You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Super Injunction BookDocument3 pagesSuper Injunction BookReckless Kobold0% (1)

- Concentration of SolutionsDocument32 pagesConcentration of SolutionsRaja Mohan Gopalakrishnan100% (2)

- Dion Market Timing ModelDocument18 pagesDion Market Timing Modelxy053333100% (1)

- 2010 10 06 NJ MezrichDocument26 pages2010 10 06 NJ Mezrichxy053333No ratings yet

- Avro RJ General Data Brochure PDFDocument66 pagesAvro RJ General Data Brochure PDFMonica Enin100% (2)

- Best Practices in Hotel Financial ManagementDocument3 pagesBest Practices in Hotel Financial ManagementDhruv BansalNo ratings yet

- Demystifying Equity Risk-Based StrategiesDocument20 pagesDemystifying Equity Risk-Based Strategiesxy053333No ratings yet

- A Risk-Oriented Model For Factor Rotation DecisionsDocument38 pagesA Risk-Oriented Model For Factor Rotation Decisionsxy053333No ratings yet

- Air India - Balance Score CardDocument6 pagesAir India - Balance Score Cardramyavenugopal100% (1)

- Spisak Parfema NEWDocument1 pageSpisak Parfema NEWDouglas CoxNo ratings yet

- Equity Performance Attribution MethDocument54 pagesEquity Performance Attribution Methxy053333No ratings yet

- Break Even Point ExplanationDocument2 pagesBreak Even Point ExplanationEdgar IbarraNo ratings yet

- 8508Document10 pages8508Danyal ChaudharyNo ratings yet

- Uganda Bureau of Statistics Census of Business Establishments, 2010/11 Report OnDocument169 pagesUganda Bureau of Statistics Census of Business Establishments, 2010/11 Report OnCano KaluNo ratings yet

- SOLAS - Verified Gross Mass (VGM)Document2 pagesSOLAS - Verified Gross Mass (VGM)Mary Joy Dela MasaNo ratings yet

- Cheque and Its TypesDocument2 pagesCheque and Its Typesdevraj subediNo ratings yet

- Closure in Valuation: Estimating Terminal Value: Problem 1Document3 pagesClosure in Valuation: Estimating Terminal Value: Problem 1Silviu TrebuianNo ratings yet

- Apartment Community BrochureDocument7 pagesApartment Community Brochureapi-327678777No ratings yet

- FM 8th Edition Chapter 12 - Risk and ReturnDocument20 pagesFM 8th Edition Chapter 12 - Risk and ReturnKa Io ChaoNo ratings yet

- Chief Executive Officer CPG in West Palm Beach FL Resume James MercerDocument2 pagesChief Executive Officer CPG in West Palm Beach FL Resume James MercerJames MercerNo ratings yet

- Question Bank Volume 2 QDocument231 pagesQuestion Bank Volume 2 QCecilia Mfene Sekubuwane100% (1)

- Harish NatarajanDocument10 pagesHarish NatarajanbananiacorpNo ratings yet

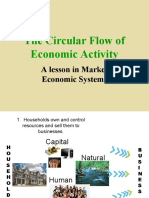

- Circular FlowDocument21 pagesCircular FlowSheryl BorromeoNo ratings yet

- Uy Balance SheetDocument8 pagesUy Balance SheetMary Louise CamposanoNo ratings yet

- Jack Daniel'sDocument17 pagesJack Daniel'sIon TarlevNo ratings yet

- Case Study-1 SHEENADocument2 pagesCase Study-1 SHEENARushikesh Dandagwhal100% (1)

- Chapter 7Document18 pagesChapter 7dheerajm88No ratings yet

- StartUp India - Case AnalysisDocument3 pagesStartUp India - Case AnalysisIrshad AzeezNo ratings yet

- PinoyDocument5 pagesPinoyLarete PaoloNo ratings yet

- Ans Mini Case 2 - A171 - LecturerDocument14 pagesAns Mini Case 2 - A171 - LecturerXue Yin Lew100% (1)

- TWSS CFA Level I - Planner and TrackerDocument6 pagesTWSS CFA Level I - Planner and TrackerSai Ranjit TummalapalliNo ratings yet

- Agriculture Subsidies and DevelopmentDocument2 pagesAgriculture Subsidies and Developmentbluerockwalla100% (2)

- Introduction To Business - 5Document11 pagesIntroduction To Business - 5Md. Rayhanul IslamNo ratings yet

- Powerpoint Lectures For Principles of Macroeconomics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterDocument24 pagesPowerpoint Lectures For Principles of Macroeconomics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterJiya Nitric AcidNo ratings yet

- Tourism PolicyDocument6 pagesTourism Policylanoox0% (1)