You might also like

- Investing in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketFrom EverandInvesting in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketNo ratings yet

- Grantham Quarterly Dec 2011Document4 pagesGrantham Quarterly Dec 2011careyescapitalNo ratings yet

- Gmo Quarterly LetterDocument16 pagesGmo Quarterly LetterAnonymous Ht0MIJ100% (2)

- GMO Grantham Quarterly Apr10Document14 pagesGMO Grantham Quarterly Apr10careyescapitalNo ratings yet

- Financial Fine Print: Uncovering a Company's True ValueFrom EverandFinancial Fine Print: Uncovering a Company's True ValueRating: 3 out of 5 stars3/5 (3)

- GMO JanuaryDocument9 pagesGMO JanuaryZerohedgeNo ratings yet

- The Power to Stop any Illusion of Problems: (Behind Economics and the Myths of Debt & Inflation.): The Power To Stop Any Illusion Of ProblemsFrom EverandThe Power to Stop any Illusion of Problems: (Behind Economics and the Myths of Debt & Inflation.): The Power To Stop Any Illusion Of ProblemsNo ratings yet

- Stocks Have Rallied and Will Now Return Less. Hip Hip Hooray! But Now What?Document5 pagesStocks Have Rallied and Will Now Return Less. Hip Hip Hooray! But Now What?saif_shakeelNo ratings yet

- Grantham 4-25-11 Letter Part 1Document19 pagesGrantham 4-25-11 Letter Part 1wompyfratNo ratings yet

- Across the Great Divide: New Perspectives on the Financial CrisisFrom EverandAcross the Great Divide: New Perspectives on the Financial CrisisNo ratings yet

- Resource Limitations 2: Separating The Dangerous From The Merely SeriousDocument15 pagesResource Limitations 2: Separating The Dangerous From The Merely SeriousDevarsh VakilNo ratings yet

- GMO Capital Q3 2013 Letter To InvestorsDocument15 pagesGMO Capital Q3 2013 Letter To InvestorsWall Street WanderlustNo ratings yet

- GMO Grantham July 09Document6 pagesGMO Grantham July 09rodmorleyNo ratings yet

- The Investor's Manifesto (Review and Analysis of Bernstein's Book)From EverandThe Investor's Manifesto (Review and Analysis of Bernstein's Book)No ratings yet

- Q2 2007 GmoDocument8 pagesQ2 2007 GmoGonçalo Callé Lucas MendesNo ratings yet

- GMO Quarterly Letter-My Sister's Pension Assets 0412 GMO-GranthamDocument11 pagesGMO Quarterly Letter-My Sister's Pension Assets 0412 GMO-GranthamMarko AleksicNo ratings yet

- 7YrForecasts 813Document1 page7YrForecasts 813CanadianValueNo ratings yet

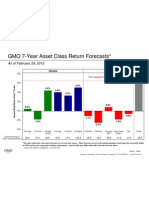

- GMO 7-Year Forecast - Feb '12Document1 pageGMO 7-Year Forecast - Feb '12Douglas RattrayNo ratings yet

- GMO Ben Inker - Valuing Equities in An Economic Crisis - April 6 2009Document6 pagesGMO Ben Inker - Valuing Equities in An Economic Crisis - April 6 2009Brian McMorris100% (1)

- 7YrForecasts 111Document1 page7YrForecasts 111maxiannozziNo ratings yet

- James Montier WhatGoesUpDocument8 pagesJames Montier WhatGoesUpdtpalfiniNo ratings yet

- East Coast Asset Management (Q4 2009) Investor LetterDocument10 pagesEast Coast Asset Management (Q4 2009) Investor Lettermarketfolly.comNo ratings yet

- Gmo Quarterly Letter Q4 2018Document17 pagesGmo Quarterly Letter Q4 2018Stirling AdelhelmNo ratings yet

- Q1 2020 ThirdPoint-InvestorLetterDocument11 pagesQ1 2020 ThirdPoint-InvestorLetterlopaz777No ratings yet

- Third Point Q2 2010 Investor LetterDocument9 pagesThird Point Q2 2010 Investor Lettereric695No ratings yet

- Artko Capital 2018 Q4 LetterDocument9 pagesArtko Capital 2018 Q4 LetterSmitty WNo ratings yet

- Second Quarter 2010 GTAA Fixed IncomeDocument32 pagesSecond Quarter 2010 GTAA Fixed IncomeZerohedge100% (1)

