You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- HJR 192Document2 pagesHJR 192Sue Rhoades100% (13)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Your National Insurance Number: About This FormDocument4 pagesYour National Insurance Number: About This FormTatyana TerziyskaNo ratings yet

- CNN 130111 Yewtree Report PDF Wdf93652Document39 pagesCNN 130111 Yewtree Report PDF Wdf93652Censored News NowNo ratings yet

- 2-2 Affidavit of Mailing Notice - Organizational MeetingDocument1 page2-2 Affidavit of Mailing Notice - Organizational MeetingDaniel100% (1)

- Supplemental Budget of Brookside Barangay CityDocument3 pagesSupplemental Budget of Brookside Barangay CityJonathan75% (4)

- ResolutionDocument2 pagesResolutionAyden Joy Rendon100% (8)

- Batangas Transportation Co V OrlanesDocument2 pagesBatangas Transportation Co V OrlanesMark Leo BejeminoNo ratings yet

- The Feasibility of Merging Naga, Camaligan and GainzaDocument5 pagesThe Feasibility of Merging Naga, Camaligan and Gainzaapi-3709906100% (1)

- Frieden - Classes, Sectors, and Foreign Debt in Latin AmericaDocument21 pagesFrieden - Classes, Sectors, and Foreign Debt in Latin AmericaManuel Romero MolinaNo ratings yet

- Wales Top 300 2013Document5 pagesWales Top 300 2013Wales_Online100% (1)

- Williams Commission: The Report of The Commission On Public Service Governance and Delivery in WalesDocument105 pagesWilliams Commission: The Report of The Commission On Public Service Governance and Delivery in WalesWales_OnlineNo ratings yet

- Susanne Llewellyn-Jones002 PDFDocument1 pageSusanne Llewellyn-Jones002 PDFWales_OnlineNo ratings yet

- 50 Reasons Why North East Business Is GreatDocument1 page50 Reasons Why North East Business Is GreatWales_OnlineNo ratings yet

- Susanne Llewellyn-Jones Coverage in The South Wales Echo, 15 June 1990Document1 pageSusanne Llewellyn-Jones Coverage in The South Wales Echo, 15 June 1990Wales_OnlineNo ratings yet

- Part 1 of The Jillings Report Into Child Abuse in North WalesDocument175 pagesPart 1 of The Jillings Report Into Child Abuse in North WalesWales_OnlineNo ratings yet

- Stage 5 Tour of BritainDocument4 pagesStage 5 Tour of BritainWales_OnlineNo ratings yet

- Susanne Llewellyn-Jones Coverage in The South Wales Echo, 18 August 1980Document1 pageSusanne Llewellyn-Jones Coverage in The South Wales Echo, 18 August 1980Wales_OnlineNo ratings yet

- 2013 02 13 FINAL Silk Evidence PDF - EnglishDocument31 pages2013 02 13 FINAL Silk Evidence PDF - EnglishWales_Online0% (1)

- Susanne Llewellyn-Jones Coverage in The South Wales EchoDocument1 pageSusanne Llewellyn-Jones Coverage in The South Wales EchoWales_OnlineNo ratings yet

- Part 2 of The Jillings Report Into Child Abuse in North WalesDocument143 pagesPart 2 of The Jillings Report Into Child Abuse in North WalesWales_OnlineNo ratings yet

- Stage 4 Tour of BritainDocument4 pagesStage 4 Tour of BritainWales_OnlineNo ratings yet

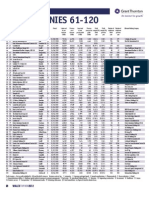

- Top300 61Document1 pageTop300 61Wales_OnlineNo ratings yet

- Top300 121Document1 pageTop300 121Wales_OnlineNo ratings yet

- Top300 1Document1 pageTop300 1Wales_OnlineNo ratings yet

- Fly Tipping 6Document1 pageFly Tipping 6Wales_OnlineNo ratings yet

- Top300 241Document1 pageTop300 241Wales_OnlineNo ratings yet

- Pembrokeshire County Council: Independent Review Pupil Referral UnitDocument29 pagesPembrokeshire County Council: Independent Review Pupil Referral UnitWales_OnlineNo ratings yet

- Improving Schools - Executive SummaryDocument12 pagesImproving Schools - Executive SummaryWales_OnlineNo ratings yet

