You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Diagram of Accounting EquationDocument1 pageDiagram of Accounting EquationMary100% (3)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Kirkpatrick + ModelDocument1 pageKirkpatrick + ModelMaryNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Basic Everyday Journal Entries Retained Earnings and Stockholders EquityDocument2 pagesBasic Everyday Journal Entries Retained Earnings and Stockholders EquityMary100% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Basic Impact of Everyday Journal Entries On The Income StatementDocument2 pagesBasic Impact of Everyday Journal Entries On The Income StatementMary100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Cash Flows Statement Indirect MethodDocument2 pagesCash Flows Statement Indirect MethodMary100% (1)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- End of The Year Adjustment For Allowance For Doubtful AccountsDocument1 pageEnd of The Year Adjustment For Allowance For Doubtful AccountsMary100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Adjusting Entries For Bank ReconciliationDocument1 pageAdjusting Entries For Bank ReconciliationMaryNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Analysis of Financial Statements RatiosDocument2 pagesAnalysis of Financial Statements RatiosMaryNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Special Order AnalysisDocument2 pagesSpecial Order AnalysisMaryNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Continue or Eliminate AnalysisDocument3 pagesContinue or Eliminate AnalysisMaryNo ratings yet

- Make or Buy AnalysisDocument4 pagesMake or Buy AnalysisMaryNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Horizontal Analysis of A Balance SheetDocument3 pagesHorizontal Analysis of A Balance SheetMary100% (6)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Circle of LifeDocument1 pageCircle of LifeMaryNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Scaffolding MethodDocument1 pageScaffolding MethodMaryNo ratings yet

- Journal Entry Format PDFDocument1 pageJournal Entry Format PDFMaryNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Partial Income Statement For Manufacturing CompanyDocument1 pagePartial Income Statement For Manufacturing CompanyMary50% (2)

- Current Assets, Liabilities, and Stockholders' Equity Normal BalancesDocument1 pageCurrent Assets, Liabilities, and Stockholders' Equity Normal BalancesMaryNo ratings yet

- ARCS Method of MotivationDocument1 pageARCS Method of MotivationMaryNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Chunking Method DiagramDocument1 pageChunking Method DiagramMaryNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

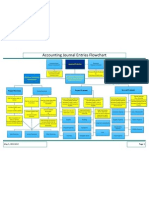

- Accounting Journal Entries Flowchart PDFDocument1 pageAccounting Journal Entries Flowchart PDFMary75% (4)

- Table Factors For Present and Future Value of One DollarDocument6 pagesTable Factors For Present and Future Value of One DollarMaryNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Labor Variance FormulasDocument2 pagesLabor Variance FormulasMaryNo ratings yet

- Materials Variance FormulasDocument2 pagesMaterials Variance FormulasMary100% (1)

- Transaction Analyzes For A CorporationDocument2 pagesTransaction Analyzes For A CorporationMaryNo ratings yet

- Simplified Charts-Percentage Method Income Tax Withholding 2008Document4 pagesSimplified Charts-Percentage Method Income Tax Withholding 2008MaryNo ratings yet

- Calendars For Sales TermsDocument2 pagesCalendars For Sales TermsMaryNo ratings yet

- Simplified Charts - Percentage Method Income Tax Withholding 2012Document4 pagesSimplified Charts - Percentage Method Income Tax Withholding 2012MaryNo ratings yet

- Gross Profit Section of Income Statement-Periodic SystemDocument3 pagesGross Profit Section of Income Statement-Periodic SystemMary67% (3)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Financial StatementsDocument1 pageFinancial StatementsMary100% (4)

- BM2 Chapter 1Document23 pagesBM2 Chapter 1Lowela KasandraNo ratings yet

- Analyzing The Caterpillar Production SystemDocument6 pagesAnalyzing The Caterpillar Production Systemmanasmhatre007100% (2)

- Cost Accounting Part 1 (University of Cebu) Cost Accounting Part 1 (University of Cebu)Document6 pagesCost Accounting Part 1 (University of Cebu) Cost Accounting Part 1 (University of Cebu)Shane TorrieNo ratings yet

- Article On Staff TrainingDocument19 pagesArticle On Staff TrainingAamir SaeedNo ratings yet

- HBL Goes Digital To Grow Its Corporate Banking BusinessDocument4 pagesHBL Goes Digital To Grow Its Corporate Banking Businesssameed iqbalNo ratings yet

- International Strategic ManagementDocument17 pagesInternational Strategic ManagementVadher Amit100% (1)

