You might also like

- Banks: Possible Impact of Sharper Than Eyed DR Hikes: Morning BriefingDocument2 pagesBanks: Possible Impact of Sharper Than Eyed DR Hikes: Morning BriefingScorpian MouniehNo ratings yet

- Financials Result ReviewDocument21 pagesFinancials Result ReviewAngel BrokingNo ratings yet

- Kenyan Banks - A Follow Up On Credit Risks As Investors Become Increasingly Concerned - Salient Features On Mortgage SectorDocument9 pagesKenyan Banks - A Follow Up On Credit Risks As Investors Become Increasingly Concerned - Salient Features On Mortgage SectorMukarangaNo ratings yet

- A View On Banks FinalDocument22 pagesA View On Banks FinaljustinsofoNo ratings yet

- Agricultural Bank of ChinaDocument7 pagesAgricultural Bank of ChinaJack YuanNo ratings yet

- OCBC Research Report 2013 July 9 by MacquarieDocument6 pagesOCBC Research Report 2013 July 9 by MacquarietansillyNo ratings yet

- Compare Their Profitability Ratios. Why Is There A Difference?Document24 pagesCompare Their Profitability Ratios. Why Is There A Difference?Shruti MalpaniNo ratings yet

- UAE Banking Sector Outlook 2014: An Uptick in Lending and Economic Activity Signal Continued Profitable GrowthDocument10 pagesUAE Banking Sector Outlook 2014: An Uptick in Lending and Economic Activity Signal Continued Profitable Growthapi-227433089No ratings yet

- Banking: Valuations AttractiveDocument27 pagesBanking: Valuations AttractiveAngel BrokingNo ratings yet

- Owl Fund Financials Sector Condensed UpdateDocument4 pagesOwl Fund Financials Sector Condensed UpdaterjkostNo ratings yet

- Banks: Anticipating A BottomDocument6 pagesBanks: Anticipating A BottomerlanggaherpNo ratings yet

- DBS Bank LTD - Credit Update - 140214Document7 pagesDBS Bank LTD - Credit Update - 140214Invest StockNo ratings yet

- CPI SJ - A Critique On Credit Risks & ROE - Solid Footing But We Maintain Our HOLD On Valuation RiskDocument16 pagesCPI SJ - A Critique On Credit Risks & ROE - Solid Footing But We Maintain Our HOLD On Valuation RiskMukarangaNo ratings yet

- Final Main Pages ProjectDocument103 pagesFinal Main Pages ProjectJeswin Joseph GeorgeNo ratings yet

- LFC Sector Update 13Document16 pagesLFC Sector Update 13Randora LkNo ratings yet

- Assignment Unit II:: Company Profile Case StudyDocument10 pagesAssignment Unit II:: Company Profile Case StudyHạnh NguyễnNo ratings yet

- RBI Monetary Policy ReviewDocument5 pagesRBI Monetary Policy ReviewAngel BrokingNo ratings yet

- JPMorgan Global Investment Banks 2010-09-08Document176 pagesJPMorgan Global Investment Banks 2010-09-08francoib991905No ratings yet

- Samson Corporate Strategy BulletinDocument5 pagesSamson Corporate Strategy BulletinAnonymous Ht0MIJNo ratings yet

- Fag 3qcy2012ruDocument6 pagesFag 3qcy2012ruAngel BrokingNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument26 pagesMarket Outlook Market Outlook: Dealer's DiaryangelbrokingNo ratings yet

- What Keeps Singapore Banks The World's Strongest?: Big Issue 1Document1 pageWhat Keeps Singapore Banks The World's Strongest?: Big Issue 1ervinishereNo ratings yet

- US Bank of Washington - Executive SummaryDocument5 pagesUS Bank of Washington - Executive SummaryJoshua Sullivan100% (2)

- Jones Electrical DistributionDocument6 pagesJones Electrical DistributionMichelle Rodríguez100% (1)

- Bank Loans: Market Dynamics Poised To Deliver Attractive Risk-Adjusted ReturnsDocument6 pagesBank Loans: Market Dynamics Poised To Deliver Attractive Risk-Adjusted ReturnsSabin NiculaeNo ratings yet

- C O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficerDocument61 pagesC O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficervipinkathpalNo ratings yet

- Analysis of Sbi ResultsDocument8 pagesAnalysis of Sbi ResultssrinaathmNo ratings yet

- Trups CDO PrimerDocument8 pagesTrups CDO PrimerAly KanjiNo ratings yet

- SHAW Equity Research ReportDocument13 pagesSHAW Equity Research ReportAnonymous 7CxwuBUJz3No ratings yet

