You might also like

- Meaning of Money Refers To The Definition of MoneyDocument2 pagesMeaning of Money Refers To The Definition of Moneyanon_485365916No ratings yet

- Case Study of Sunlight Industries LTD: SolutionDocument3 pagesCase Study of Sunlight Industries LTD: Solutionparv guptaNo ratings yet

- 5-Niif-9-Instrumentos-Financieros Libro Rojo PDFDocument88 pages5-Niif-9-Instrumentos-Financieros Libro Rojo PDFmlarrotasNo ratings yet

- IgniteDocument4 pagesIgniteTarunVarmaNo ratings yet

- CHAPTER 16 Industry Life CyclesDocument23 pagesCHAPTER 16 Industry Life Cyclesjason padulNo ratings yet

- Delta Hedging Dayton ManufacturingDocument10 pagesDelta Hedging Dayton ManufacturingMeet JivaniNo ratings yet

- Classification and Regression Trees (CART) Theory and ApplicationsDocument40 pagesClassification and Regression Trees (CART) Theory and ApplicationsKiran Kumar KuppaNo ratings yet

- Hanson CaseDocument11 pagesHanson Casegharelu10No ratings yet

- HomeworkDocument8 pagesHomeworkEnrique Feliciano Cornejo50% (2)

- Financial Lemonade: Refresh Your Wellbeing Thru Managing Personal FinanceDocument40 pagesFinancial Lemonade: Refresh Your Wellbeing Thru Managing Personal FinanceConrado Delos Reyes Jr.No ratings yet

- Foreign Exchange MarketDocument73 pagesForeign Exchange MarketAmit Sinha100% (1)

- Contents of IntermarketDocument12 pagesContents of IntermarketBảo KhánhNo ratings yet

- Tweezer TopDocument5 pagesTweezer Topkarthick sudharsanNo ratings yet

- Fuel Studies PDFDocument78 pagesFuel Studies PDFLance Vidal RiegoNo ratings yet

- Fundamental and Technical AnalysisDocument19 pagesFundamental and Technical AnalysisKarthi KeyanNo ratings yet

- Technical Analysis EnglishDocument30 pagesTechnical Analysis EnglishRAJESH KUMARNo ratings yet

- Technical Analysis: Urali ArkataliDocument34 pagesTechnical Analysis: Urali ArkataliTalal AnsariNo ratings yet

- Introduction To Active Portfolio ManagementDocument26 pagesIntroduction To Active Portfolio Managementsanjith6371No ratings yet

- Lecture 4-Hedging With FuturesDocument36 pagesLecture 4-Hedging With FuturesNIAZ ALI KHANNo ratings yet

- Delgado - Forex: The Fundamental Analysis.Document10 pagesDelgado - Forex: The Fundamental Analysis.Franklin Delgado VerasNo ratings yet

- Bond Risks and Yield Curve AnalysisDocument33 pagesBond Risks and Yield Curve Analysisarmando.chappell1005No ratings yet

- International Monetary SystemDocument7 pagesInternational Monetary SystemAmethyst NocelladoNo ratings yet

- International Stock Exchanges WorldwideDocument5 pagesInternational Stock Exchanges WorldwideNilesh MandlikNo ratings yet

- Macro Ecnomics Full Revision PDFDocument17 pagesMacro Ecnomics Full Revision PDFharshit kalra0% (1)

- A Presentation On: International Finance Instruments and IntricaciesDocument118 pagesA Presentation On: International Finance Instruments and IntricaciesRahul GuptaNo ratings yet

- Determine The Impact of Business Cycles On Business ActivitiesDocument19 pagesDetermine The Impact of Business Cycles On Business ActivitiesChitra RajeshNo ratings yet

- Forward: Muhammad The Prophet of IslamDocument17 pagesForward: Muhammad The Prophet of IslamSajid QureshiNo ratings yet

