You might also like

- Basics of Supply Chain Management Concepts and Key FunctionsDocument35 pagesBasics of Supply Chain Management Concepts and Key FunctionsAshish SinghNo ratings yet

- Spanish - Ii: Course Code: MMS 246 Credit Units: 02 Course ObjectiveDocument1 pageSpanish - Ii: Course Code: MMS 246 Credit Units: 02 Course ObjectiveAshish SinghNo ratings yet

- Subliminal FinalDocument22 pagesSubliminal FinalAshish SinghNo ratings yet

- Trainning Woes: Ashish Kr. Singh B-43 Akash Sharma B-52 Harshit Sharma B-39 Rajendra Mehta B-45 Gokul Nath B-38Document2 pagesTrainning Woes: Ashish Kr. Singh B-43 Akash Sharma B-52 Harshit Sharma B-39 Rajendra Mehta B-45 Gokul Nath B-38Ashish SinghNo ratings yet

- Lab CDocument44 pagesLab CAshish SinghNo ratings yet

- RamayanDocument24 pagesRamayanAshish SinghNo ratings yet

- CampusAmbassador AppDocument2 pagesCampusAmbassador AppKarthick NarayananNo ratings yet

- AdiDocument74 pagesAdiAshish SinghNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

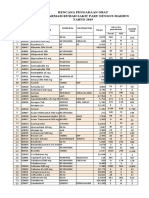

- Rencana Pengadaan Farmasi Semt 2 2019Document38 pagesRencana Pengadaan Farmasi Semt 2 2019dwiiwidiaNo ratings yet

- Antidepressants Pharmacology LectureDocument19 pagesAntidepressants Pharmacology LectureHomman TommanNo ratings yet

- Kissei PerformanceDocument23 pagesKissei PerformancelichenresearchNo ratings yet

- PharmacyDocument3 pagesPharmacyAlyssa PicarNo ratings yet

- Pharmacognosy guide for pharmacy techniciansDocument61 pagesPharmacognosy guide for pharmacy techniciansKumar rajesh Kumar rajeshNo ratings yet

- Review On Gastroretentive Drug Delivery SytemDocument9 pagesReview On Gastroretentive Drug Delivery SytemBaru Chandrasekhar Rao100% (1)

- Cannabis - A Compilation (12-19-2009)Document78 pagesCannabis - A Compilation (12-19-2009)phr3d0m2gr0100% (3)

- Bioequivalence Study - in Vitro TestDocument19 pagesBioequivalence Study - in Vitro TestDoinita DuranNo ratings yet

- Validated UV Spectrophotometric Method Development For Simultaneous Estimation of Tazarotene and Hydroquinone in Gel PreparationDocument3 pagesValidated UV Spectrophotometric Method Development For Simultaneous Estimation of Tazarotene and Hydroquinone in Gel PreparationalfaNo ratings yet

- Phardose Lab Aromatic Water Dakin SDocument5 pagesPhardose Lab Aromatic Water Dakin SJaica Mangurali TumulakNo ratings yet

- Pharmaceutical MarketingDocument25 pagesPharmaceutical MarketingGodson YogarajanNo ratings yet

- Withdrawal Symptoms After Selective Serotonin Reuptake Inhibitor Discontinuation - A Systematic ReviewDocument10 pagesWithdrawal Symptoms After Selective Serotonin Reuptake Inhibitor Discontinuation - A Systematic ReviewGastón PacciaroniNo ratings yet

- Review of Literature on Fast Dissolving TabletsDocument22 pagesReview of Literature on Fast Dissolving TabletsSunil ChaudharyNo ratings yet

- MCQ Pathways9th.IDocument4 pagesMCQ Pathways9th.Iareej alblowi100% (1)

- FDIDocument16 pagesFDIbhartissNo ratings yet

- Range Brochure PDFDocument148 pagesRange Brochure PDFOlavRueslattenNo ratings yet

- Assignment - Copy EditorsDocument4 pagesAssignment - Copy Editors21066 NIDHI NGAIHOIHNo ratings yet

- Ethics in Pharmacy PracticeDocument21 pagesEthics in Pharmacy PracticeLighto Ryusaki100% (1)

- Account Name and Title ReportDocument20 pagesAccount Name and Title ReportSumit Mishra100% (2)

- Warner LambertDocument19 pagesWarner LambertEhsan KarimNo ratings yet

- Moringa Oleifera Aqueous Leaf Extract Down-Regulates Nuclear Factor-Kappab and Increases Cytotoxic Effect of Chemotherapy in Pancreatic Cancer CellsDocument7 pagesMoringa Oleifera Aqueous Leaf Extract Down-Regulates Nuclear Factor-Kappab and Increases Cytotoxic Effect of Chemotherapy in Pancreatic Cancer CellsDewi EfnajuwitaNo ratings yet

- In Vitro Studies On Release and Human Skin Permeation of Australian Tea Tree Oil (TTO) From Topical FormulationsDocument7 pagesIn Vitro Studies On Release and Human Skin Permeation of Australian Tea Tree Oil (TTO) From Topical FormulationsEng.Químico SCNo ratings yet

- Financial Analysis of Glaxosmithkline Bangladesh LimitedDocument37 pagesFinancial Analysis of Glaxosmithkline Bangladesh LimitedMd ShohanNo ratings yet

- 08 Psilocyn Sop Rev 4Document0 pages08 Psilocyn Sop Rev 4Mark ReinhardtNo ratings yet

- Profiles of Drug Substances Vol 05Document556 pagesProfiles of Drug Substances Vol 05Binhnguyen Nguyen100% (3)

- Osmotic DiureticsDocument30 pagesOsmotic Diureticsrhimineecat71100% (1)

- Antibiotic ChartsDocument61 pagesAntibiotic Chartspempekplg100% (1)

- Dermatologicals in Singapore: Euromonitor International November 2020Document9 pagesDermatologicals in Singapore: Euromonitor International November 2020Phua Wei TingNo ratings yet

- Ba-Be PDFDocument30 pagesBa-Be PDFUswatun Hasanah7201No ratings yet