You might also like

- Infrastructure Finance: The Business of Infrastructure for a Sustainable FutureFrom EverandInfrastructure Finance: The Business of Infrastructure for a Sustainable FutureRating: 5 out of 5 stars5/5 (1)

- BASIC Bank Customer Satisfaction SurveyDocument68 pagesBASIC Bank Customer Satisfaction Surveymasudaiub100% (1)

- CbnkingDocument100 pagesCbnkingRana PrathapNo ratings yet

- Harnessing Technology for More Inclusive and Sustainable Finance in Asia and the PacificFrom EverandHarnessing Technology for More Inclusive and Sustainable Finance in Asia and the PacificNo ratings yet

- Standard Charted BankDocument84 pagesStandard Charted BankPari SavlaNo ratings yet

- Derivatives ProjectDocument23 pagesDerivatives ProjectChirag RankjaNo ratings yet

- Info Sys ReportDocument12 pagesInfo Sys Reportaditya_jain0041796No ratings yet

- Integrated Corporate Reporting - A Study... Dr. Kingshuk AdhikariDocument9 pagesIntegrated Corporate Reporting - A Study... Dr. Kingshuk Adhikariరఘువీర్ సూర్యనారాయణNo ratings yet

- Overview of Changing Financial Sector and Emergence of Universal BankingDocument9 pagesOverview of Changing Financial Sector and Emergence of Universal BankingdrkmatterNo ratings yet

- Finance 2Document4 pagesFinance 2vjdragonNo ratings yet

- Sagar M.P.: Marketing Policies B/W HDFC & Icici BankDocument72 pagesSagar M.P.: Marketing Policies B/W HDFC & Icici BankSaurabh UpadhyayNo ratings yet

- Final To Print Services Offered by SBIDocument113 pagesFinal To Print Services Offered by SBISrinivas PalukuriNo ratings yet

- Performance Analysis of Uttara Bank LimitedDocument49 pagesPerformance Analysis of Uttara Bank LimitedConnorLokmanNo ratings yet

- Swot of ICICI BankDocument12 pagesSwot of ICICI BankDedrick JonesNo ratings yet

- Capital Market ReformsDocument6 pagesCapital Market ReformsPoonam SwamiNo ratings yet

- Introduction to Exim Bank LimitedDocument43 pagesIntroduction to Exim Bank LimitedAzim KowshikNo ratings yet

- Market-Based Financing Urban Infrastructure IndiaDocument12 pagesMarket-Based Financing Urban Infrastructure IndiaAkash ShuklaNo ratings yet

- AcknowledgementDocument12 pagesAcknowledgementPushpa BaruaNo ratings yet

- MCB Internship ReportDocument62 pagesMCB Internship ReportJaikrishan RajNo ratings yet

- Retail Banking in India - DocfinalDocument37 pagesRetail Banking in India - DocfinalYaadrahulkumar MoharanaNo ratings yet

- Merchant BankingDocument96 pagesMerchant BankingJerome RandolphNo ratings yet

- Banking Sector Growth in IndiaDocument12 pagesBanking Sector Growth in IndiajegankvpNo ratings yet

- Ubi, Icici, HDFCDocument70 pagesUbi, Icici, HDFCankitverma9716No ratings yet

- Report On EXIM BankDocument120 pagesReport On EXIM Banksimanto2kumarNo ratings yet

- Sequrity AnalysisDocument72 pagesSequrity AnalysisGanganiMehulNo ratings yet

- Execution and Analysis of Working Capital As A Product of HDFC BankDocument43 pagesExecution and Analysis of Working Capital As A Product of HDFC Banknikhil0889No ratings yet

- Syndicate Bank HRDocument64 pagesSyndicate Bank HRsrinibashb5546100% (1)

- IMPACT OF INTREST RATE ON NIFTY ReportDocument57 pagesIMPACT OF INTREST RATE ON NIFTY ReportAditya VardhanNo ratings yet

- MSC Thesis ProposalDocument47 pagesMSC Thesis ProposalEric Osei Owusu-kumihNo ratings yet

