational Income and Circular Flow of IncomePriya AnantharamanNo ratings yet

- Lecture 17Document14 pagesLecture 17praneixNo ratings yet

- Lecture 16Document13 pagesLecture 16praneixNo ratings yet

- Lecture 09Document7 pagesLecture 09praneixNo ratings yet

- Lecture 18Document20 pagesLecture 18praneixNo ratings yet

- Lecture 15Document8 pagesLecture 15praneixNo ratings yet

- Lecture 11Document11 pagesLecture 11praneixNo ratings yet

- Lecture 14Document9 pagesLecture 14praneixNo ratings yet

- Lecture 10Document13 pagesLecture 10praneixNo ratings yet

- Lecture 06Document16 pagesLecture 06praneixNo ratings yet

- Unit - 1 Basics of Managerial Ecnomics LESSON 5-Tools and Technique of Decision MakingDocument5 pagesUnit - 1 Basics of Managerial Ecnomics LESSON 5-Tools and Technique of Decision MakingpraneixNo ratings yet

- Lecture 07Document6 pagesLecture 07praneixNo ratings yet

- Lecture 08Document9 pagesLecture 08praneixNo ratings yet

- Lecture 04Document4 pagesLecture 04praneixNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Part 5Document2 pagesPart 5PRETTYKO0% (1)

- Web Appendix: Solutions To Self-Test ProblemsDocument28 pagesWeb Appendix: Solutions To Self-Test ProblemsElba Rossemary Vela MaytaNo ratings yet

- A Project Report ON: (Bank Loan Proposal)Document13 pagesA Project Report ON: (Bank Loan Proposal)varshamankarNo ratings yet

- Acctg Lab 7Document8 pagesAcctg Lab 7AngieNo ratings yet

- Accounting Cycle Practice Problem - Final ExamDocument2 pagesAccounting Cycle Practice Problem - Final ExamAMNEERA SHANIA LALANTONo ratings yet

- Chap7 PDFDocument61 pagesChap7 PDFAshraf Alawneh100% (1)

- Act1205 Midterm Exam For Posting PDFDocument9 pagesAct1205 Midterm Exam For Posting PDFteam SAMNo ratings yet

- Pof AFS SundayDocument32 pagesPof AFS SundayAsad AhmedNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Change in Psr-12th Commerce-AccountancyDocument5 pagesChange in Psr-12th Commerce-Accountancysinghharshu3222No ratings yet

- Cma Esp Additional Practice Questions Part 2 FinalDocument175 pagesCma Esp Additional Practice Questions Part 2 FinalPattyNo ratings yet

- Working Capital ReviewerDocument4 pagesWorking Capital Reviewerjennyxrous26No ratings yet

- Batch 93 FAR First Preboard February 2023Document15 pagesBatch 93 FAR First Preboard February 2023Ameroden AbdullahNo ratings yet

- Asii PDFDocument2 pagesAsii PDFKhaerudin RangersNo ratings yet

- Accounting CH 5Document32 pagesAccounting CH 5Nguyen Dac ThichNo ratings yet

- 08 Audit of InvestmentsDocument10 pages08 Audit of InvestmentsAryando Mocali TampubolonNo ratings yet

- Balance SheetDocument2 pagesBalance SheetK JNo ratings yet

- Actng 1 2Document16 pagesActng 1 2Aries Christian S PadillaNo ratings yet

- Chapter 4 2020Document17 pagesChapter 4 2020JAEHYUK YOONNo ratings yet

- Contemporary Issues in Accounting: Solution ManualDocument17 pagesContemporary Issues in Accounting: Solution ManualKeiLiewNo ratings yet

- Aero Inc Had The Following Statement of Financial Position at PDFDocument2 pagesAero Inc Had The Following Statement of Financial Position at PDFLet's Talk With HassanNo ratings yet

- The Most Recent Statement of Financial Position For Vadeema PLCDocument2 pagesThe Most Recent Statement of Financial Position For Vadeema PLCAmit PandeyNo ratings yet

- Auditing Problems With AnswersDocument12 pagesAuditing Problems With AnswersFlorie May HizoNo ratings yet

- Solution - Problem 13-18Document45 pagesSolution - Problem 13-18Angelika Delosreyes VergaraNo ratings yet

- 4 Internal ReconstructionDocument10 pages4 Internal ReconstructionAnakin SkywalkerNo ratings yet

- Case 01 Buffett 2015 F1769TNDocument18 pagesCase 01 Buffett 2015 F1769TNVaney IoriNo ratings yet

- Finance Interview QuestionsDocument12 pagesFinance Interview QuestionsMD RehanNo ratings yet

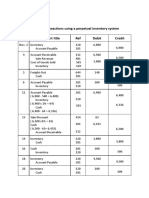

- Group 1: A) Journalize The Transactions Using A Perpetual Inventory System Date Account Title Ref Debit CreditDocument6 pagesGroup 1: A) Journalize The Transactions Using A Perpetual Inventory System Date Account Title Ref Debit CreditQuỳnh'ss Đắc'ssNo ratings yet

- Heineken 2004Document50 pagesHeineken 2004k0yujinNo ratings yet

- Engineering Economics: Rizal Technological UniversityDocument6 pagesEngineering Economics: Rizal Technological UniversityJoshuaNo ratings yet