- U I S M: Pdate On Ndian Ecuritisation ArketDocument9 pagesU I S M: Pdate On Ndian Ecuritisation ArketAbhishek SinghNo ratings yet

- Market Outlook 24th January 2012Document12 pagesMarket Outlook 24th January 2012Angel BrokingNo ratings yet

- India Banks: PSU Banks: Time To Use A Finer BrushDocument14 pagesIndia Banks: PSU Banks: Time To Use A Finer BrushVaibhav MittalNo ratings yet

- VCB - Jul 8 2014 by HSC PDFDocument6 pagesVCB - Jul 8 2014 by HSC PDFlehoangthuchienNo ratings yet

- U.S. Equity Strategy (What's Driving The Equity Market) - September 14, 2012Document4 pagesU.S. Equity Strategy (What's Driving The Equity Market) - September 14, 2012dpbasicNo ratings yet

- BT Cuoi Chuong 3 - Sach Peter RoseDocument4 pagesBT Cuoi Chuong 3 - Sach Peter RoseNguyễn Quỳnh TrangNo ratings yet

- Increasing Portfolio MaturityDocument2 pagesIncreasing Portfolio MaturityroshcrazyNo ratings yet

- Banking Sector Update - 230611Document25 pagesBanking Sector Update - 230611chaltrikNo ratings yet

- Jones Electric Case StudyDocument7 pagesJones Electric Case Studymwillar08No ratings yet

- Indian Financials: Tryst With DestinyDocument28 pagesIndian Financials: Tryst With DestinyJohnny HarlowNo ratings yet

- Chapter 7 ExamplesDocument18 pagesChapter 7 Examplesm bNo ratings yet

- Update To Ocwen PaperDocument11 pagesUpdate To Ocwen PaperForeclosure FraudNo ratings yet

- Market Outlook 26th December 2011Document4 pagesMarket Outlook 26th December 2011Angel BrokingNo ratings yet

- Er 20130722 Bull Phat DragonDocument3 pagesEr 20130722 Bull Phat DragonDavid SmithNo ratings yet

- 2018 Response To CCPDocument7 pages2018 Response To CCPCheckmate Research0% (1)

- JP Morgan 8.02.13 PDFDocument9 pagesJP Morgan 8.02.13 PDFChad Thayer VNo ratings yet

- Market Insight Q3FY12 RBI Policy Review Jan12Document3 pagesMarket Insight Q3FY12 RBI Policy Review Jan12poojarajeswariNo ratings yet

- Weekly Market Commentary 5/6/2013Document3 pagesWeekly Market Commentary 5/6/2013monarchadvisorygroupNo ratings yet

- Manila Water Company: Arbitration Brings Uncertainty - : Wednesday, 25 September 2013Document3 pagesManila Water Company: Arbitration Brings Uncertainty - : Wednesday, 25 September 2013RoseAnnFloriaNo ratings yet

- Australian Interest Rates - OI #33 2012Document2 pagesAustralian Interest Rates - OI #33 2012anon_370534332No ratings yet

- Barclays - The Emerging Markets Quarterly - Vietnam - Sep 2012Document3 pagesBarclays - The Emerging Markets Quarterly - Vietnam - Sep 2012SIVVA2No ratings yet

- Credit Memorandum: Situation OverviewDocument2 pagesCredit Memorandum: Situation OverviewAlbert JonesNo ratings yet

- Market Outlook 5th October 2011Document4 pagesMarket Outlook 5th October 2011Angel BrokingNo ratings yet

- RBIPolicy CRISIL 170912Document4 pagesRBIPolicy CRISIL 170912Meenakshi MittalNo ratings yet

- JPM Mortgage WarningsDocument21 pagesJPM Mortgage WarningsZerohedgeNo ratings yet

- Yes Bank: CMP: Target Price: BuyDocument4 pagesYes Bank: CMP: Target Price: BuyramanathanseshaNo ratings yet

- WorldcomDocument5 pagesWorldcomHAN NGUYEN KIM100% (1)

- EOC08 EdittedDocument12 pagesEOC08 EdittedFilip velico100% (1)

- Weekly Trends January 10 2013Document4 pagesWeekly Trends January 10 2013John ClarkeNo ratings yet

- Banking Sector Report 1Document14 pagesBanking Sector Report 1Pathanjali DiduguNo ratings yet

- Roxy Pacific OCBCRDocument4 pagesRoxy Pacific OCBCRphuawlNo ratings yet

- 7 Factors To Low-Code PDFDocument14 pages7 Factors To Low-Code PDFphuawlNo ratings yet

- Alpha-2 Adrenergic Receptor Agonists: A Review of Current Clinical ApplicationsDocument8 pagesAlpha-2 Adrenergic Receptor Agonists: A Review of Current Clinical ApplicationsabdulNo ratings yet