- HDFC G - 1Document83 pagesHDFC G - 1Gurinder SinghNo ratings yet

- Wa0013.Document11 pagesWa0013.Merlyn MartinNo ratings yet

- Bunty BLCK BookDocument9 pagesBunty BLCK BookSBI103 PranayNo ratings yet

- Financial Performance Analysis On Dhaka Bank LTDDocument15 pagesFinancial Performance Analysis On Dhaka Bank LTDনূরুল আলম শুভNo ratings yet

- Acknowledgement: Shukla, RPEC Sec 78 Mohali For Allowing Me To Undergo Training at Karvy StockDocument52 pagesAcknowledgement: Shukla, RPEC Sec 78 Mohali For Allowing Me To Undergo Training at Karvy StockPreet JosanNo ratings yet

- Indian Banking IndustryDocument30 pagesIndian Banking IndustryApoorv GoelNo ratings yet

- INTERNATIONAL FINANCIAL MARKETS REPORTDocument47 pagesINTERNATIONAL FINANCIAL MARKETS REPORTReshma MaliNo ratings yet

- International Financial Markets FinalDocument46 pagesInternational Financial Markets Finalprashantgorule100% (1)

- Untitled DocumentDocument44 pagesUntitled Documentjamwalvarun58No ratings yet

- Uti Mutual FundDocument86 pagesUti Mutual Fundprashantgorule100% (3)

- Changing Face of Indian BankingDocument22 pagesChanging Face of Indian Bankinganon_356753627No ratings yet

- Service Marketing Question BankDocument10 pagesService Marketing Question BankKarthika Nathan100% (3)

- A Project Report On A Comparitive Analysis of Different Product and Marketing Strategies of Kotak Mahindra Bank W.R.T Other BanksDocument112 pagesA Project Report On A Comparitive Analysis of Different Product and Marketing Strategies of Kotak Mahindra Bank W.R.T Other BanksNishaAroraNo ratings yet

- HDFC Project ReportDocument55 pagesHDFC Project ReportManeesh Sharma100% (1)

- Market Strategy of Reliance Communication for GSM and CDMA Postpaid ServicesDocument111 pagesMarket Strategy of Reliance Communication for GSM and CDMA Postpaid ServicesSami ZamaNo ratings yet

- Project On Foreign BanksDocument57 pagesProject On Foreign BanksAditya SawantNo ratings yet

- Project on Export Import Bank of India (EXIM BankDocument75 pagesProject on Export Import Bank of India (EXIM BankMohit Kala64% (11)

- HGHJDocument94 pagesHGHJankitverma9716No ratings yet

- Development Finance Institutions in Nigeria: Structure, Roles and AssessmentDocument7 pagesDevelopment Finance Institutions in Nigeria: Structure, Roles and AssessmentMalik SaimaNo ratings yet

- Background of The Dhaka BankDocument15 pagesBackground of The Dhaka BankZakaria Ebne AminNo ratings yet

- Final Report Mutual Fund Valuation and Accounting 1Document69 pagesFinal Report Mutual Fund Valuation and Accounting 1Neha Aggarwal AhujaNo ratings yet

- Consumer Perception Icici Bank SynopsisDocument8 pagesConsumer Perception Icici Bank Synopsisbantu121No ratings yet

- FDI in India's Retail Sector - More Good than BadDocument22 pagesFDI in India's Retail Sector - More Good than BadsrisaiuniversityNo ratings yet

- Chapter 1: INTRODUCTIONDocument14 pagesChapter 1: INTRODUCTIONprajwal jainNo ratings yet

- Final Micro Finance ReportDocument89 pagesFinal Micro Finance ReportNilabjo Kanti Paul50% (2)

- MBA Finance ProjectDocument73 pagesMBA Finance Projectsabaris477No ratings yet

- Comparative Analysis of Saving Account of HDFC ICICI BankDocument59 pagesComparative Analysis of Saving Account of HDFC ICICI BankCharith LiyanageNo ratings yet

- Thesis On IFIC BANK BangladeshDocument94 pagesThesis On IFIC BANK BangladeshjilanistuNo ratings yet

- Role of Financial Institutional Investors in Indian Capital MarketDocument37 pagesRole of Financial Institutional Investors in Indian Capital MarketHimanshu BokadiaNo ratings yet