- International Monetary SystemsDocument19 pagesInternational Monetary SystemsIdrees BharatNo ratings yet

- FX Startegies CompressDocument26 pagesFX Startegies CompressHendra SetiawanNo ratings yet

- World's Most Powerful Stock Market RulesDocument62 pagesWorld's Most Powerful Stock Market RulesShreePanickerNo ratings yet

- Beta Leverage and The Cost of CapitalDocument3 pagesBeta Leverage and The Cost of CapitalpumaguaNo ratings yet

- Financial Market Capital Market and Money Market Capital MarketDocument30 pagesFinancial Market Capital Market and Money Market Capital MarketEnayetullah RahimiNo ratings yet

- Advanced Trading Course Vol.1 Introduction To Fractal TradingDocument8 pagesAdvanced Trading Course Vol.1 Introduction To Fractal TradingMohamedNo ratings yet

- Strategy Portfolio: Dravyaniti Consulting LLPDocument13 pagesStrategy Portfolio: Dravyaniti Consulting LLPChidambara StNo ratings yet

- Forecasting Usd - Euro Ex Rates Using ARMA ModelDocument13 pagesForecasting Usd - Euro Ex Rates Using ARMA ModelNavin Poddar100% (1)

- Zahar Udin PHD ThesisDocument201 pagesZahar Udin PHD ThesisSunny ChaturvediNo ratings yet

- Chapter 1 Spot Exchange MarketDocument20 pagesChapter 1 Spot Exchange Marketchaman_shrestha100% (2)

- Chart Patterns Double Tops BottomsDocument9 pagesChart Patterns Double Tops BottomsJeremy NealNo ratings yet

- Impact of Inflation and Its Effects On Karachi Stock Exchange (Kse)Document9 pagesImpact of Inflation and Its Effects On Karachi Stock Exchange (Kse)Anonymous uY667INo ratings yet

- International Finance: Factors Affecting Foreign Exchange RatesDocument8 pagesInternational Finance: Factors Affecting Foreign Exchange Ratesvan_1234100% (1)

- 5 Hidden Secrets About Stock Market That You Can't Learn From Books - by Indrazith Shantharaj - May, 2022 - MediumDocument10 pages5 Hidden Secrets About Stock Market That You Can't Learn From Books - by Indrazith Shantharaj - May, 2022 - MediumArun KumarNo ratings yet

- Economic IndicatorsDocument6 pagesEconomic IndicatorsChenny Marie AdanNo ratings yet

- Dean's Statement: Guidance For ApplicantsDocument3 pagesDean's Statement: Guidance For ApplicantsSarina PromthongNo ratings yet

- A Project Reort On Technical Analysis OF Tata-MotorsDocument11 pagesA Project Reort On Technical Analysis OF Tata-MotorsSahil ChhibberNo ratings yet

- Planning Your Trades: Risk Management RiskDocument2 pagesPlanning Your Trades: Risk Management RiskdoremonNo ratings yet

- Fundamental AnalysisDocument6 pagesFundamental AnalysisLiu Jin RongNo ratings yet

- Evidence For Mean Reversion in Equity PricesDocument6 pagesEvidence For Mean Reversion in Equity Pricesmirando93No ratings yet

- 1 Liquidity RiskDocument8 pages1 Liquidity RiskShreyanko GhosalNo ratings yet

- 4 Different Types of Losses in Transformer - CalculationDocument23 pages4 Different Types of Losses in Transformer - CalculationFahadKhanNo ratings yet

- Synopsis of Indian Derivatives MarketDocument6 pagesSynopsis of Indian Derivatives MarketEhsaan IllahiNo ratings yet

- Long Term Capital ManagementDocument49 pagesLong Term Capital ManagementLiu Shuang100% (2)

- Top 10 Drivers For OutsourcingDocument2 pagesTop 10 Drivers For OutsourcingGeetha Srinivas Pasupulati100% (1)