- Gulf Ar2017 en PDFDocument226 pagesGulf Ar2017 en PDFphuawlNo ratings yet

- Colex Fin Dis 1 Q17Document1 pageColex Fin Dis 1 Q17phuawlNo ratings yet

- Cole X 092017Document1 pageCole X 092017phuawlNo ratings yet

- Lauren Templeton - Methods Sir John Templeton Used To Take Advantage of Crisis EventsDocument3 pagesLauren Templeton - Methods Sir John Templeton Used To Take Advantage of Crisis EventsphuawlNo ratings yet

- Singapore E-Commerce Firm Y Ventures Bets Big On Big Data, Technology - The BUSINESS TIMESDocument3 pagesSingapore E-Commerce Firm Y Ventures Bets Big On Big Data, Technology - The BUSINESS TIMESphuawlNo ratings yet

- $685m Bid Triggers Sale of Queenstown Residential Site, Property News & Top Stories - The Straits TimesDocument2 pages$685m Bid Triggers Sale of Queenstown Residential Site, Property News & Top Stories - The Straits TimesphuawlNo ratings yet

- Keppel DC Reit 2q 1h 2017 Results - SgxnetDocument55 pagesKeppel DC Reit 2q 1h 2017 Results - SgxnetphuawlNo ratings yet

- Phillip Research Note 10 July 2017Document9 pagesPhillip Research Note 10 July 2017phuawlNo ratings yet

- IFAST 2Q2017 Result AnnouncementDocument22 pagesIFAST 2Q2017 Result AnnouncementphuawlNo ratings yet

- BasfDocument4 pagesBasfHimanshuNo ratings yet

- S-Reits Offer Sustainable Income - Schroders, Companies & Markets - The BUSINESS TIMESDocument1 pageS-Reits Offer Sustainable Income - Schroders, Companies & Markets - The BUSINESS TIMESphuawlNo ratings yet

- Banks A Bright Spot in Dull Singapore Stock Market, Companies & Markets - The BUSINESS TIMESDocument3 pagesBanks A Bright Spot in Dull Singapore Stock Market, Companies & Markets - The BUSINESS TIMESphuawlNo ratings yet

- HDB Flats Are Still Nest Eggs For Future Retirement Needs - Lawrence Wong, Housing News & Top Stories - The Straits TimesDocument3 pagesHDB Flats Are Still Nest Eggs For Future Retirement Needs - Lawrence Wong, Housing News & Top Stories - The Straits TimesphuawlNo ratings yet

- Brokers' Take, Companies & Markets - The BUSINESS TIMESDocument2 pagesBrokers' Take, Companies & Markets - The BUSINESS TIMESphuawlNo ratings yet

- Private Non-Landed Resale Volumes Surge in March, Prices Inch Higher - SRX, Real Estate - The BUSINESS TIMESDocument2 pagesPrivate Non-Landed Resale Volumes Surge in March, Prices Inch Higher - SRX, Real Estate - The BUSINESS TIMESphuawlNo ratings yet

- Bullish Bidding For Toh Tuck Site, Real Estate - The BUSINESS TIMESDocument2 pagesBullish Bidding For Toh Tuck Site, Real Estate - The BUSINESS TIMESphuawlNo ratings yet

- SGXNET FY2016 - 21feb17Document12 pagesSGXNET FY2016 - 21feb17phuawlNo ratings yet

- Private Home Resale Prices Rise For 5th Straight Month To 2 - Year High in March - SRX Property, Property News & Top Stories - The Straits TimesDocument2 pagesPrivate Home Resale Prices Rise For 5th Straight Month To 2 - Year High in March - SRX Property, Property News & Top Stories - The Straits TimesphuawlNo ratings yet

- Brokers' Take, Companies & Markets - The BUSINESS TIMESDocument2 pagesBrokers' Take, Companies & Markets - The BUSINESS TIMESphuawlNo ratings yet

- Outlook On Currencies - The Straits TimesDocument3 pagesOutlook On Currencies - The Straits TimesphuawlNo ratings yet

- Form 6 - KDCRM 27022017 FinalDocument5 pagesForm 6 - KDCRM 27022017 FinalphuawlNo ratings yet

- Kdcreit PoemsDocument7 pagesKdcreit PoemsphuawlNo ratings yet

- SCI FY2016 Financial StatementsDocument28 pagesSCI FY2016 Financial StatementsphuawlNo ratings yet

- SGX+Securities+Market+Direct+Feed+ (SMDF) +factsheet+ (Eng) +-+mar+2015 D2Document1 pageSGX+Securities+Market+Direct+Feed+ (SMDF) +factsheet+ (Eng) +-+mar+2015 D2phuawlNo ratings yet