- Fina DissDocument65 pagesFina DissAshwani SinghNo ratings yet

- UDocument2 pagesUSaurabh UpadhyayNo ratings yet

- Cash Confirmation Format-BinaDocument1 pageCash Confirmation Format-BinaSaurabh Upadhyay0% (1)

- Project Report On LICDocument60 pagesProject Report On LICcoolvats70% (37)

- Ilabadh BankDocument1 pageIlabadh BankSaurabh UpadhyayNo ratings yet

- Ecosystem Services PresentationDocument11 pagesEcosystem Services PresentationSaurabh UpadhyayNo ratings yet

- Frint MonicaDocument55 pagesFrint MonicaSaurabh UpadhyayNo ratings yet

- Bookstore 2016Document59 pagesBookstore 2016Saurabh UpadhyayNo ratings yet

- Cash Confirmation Format-BinaDocument1 pageCash Confirmation Format-BinaSaurabh Upadhyay0% (1)

- To Study Effect of Age On Face Using Photogrammetry: Master of Science IN ForensicscienceDocument1 pageTo Study Effect of Age On Face Using Photogrammetry: Master of Science IN ForensicscienceSaurabh UpadhyayNo ratings yet

- Max Life Insurance Project ReportDocument55 pagesMax Life Insurance Project ReportSaurabh Upadhyay0% (1)

- A Project ON: "Customer Satisfaction Survey On Private and Public Telecom Users in Sagar"Document3 pagesA Project ON: "Customer Satisfaction Survey On Private and Public Telecom Users in Sagar"Saurabh UpadhyayNo ratings yet

- Pgdca ProjectDocument5 pagesPgdca ProjectSaurabh UpadhyayNo ratings yet

- Monica GuptaDocument2 pagesMonica GuptaSaurabh UpadhyayNo ratings yet

- DR Hari SinghDocument71 pagesDR Hari SinghSaurabh UpadhyayNo ratings yet

- Ultra Sound PDFDocument1 pageUltra Sound PDFSaurabh UpadhyayNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Imran SsoDocument1 pageImran SsoSaurabh UpadhyayNo ratings yet

- Monica GuptaDocument2 pagesMonica GuptaSaurabh UpadhyayNo ratings yet

- TST PDFDocument1 pageTST PDFSaurabh UpadhyayNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- A Project ON: "Customer Satisfaction Survey On Private and Public Telecom Users in Sagar"Document3 pagesA Project ON: "Customer Satisfaction Survey On Private and Public Telecom Users in Sagar"Saurabh UpadhyayNo ratings yet

- Resume KapilDocument2 pagesResume KapilSaurabh UpadhyayNo ratings yet

- II Evaluation 2014 - 15 Maths: Marks: 50 Class: NurseryDocument6 pagesII Evaluation 2014 - 15 Maths: Marks: 50 Class: NurserySaurabh UpadhyayNo ratings yet

- To Whom So Ever It May ConcernDocument1 pageTo Whom So Ever It May ConcernSaurabh UpadhyayNo ratings yet

- JH N Ifr Dks'Ky Yksd Dy K.K Lfefr Fguksrk Ujflagx Ftyk Neksg E0Iz0Document2 pagesJH N Ifr Dks'Ky Yksd Dy K.K Lfefr Fguksrk Ujflagx Ftyk Neksg E0Iz0Saurabh UpadhyayNo ratings yet

- DateDocument1 pageDateSaurabh UpadhyayNo ratings yet

- Final Summer Training Project MarutiDocument55 pagesFinal Summer Training Project Marutishivam_nnn75% (4)

- Sbi FormDocument8 pagesSbi Formjigar_gajjar_9No ratings yet

- Gopalganj WardDocument798 pagesGopalganj WardSaurabh UpadhyayNo ratings yet

- Deepesh JainDocument1 pageDeepesh JainSaurabh UpadhyayNo ratings yet

- Deloitte CX in Banking EnglishDocument12 pagesDeloitte CX in Banking EnglishalexNo ratings yet