- A Conceptual Framework of Online Shopping Intention and E - Purchase HabitDocument3 pagesA Conceptual Framework of Online Shopping Intention and E - Purchase HabitVince Villamin SatinNo ratings yet

- Business Cycles (BBA BI)Document19 pagesBusiness Cycles (BBA BI)Yograj PandeyaNo ratings yet

- Goldman Sachs 2022Document264 pagesGoldman Sachs 2022Ogbu VincentNo ratings yet

- Stock SelectionDocument32 pagesStock SelectionMonchai PhaichitchanNo ratings yet

- Investors Preference in Share MTDocument87 pagesInvestors Preference in Share MTravikumarreddytNo ratings yet

- Chapter 08 Stock ValuationDocument34 pagesChapter 08 Stock Valuationfiq8809No ratings yet

- Customs ActDocument43 pagesCustoms ActAbhishek AgarwalNo ratings yet

- SSRN Id3596245 PDFDocument64 pagesSSRN Id3596245 PDFAkil LawyerNo ratings yet

- Foreign Exchange Market Intervention: Amie Colgan, Mary Deely, Fergus Colleran, Anna NikolskayaDocument19 pagesForeign Exchange Market Intervention: Amie Colgan, Mary Deely, Fergus Colleran, Anna Nikolskayamanavdce1986No ratings yet

- Fundamental Analysis of EquityDocument14 pagesFundamental Analysis of EquityJai RoxNo ratings yet

- 3 3 Price PatternsDocument15 pages3 3 Price PatternsSMO979No ratings yet

- FX Markets and Exchange RatesDocument15 pagesFX Markets and Exchange RatesKath LeynesNo ratings yet

- Evolutionary Game TheoryDocument28 pagesEvolutionary Game TheoryKiran Kumar KuppaNo ratings yet

- Political Islam - An Evolutionary HistoryDocument29 pagesPolitical Islam - An Evolutionary HistoryKiran Kumar KuppaNo ratings yet

- Trading Justice For MoneyDocument15 pagesTrading Justice For MoneyKiran Kumar KuppaNo ratings yet

- Anti Americanism in Pakistan - A Brief HistoryDocument11 pagesAnti Americanism in Pakistan - A Brief HistoryKiran Kumar KuppaNo ratings yet

- The Lambda CalculusDocument23 pagesThe Lambda CalculusKiran Kumar Kuppa100% (1)

- The Asymmetric Dialog of CivilizationsDocument7 pagesThe Asymmetric Dialog of CivilizationsKiran Kumar KuppaNo ratings yet

- Economics and Optimization TechniquesDocument163 pagesEconomics and Optimization TechniquesKiran KuppaNo ratings yet

- An Open Letter To Moderate MuslimsDocument9 pagesAn Open Letter To Moderate MuslimsKiran Kumar KuppaNo ratings yet

- Healing Our Sectarian DivideDocument3 pagesHealing Our Sectarian DivideKiran Kumar KuppaNo ratings yet

- Python Scientific TutorialDocument139 pagesPython Scientific TutorialpietoesNo ratings yet

- The Root of India-Pakistan ConflictsDocument11 pagesThe Root of India-Pakistan ConflictsKiran Kumar KuppaNo ratings yet

- Finite State AutomataDocument21 pagesFinite State AutomataKiran Kumar Kuppa100% (1)

- The Untold Story of Pakistan's Blasphemy LawDocument4 pagesThe Untold Story of Pakistan's Blasphemy LawKiran Kumar KuppaNo ratings yet

- The Lack of - Design Patterns in Python PresentationDocument68 pagesThe Lack of - Design Patterns in Python PresentationossjunkieNo ratings yet

- Mathematics UPIL CatalogueDocument62 pagesMathematics UPIL CatalogueKiran Kumar KuppaNo ratings yet

- Regression Trees With Classification (CART)Document72 pagesRegression Trees With Classification (CART)Kiran Kumar KuppaNo ratings yet