- Analytics & Data Mastery: and Certification ClassDocument26 pagesAnalytics & Data Mastery: and Certification ClassZeib Shelby100% (1)

- Resume Book of Pmbok Bab 1Document10 pagesResume Book of Pmbok Bab 1Muhamad SyafiiNo ratings yet

- SMUDocument10 pagesSMUAbhisek Sarkar0% (1)

- Vaibhav Bandekar - PROCESS ANALYSIS AND IMPROVEMENTDocument9 pagesVaibhav Bandekar - PROCESS ANALYSIS AND IMPROVEMENTVaibhav BandekarNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Student Dossier 2011-2012 SOILDocument60 pagesStudent Dossier 2011-2012 SOILSaket SaurabhNo ratings yet

- Manual of Works AuditDocument566 pagesManual of Works Auditsaurabh singh100% (1)

- Topic 1: Supply Chain ManagementDocument17 pagesTopic 1: Supply Chain ManagementRoyce DenolanNo ratings yet

- Managing Brands Over Geographic Boundaries and Market SegmentsDocument10 pagesManaging Brands Over Geographic Boundaries and Market SegmentsShenali AndreaNo ratings yet

- International Business: AssignmentDocument7 pagesInternational Business: AssignmentariaNo ratings yet

- Parker Quality ManualDocument33 pagesParker Quality ManualRaul AquinoNo ratings yet

- Enterprise Resource Planning SystemsDocument15 pagesEnterprise Resource Planning SystemsabuNo ratings yet

- Dipali Bundheliya: Sr. Executive HR & Admin at Rex-Tone Industries LTDDocument5 pagesDipali Bundheliya: Sr. Executive HR & Admin at Rex-Tone Industries LTDNILESHNo ratings yet

- Lloyd's Register GroupDocument6 pagesLloyd's Register GroupRhegina Mariztelle ForteNo ratings yet

- Project ReportDocument7 pagesProject ReportShahrooz JuttNo ratings yet

- Incorrect Material Movements PDFDocument55 pagesIncorrect Material Movements PDFsksk1911No ratings yet

- Human Resource Information System (Hris) PlanningDocument26 pagesHuman Resource Information System (Hris) PlanningAde MuseNo ratings yet

- M4T1 - Retail Life CycleDocument2 pagesM4T1 - Retail Life CycleShalu KumariNo ratings yet

- Al-Ko Katalog Paderborn 10 2018-En Lowres PDFDocument146 pagesAl-Ko Katalog Paderborn 10 2018-En Lowres PDFGround ViewNo ratings yet

- Gap Fin SaaS Solv1.2Document6 pagesGap Fin SaaS Solv1.2shanmugaNo ratings yet

- Conventional Views of BA Are Concerned in Some Way With Operating On DataDocument2 pagesConventional Views of BA Are Concerned in Some Way With Operating On DataMaChAnZzz OFFICIALNo ratings yet

- Audit Internal ISO 19011 2018 - 9001Document47 pagesAudit Internal ISO 19011 2018 - 9001Yohannes SinagaNo ratings yet

- Leadership and Influence ProcessesDocument62 pagesLeadership and Influence ProcessesNenad Krstevski75% (4)

- Chapter 2Document2 pagesChapter 2TrangNo ratings yet

- Design and Facilities Management in A Time of Change: Francis DuffyDocument2 pagesDesign and Facilities Management in A Time of Change: Francis DuffyEtnad Oric OreducseNo ratings yet

- The Anatomy of Ethical Leadership: To Lead Our Organizations in a Conscientious and Authentic MannerFrom EverandThe Anatomy of Ethical Leadership: To Lead Our Organizations in a Conscientious and Authentic MannerNo ratings yet

- Lean Maintenance: Reduce Costs, Improve Quality, and Increase Market ShareFrom EverandLean Maintenance: Reduce Costs, Improve Quality, and Increase Market ShareRating: 5 out of 5 stars5/5 (2)

- Inventory Management System A Complete Guide - 2019 EditionFrom EverandInventory Management System A Complete Guide - 2019 EditionNo ratings yet

- Securing Prosperity: The American Labor Market: How It Has Changed and What to Do about ItFrom EverandSecuring Prosperity: The American Labor Market: How It Has Changed and What to Do about ItNo ratings yet

- Do What You Love: And Other Lies About Success & HappinessFrom EverandDo What You Love: And Other Lies About Success & HappinessRating: 4 out of 5 stars4/5 (2)