- Topic 5 Working Capital and Current Asset ManagementDocument65 pagesTopic 5 Working Capital and Current Asset ManagementbriogeliqueNo ratings yet

- Bank Statement June-August 2019Document1 pageBank Statement June-August 2019sathish skNo ratings yet

- BMO Annual Report 2020Document218 pagesBMO Annual Report 2020Bilal MustafaNo ratings yet

- Prime BrokerageDocument118 pagesPrime BrokerageStelu OlarNo ratings yet

- Excel Spreadsheet SampleDocument27 pagesExcel Spreadsheet SampleJennifer VegaNo ratings yet

- MR - Manoj B Wilson: Page 1 of 3 M-87654321-1Document3 pagesMR - Manoj B Wilson: Page 1 of 3 M-87654321-1Manoj WilsonNo ratings yet

- The Bank of KhyberDocument15 pagesThe Bank of KhyberNaila Mehboob100% (2)

- MBFM 5 PDFDocument13 pagesMBFM 5 PDFMANISHA GARGNo ratings yet

- Ibps RRB Po 2017 Capsule by Gopal Sir NewDocument83 pagesIbps RRB Po 2017 Capsule by Gopal Sir NewPraveen ChaudharyNo ratings yet

- Garbemco StoryDocument4 pagesGarbemco Storyᜇᜎᜄ ᜁᜄᜉNo ratings yet

- ABU ROAD SHOE MARKET SANJAY PLACE ACCOUNTANTS LISTDocument209 pagesABU ROAD SHOE MARKET SANJAY PLACE ACCOUNTANTS LISTDev SharmaNo ratings yet

- Regional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerDocument2 pagesRegional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerCynthia ChandlerNo ratings yet

- Precision Drilling Announces Middle East New Build Award and Proposed Private OfferingDocument4 pagesPrecision Drilling Announces Middle East New Build Award and Proposed Private OfferingzNo ratings yet

- Credit Management at Janata BankDocument58 pagesCredit Management at Janata BankRubicon InternationalNo ratings yet

- RBI Guideline On UCBS NOTI082Document11 pagesRBI Guideline On UCBS NOTI082sroyNo ratings yet

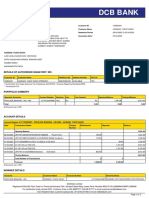

- DCB Bank: Statement of AccountDocument2 pagesDCB Bank: Statement of AccounthasnainNo ratings yet

- Study of Non Performing Assets in Bank of Maharashtra.Document74 pagesStudy of Non Performing Assets in Bank of Maharashtra.Arun Savukar60% (10)

- Treasury BillsDocument11 pagesTreasury BillspoojaNo ratings yet

- 145 Manish ValechaDocument66 pages145 Manish ValechaMeet GandhiNo ratings yet

- IBPS Clerk Main 2016 Capsule by AffairscloudDocument91 pagesIBPS Clerk Main 2016 Capsule by AffairscloudMadhu SekharNo ratings yet

- OSP#16078878Document6 pagesOSP#16078878Guhanadh PadarthyNo ratings yet

- 2010 FirstRand Annual Report 1Document450 pages2010 FirstRand Annual Report 1Sathya SeelanNo ratings yet

- TDS Rates For AY 10-11 PDFDocument1 pageTDS Rates For AY 10-11 PDFjiten1986No ratings yet

- Chap012 Solution Manual Financial Institutions Management A Risk Management ApprDocument12 pagesChap012 Solution Manual Financial Institutions Management A Risk Management ApprПита ДаминNo ratings yet

- Introduction To Financial MarketsDocument109 pagesIntroduction To Financial Marketssadhana100% (1)

- Equity ResearchDocument24 pagesEquity ResearchMaxime BayenNo ratings yet

- Business Communication Project-NBP Gomal University Branch DiKhanDocument10 pagesBusiness Communication Project-NBP Gomal University Branch DiKhan✬ SHANZA MALIK ✬No ratings yet

- Books Prime of EntryDocument2 pagesBooks Prime of EntryAdriana FilzahNo ratings yet

- M& A - Case Study PresentationDocument71 pagesM& A - Case Study PresentationDilip JagadNo ratings yet

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)