- GMO 7 Year Asset Class Forecast Apr 14Document1 pageGMO 7 Year Asset Class Forecast Apr 14CanadianValueNo ratings yet

- GMO 2009 1st Quarter Investor LetterDocument14 pagesGMO 2009 1st Quarter Investor LetterBrian McMorris100% (2)

- East Coast Q1 2015 MR Market RevisitedDocument17 pagesEast Coast Q1 2015 MR Market RevisitedCanadianValue0% (1)

- Jgletter All 3q09Document14 pagesJgletter All 3q09ZerohedgeNo ratings yet

- R. Driehaus, Unconventional Wisdom in The Investment ProcessDocument6 pagesR. Driehaus, Unconventional Wisdom in The Investment Processbagelboy2No ratings yet

- PzenaCommentary Second Quarter 2013Document3 pagesPzenaCommentary Second Quarter 2013CanadianValueNo ratings yet

- Greenlight GMDocument15 pagesGreenlight GMZerohedge100% (1)

- Third Point Q2 15Document10 pagesThird Point Q2 15marketfolly.comNo ratings yet

- Second Quarter 2010 GTAA EquitiesDocument68 pagesSecond Quarter 2010 GTAA EquitiesZerohedge100% (1)

- Third Quarter 2010 GTAA EquitiesDocument70 pagesThird Quarter 2010 GTAA EquitiesZerohedge100% (1)

- Mark Yusko LetterDocument43 pagesMark Yusko LetterValueWalk100% (2)

- Klarman WorryingDocument2 pagesKlarman WorryingSudhanshuNo ratings yet

- David Einhorn MSFT Speech-2006Document5 pagesDavid Einhorn MSFT Speech-2006mikesfbayNo ratings yet

- Wally Weitz Letter To ShareholdersDocument2 pagesWally Weitz Letter To ShareholdersAnonymous j5tXg7onNo ratings yet

- Market at Much Less Than Book Value. The Weighted Average Stock Price in Relation To Book Value ForDocument10 pagesMarket at Much Less Than Book Value. The Weighted Average Stock Price in Relation To Book Value ForT Anil KumarNo ratings yet

- Distressed Debt Investing: Seth KlarmanDocument4 pagesDistressed Debt Investing: Seth Klarmanjt322No ratings yet

- Armstrong Economics: The Coming Great Depression. Why Government Is PowerlessDocument44 pagesArmstrong Economics: The Coming Great Depression. Why Government Is PowerlessRobert Bonomo100% (1)

- Bob Chapman Deepening Economic Crisis 23 4 2011Document4 pagesBob Chapman Deepening Economic Crisis 23 4 2011sankaratNo ratings yet

- Worried About A Recession? Don't Blame Free Trade, Cato Free Trade Bulletin No. 34Document4 pagesWorried About A Recession? Don't Blame Free Trade, Cato Free Trade Bulletin No. 34Cato InstituteNo ratings yet

- March 112010 PostsDocument10 pagesMarch 112010 PostsAlbert L. PeiaNo ratings yet

- Brazil Russia India China South AfricaDocument3 pagesBrazil Russia India China South AfricaRAHULSHARMA1985999No ratings yet

- Crashing EconomyDocument2 pagesCrashing EconomyStanleyNo ratings yet

- Rethinking Globalization - NotesDocument13 pagesRethinking Globalization - NotesLana HNo ratings yet

- Spreng Capital Outlook 2010 Q2Document4 pagesSpreng Capital Outlook 2010 Q2a1printingNo ratings yet

- Ricardo's Law: The Unintended Consequence of The Federal Government's Budget Only You Will SeeDocument8 pagesRicardo's Law: The Unintended Consequence of The Federal Government's Budget Only You Will Seehunghl9726No ratings yet

- Global Market Outlook July 2011Document8 pagesGlobal Market Outlook July 2011IceCap Asset ManagementNo ratings yet

- All Greenhouses Are See-Through But Ours Have A Remarkable TransparencyDocument1 pageAll Greenhouses Are See-Through But Ours Have A Remarkable TransparencythickskinNo ratings yet

- Long-Term: Janus Henderson Exists To Help You Achieve Your Fi Nancial GoalsDocument1 pageLong-Term: Janus Henderson Exists To Help You Achieve Your Fi Nancial GoalsthickskinNo ratings yet

- Save When You Subscribe: To The Digital EditionDocument1 pageSave When You Subscribe: To The Digital EditionthickskinNo ratings yet