- Top300 GraphicDocument1 pageTop300 GraphicWales_OnlineNo ratings yet

- Flytipping WalesDocument8 pagesFlytipping WalesWales_OnlineNo ratings yet

- Fly Tipping 5Document3 pagesFly Tipping 5Wales_OnlineNo ratings yet

- Awe MaDocument16 pagesAwe MaWales_OnlineNo ratings yet

- Young Drivers BookletDocument8 pagesYoung Drivers BookletWales_OnlineNo ratings yet

- Football Agent Fees 2011Document7 pagesFootball Agent Fees 2011Wales_OnlineNo ratings yet

- Ministerial Letter On Councillors' RemunerationDocument2 pagesMinisterial Letter On Councillors' RemunerationWales_OnlineNo ratings yet

- Fly Tipping 4Document1 pageFly Tipping 4Wales_OnlineNo ratings yet

- Fly Tipping 3Document1 pageFly Tipping 3Wales_OnlineNo ratings yet

- 2014 Tax CommitmentDocument737 pages2014 Tax Commitmentashes_xNo ratings yet

- Annuario 2010Document202 pagesAnnuario 2010pippo6056No ratings yet

- Sigma Purchase Order TempDocument2 pagesSigma Purchase Order TempusmanitecNo ratings yet

- VIP RECEPTION & GENERAL RECEPTION For Nick LeibhamDocument2 pagesVIP RECEPTION & GENERAL RECEPTION For Nick LeibhamSunlight FoundationNo ratings yet

- Gorakhpur ExpresswayDocument1 pageGorakhpur Expresswayprashant_scribdNo ratings yet

- Public Finance BibliographyDocument3 pagesPublic Finance BibliographyPelajar Baru0% (1)

- 02 Public Expenditures and Budget Reform - Prof. Leonor Magtolis BrionesDocument21 pages02 Public Expenditures and Budget Reform - Prof. Leonor Magtolis BrionesJ. O. M. SalazarNo ratings yet

- 10 Reasons To Vote ConservativeDocument1 page10 Reasons To Vote ConservativeConor BurnsNo ratings yet

- Welsh Rates of Income Tax FaqsDocument4 pagesWelsh Rates of Income Tax Faqsdhinakaranme3056No ratings yet

- PEST Analysis (Egypt Market) External Audit - Threats - OpportunitiesDocument13 pagesPEST Analysis (Egypt Market) External Audit - Threats - OpportunitiesBassem Safwat Boushra75% (4)

- SSC Candidate Application 51155119948Document3 pagesSSC Candidate Application 51155119948Malik MalikNo ratings yet

- 010 Salaries To Municipal Employees and Teachers 2012MAUD - MS200Document1 page010 Salaries To Municipal Employees and Teachers 2012MAUD - MS200Narasimha SastryNo ratings yet

- Kingdom Hall For Sale in Livingson, ScotlandDocument2 pagesKingdom Hall For Sale in Livingson, ScotlandsirjsslutNo ratings yet

- DBM Presentation - 23rd Annual Convention-Janet B. Abuel PDFDocument19 pagesDBM Presentation - 23rd Annual Convention-Janet B. Abuel PDFJacqueline P AlfaroNo ratings yet

- J. Monroe's ResumeDocument1 pageJ. Monroe's ResumeJordan SchultzNo ratings yet

- Output Without RequisitionDocument2 pagesOutput Without RequisitionVaibhav PanchgadeNo ratings yet

- Holcombe 05Document18 pagesHolcombe 05Syahlan G AtjehNo ratings yet

- 2013rev MS581Document2 pages2013rev MS581Nagaraja Rao MukhiralaNo ratings yet

- Waimanoni Marae Committee Meeting Minutes 11 02 15Document2 pagesWaimanoni Marae Committee Meeting Minutes 11 02 15api-283488364No ratings yet

- Documentary Stamp Taxes: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersDocument3 pagesDocumentary Stamp Taxes: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested Answersrayjoshua12No ratings yet

- CHAPTER II: Review of Related Literature I. Legal ReferencesDocument2 pagesCHAPTER II: Review of Related Literature I. Legal ReferencesChaNo ratings yet

- Emulsion and Bitumen Rates BPCL - CBE - 01.09.11Document2 pagesEmulsion and Bitumen Rates BPCL - CBE - 01.09.11karunamoorthi_p22090% (1)