- Nobel FY2016ResultsAnnouncement 23-02-2017Document20 pagesNobel FY2016ResultsAnnouncement 23-02-2017phuawlNo ratings yet

- HoBee FSAnnouncement FY2016Document11 pagesHoBee FSAnnouncement FY2016phuawlNo ratings yet

- First Reit OcbcrDocument4 pagesFirst Reit OcbcrphuawlNo ratings yet

- Chapter 4 FinmarDocument12 pagesChapter 4 FinmarhannahNo ratings yet

- Bank of Credit and Commerce InternationalDocument9 pagesBank of Credit and Commerce InternationalMd. FaysalNo ratings yet

- Business TranslationDocument154 pagesBusiness TranslationBdour AlfalahNo ratings yet

- PayPal - Asia - Research - Report - Digital - Payments - Thinking Beyond TransactionsDocument22 pagesPayPal - Asia - Research - Report - Digital - Payments - Thinking Beyond TransactionsClara LilaNo ratings yet

- Finance Current Affairs March RevisionDocument47 pagesFinance Current Affairs March RevisionRte FrthNo ratings yet

- Bank of Credit and Commerce (Bcci)Document13 pagesBank of Credit and Commerce (Bcci)Shah Jamal100% (2)

- CIMBClicksDocument39 pagesCIMBClicksVaishnavi KrishnanNo ratings yet

- Assignment of Islamic BankingDocument21 pagesAssignment of Islamic BankingSadia 55No ratings yet

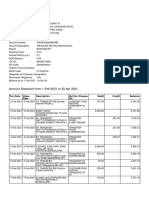

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiNo ratings yet

- N SpecDocument61 pagesN SpecJonathan GalorioNo ratings yet

- Account Statement: 4445935743 Bhayander (W)Document17 pagesAccount Statement: 4445935743 Bhayander (W)Nitin kumar SinghNo ratings yet

- Earnings Before Interest and Depreciation (EBID) : What It IsDocument2 pagesEarnings Before Interest and Depreciation (EBID) : What It IsNaman VermaNo ratings yet

- Negotiable Instrument NotesDocument5 pagesNegotiable Instrument NotesJoshua UmaliNo ratings yet

- International Finance Ass.Document4 pagesInternational Finance Ass.SahelNo ratings yet

- To Whom It May ConcernDocument52 pagesTo Whom It May ConcernBabu KhanNo ratings yet

- Precise DIY Metro2 Credit Ebook (DC17 - )Document16 pagesPrecise DIY Metro2 Credit Ebook (DC17 - )Tbonds67% (6)

- Account Statement For The Account: 0955010172400: Branch DetailsDocument15 pagesAccount Statement For The Account: 0955010172400: Branch DetailsANIL MANDINo ratings yet

- Loans On Bottomry and RespondentiaDocument15 pagesLoans On Bottomry and RespondentiaAgnes Francisco100% (2)

- EECODocument6 pagesEECOJohnNo ratings yet

- Bsa1acash and Cash Equivalents For Discussion PurposesDocument12 pagesBsa1acash and Cash Equivalents For Discussion PurposesSafe PlaceNo ratings yet

- Banking Project FinalDocument17 pagesBanking Project Finalnimitajinjala27No ratings yet

- Time Value - Future ValueDocument4 pagesTime Value - Future ValueSCRBDusernmNo ratings yet

- XXXXXXXXXXX0788-01-01-2022to31-07-2023 ASHUDocument3 pagesXXXXXXXXXXX0788-01-01-2022to31-07-2023 ASHUashokchaturvedi1990No ratings yet

- CGAP MFI Appraise WorksheetDocument85 pagesCGAP MFI Appraise WorksheetleekosalNo ratings yet

- BDO Unibank: H1 Statement of ConditionDocument1 pageBDO Unibank: H1 Statement of ConditionBusinessWorldNo ratings yet

- 04 - Bank Mandiri A Case in Strategic TransformationDocument13 pages04 - Bank Mandiri A Case in Strategic TransformationEka DarmadiNo ratings yet

- Byf Student Book 1 MoneyDocument36 pagesByf Student Book 1 MoneyVikasNo ratings yet

- Horizontal Vertical AnalysisDocument4 pagesHorizontal Vertical AnalysisAhmedNo ratings yet

- Discuss The Role of Banking System in Economic Growth and Development of IndiaDocument5 pagesDiscuss The Role of Banking System in Economic Growth and Development of IndiaNaruChoudharyNo ratings yet

- HSBC Add-On Credit Card Application: Primary Credit Cardholder DetailsDocument2 pagesHSBC Add-On Credit Card Application: Primary Credit Cardholder DetailsPrabudh BansalNo ratings yet