- GearDocument1 pageGearthickskinNo ratings yet

- Is It Possible To Identify "Bubbles"? Can Investors Profit From This?Document1 pageIs It Possible To Identify "Bubbles"? Can Investors Profit From This?thickskinNo ratings yet

- PyramidDocument1 pagePyramidthickskinNo ratings yet

- Do You Fight Convention With Conviction?Document1 pageDo You Fight Convention With Conviction?thickskinNo ratings yet

- Every Issue Packed With : Download To Your Device NowDocument1 pageEvery Issue Packed With : Download To Your Device NowthickskinNo ratings yet

- Discover One of Our Great Bookazines: WWW - Imagineshop.co - UkDocument1 pageDiscover One of Our Great Bookazines: WWW - Imagineshop.co - UkthickskinNo ratings yet

- With Robots That Have What It Takes To Collaborate.: Let's Write The FutureDocument1 pageWith Robots That Have What It Takes To Collaborate.: Let's Write The FuturethickskinNo ratings yet

- InspectDocument1 pageInspectthickskinNo ratings yet

- Reviews: High King of BritainDocument1 pageReviews: High King of BritainthickskinNo ratings yet

- Gear ZoneDocument1 pageGear ZonethickskinNo ratings yet

- Open Your Eyes.: "The World Just Does Not Fit Conveniently Into The Format of A 35mm Camera"Document1 pageOpen Your Eyes.: "The World Just Does Not Fit Conveniently Into The Format of A 35mm Camera"thickskinNo ratings yet

- Andthevikingconquestofengland1016: King CnutDocument1 pageAndthevikingconquestofengland1016: King CnutthickskinNo ratings yet

- France'S: Power and GloryDocument1 pageFrance'S: Power and GlorythickskinNo ratings yet

- Buy Your Issue Today: W W W.his Tor Yans Wers - Co.ukDocument1 pageBuy Your Issue Today: W W W.his Tor Yans Wers - Co.ukthickskinNo ratings yet

- TankDocument1 pageTankthickskinNo ratings yet

- Bare HandsDocument1 pageBare HandsthickskinNo ratings yet

- Recruiting Now For 2017... Join The Club Today For Only 35!: W. Britain - History in Miniature Since 1893Document1 pageRecruiting Now For 2017... Join The Club Today For Only 35!: W. Britain - History in Miniature Since 1893thickskinNo ratings yet

- The World'S NewsstandDocument1 pageThe World'S NewsstandthickskinNo ratings yet

- Open Your Eyes.: "The World Just Does Not Fit Conveniently Into The Format of A 35mm Camera"Document1 pageOpen Your Eyes.: "The World Just Does Not Fit Conveniently Into The Format of A 35mm Camera"thickskinNo ratings yet

- Holidays, Courses & Tuition: Landscape Wildlife Nature AdventureDocument1 pageHolidays, Courses & Tuition: Landscape Wildlife Nature AdventurethickskinNo ratings yet

- Build A Personal Assistant With Node - JS: Developer TutorialsDocument1 pageBuild A Personal Assistant With Node - JS: Developer TutorialsthickskinNo ratings yet

- Landscape Wildlife Nature Adventure: 96 Outdoor Photography June 2017Document1 pageLandscape Wildlife Nature Adventure: 96 Outdoor Photography June 2017thickskinNo ratings yet

- Photography Holidays: Southeast Iceland - Glacial Landscapes, Coast and HorsesDocument1 pagePhotography Holidays: Southeast Iceland - Glacial Landscapes, Coast and HorsesthickskinNo ratings yet

- Next Month: How To Take Compelling Travel PhotographsDocument1 pageNext Month: How To Take Compelling Travel PhotographsthickskinNo ratings yet

- Develop A Podcast Web Application: Developer TutorialsDocument1 pageDevelop A Podcast Web Application: Developer TutorialsthickskinNo ratings yet

- New-Generation: Web DesignerDocument1 pageNew-Generation: Web DesignerthickskinNo ratings yet

- Sony World Photography AWARDS 2017: Photo ShowcaseDocument1 pageSony World Photography AWARDS 2017: Photo ShowcasethickskinNo ratings yet

- An Analysis of Scandinavian M&a 2001-06Document130 pagesAn Analysis of Scandinavian M&a 2001-06Nick PetersNo ratings yet

- Mgt211 Updated Quiz 1 2021 We'Re David WorriorsDocument18 pagesMgt211 Updated Quiz 1 2021 We'Re David WorriorsDecent RajaNo ratings yet

- Chapter 9Document21 pagesChapter 9kumikooomakiNo ratings yet

- MAMCOMDocument22 pagesMAMCOMRoshniNo ratings yet

- Accounting (Bcom) : Rotman Commerce Specialist OverviewDocument4 pagesAccounting (Bcom) : Rotman Commerce Specialist OverviewMichael WangNo ratings yet

- Econs 101 - Quiz #2 Answer KeyDocument1 pageEcons 101 - Quiz #2 Answer KeySano ManjiroNo ratings yet

- Investment Centers and Transfer PricingDocument9 pagesInvestment Centers and Transfer PricingMohammad Nurul AfserNo ratings yet

- Benihana SimulationDocument4 pagesBenihana SimulationishanNo ratings yet

- Henri Pesch, OverviewDocument24 pagesHenri Pesch, OverviewAndre SetteNo ratings yet

- Economics Notes HindiDocument77 pagesEconomics Notes HindiYashwant Singh RathoreNo ratings yet

- A Crazy Methodology - On The Limits of Macro-Quantitative Social Science ResearchDocument32 pagesA Crazy Methodology - On The Limits of Macro-Quantitative Social Science ResearchIan RonquilloNo ratings yet

- Parabolic SAR (Wilder)Document12 pagesParabolic SAR (Wilder)Subhadip NandyNo ratings yet

- Difference Between Hedging and ArbitrageDocument2 pagesDifference Between Hedging and Arbitrageshreya_rachh1469No ratings yet

- Inference and Arbitrage: The Impact of Statistical Arbitrage On Stock PricesDocument33 pagesInference and Arbitrage: The Impact of Statistical Arbitrage On Stock PriceshanniballectterNo ratings yet

- 12Document3 pages12itachi uchihaNo ratings yet

- 13 Kowalik, From Solidarity To Sellout PDFDocument367 pages13 Kowalik, From Solidarity To Sellout PDFporterszucsNo ratings yet

- Presentation - Capital Expenditure and Operating Expenses BudgetsDocument5 pagesPresentation - Capital Expenditure and Operating Expenses BudgetsBVMF_RINo ratings yet

- Introduction To Manufacturing ProcessesDocument27 pagesIntroduction To Manufacturing ProcessesJohn Philip NadalNo ratings yet

- Dividend Policy - PPTDocument55 pagesDividend Policy - PPTkartik avhadNo ratings yet

- CH 13 Hull Fundamentals 8 The DDocument22 pagesCH 13 Hull Fundamentals 8 The DjlosamNo ratings yet

- Ideal Money - John NashDocument9 pagesIdeal Money - John NashjustingoldbergNo ratings yet

- Market Failure and The Case of Government InterventionDocument16 pagesMarket Failure and The Case of Government InterventionCristine ParedesNo ratings yet

- Iim Lucknow - Pi KitDocument176 pagesIim Lucknow - Pi Kitkumbhare100% (1)

- Solution Manual For Illustrated Guide To The National Electrical Code 7th Edition Charles R MillerDocument23 pagesSolution Manual For Illustrated Guide To The National Electrical Code 7th Edition Charles R MillerTiffanyMilleredpn100% (38)

- Unit 5: Check Your Progress (Page 35)Document3 pagesUnit 5: Check Your Progress (Page 35)Juan Francisco Hidalgo ReinaNo ratings yet

- Analyzing The Movie Office Space Through Marx's PhilosophyDocument4 pagesAnalyzing The Movie Office Space Through Marx's Philosophymartindgr8100% (2)

- Collective Efficiency and Increasing Returns: by Hubert SchmitzDocument28 pagesCollective Efficiency and Increasing Returns: by Hubert SchmitzFakhrudinNo ratings yet

- Prof. SARPV Chaturvedi - Business Management ProfileDocument8 pagesProf. SARPV Chaturvedi - Business Management Profileलक्षमी नृसिहंन् वेन्कटपतिNo ratings yet

- Chapter 1 LmsDocument22 pagesChapter 1 LmsSanaky Việt NamNo ratings yet

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyFrom EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyRating: 3 out of 5 stars3/5 (1)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsFrom EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsNo ratings yet

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsFrom EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsRating: 4.5 out of 5 stars4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondFrom EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondNo ratings yet

- Mind over Money: The Psychology of Money and How to Use It BetterFrom EverandMind over Money: The Psychology of Money and How to Use It BetterRating: 4 out of 5 stars4/5 (24)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)From EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Rating: 4 out of 5 stars4/5 (5)

- Buffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsFrom EverandBuffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsRating: 5 out of 5 stars5/5 (1)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)