- JavaScript Security PresentationDocument89 pagesJavaScript Security PresentationKiran Kumar KuppaNo ratings yet

- Solving RecurrencesDocument67 pagesSolving RecurrencesDanh NguyenNo ratings yet

- Station IslandDocument246 pagesStation Islandpiej1209No ratings yet

- InnovatiInnovations in Payment Technologiesons in Payment TechnologiesDocument14 pagesInnovatiInnovations in Payment Technologiesons in Payment Technologiessachdevaanuj765No ratings yet

- Principles of Actuarial ScienceDocument256 pagesPrinciples of Actuarial ScienceanthonykogeyNo ratings yet

- Future Adaptable Password Scheme (Bcrypt)Document13 pagesFuture Adaptable Password Scheme (Bcrypt)Kiran Kumar KuppaNo ratings yet

- Amazing Properties of Bionomial CoefficientsDocument23 pagesAmazing Properties of Bionomial CoefficientsKiran Kumar KuppaNo ratings yet

- Dos and Dont's For Portable Android User InterfacesDocument95 pagesDos and Dont's For Portable Android User InterfacesKiran Kumar KuppaNo ratings yet

- The Rhetoric of TypographyDocument18 pagesThe Rhetoric of TypographyKiran Kumar KuppaNo ratings yet

- Electronic Payment SystemsDocument111 pagesElectronic Payment SystemsRamakrishnan AlagarsamyNo ratings yet

- Combinatorial EnumerationDocument54 pagesCombinatorial EnumerationKiran Kumar KuppaNo ratings yet

- The Idea of Pakistan (Stephen Cohen) PDFDocument396 pagesThe Idea of Pakistan (Stephen Cohen) PDFRana Sandrocottus100% (1)

- Firstpost Book, Prime Minister Narendra ModiDocument39 pagesFirstpost Book, Prime Minister Narendra ModiKiran Kumar KuppaNo ratings yet

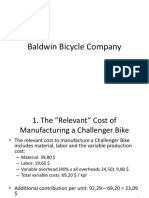

- Baldwin Bicycle Company EngDocument8 pagesBaldwin Bicycle Company EngChayan Kothari IDD,Biochem, IT-BHU, Varanasi (INDIA)No ratings yet

- Ninjatrader Futures CommissionsDocument3 pagesNinjatrader Futures CommissionsDaniel Diogenes SousaNo ratings yet

- Loan Calculator With Extra Payments: Enter ValuesDocument24 pagesLoan Calculator With Extra Payments: Enter ValuesJames R. BabbNo ratings yet

- Working Capital Management of Rajasthan Cooperative Dairy Federation LTD in India PDFDocument6 pagesWorking Capital Management of Rajasthan Cooperative Dairy Federation LTD in India PDFSk NagoorNo ratings yet

- Materi Presentasi Blue BirdDocument39 pagesMateri Presentasi Blue BirdwondoajaNo ratings yet

- The Global Cost and Availability of CapitalDocument41 pagesThe Global Cost and Availability of CapitalayurishiNo ratings yet

- Asset ValuationDocument3 pagesAsset ValuationHassanRana0% (1)

- Short SOPDocument1 pageShort SOPManas DimriNo ratings yet

- Harmonic Trader IntroDocument2 pagesHarmonic Trader IntroBiantoroKunartoNo ratings yet

- PT Option Trader PerformanceDocument45 pagesPT Option Trader PerformanceAdigoppula NarsaiahNo ratings yet

- Turnaround Management An Overview For MBADocument36 pagesTurnaround Management An Overview For MBAlnpillai75% (4)

- Measurement Models For Market Risk Management in NigeriaDocument11 pagesMeasurement Models For Market Risk Management in NigeriaBOHR International Journal of Financial market and Corporate Finance (BIJFMCF)No ratings yet

- Jade Group: Company ProfileDocument18 pagesJade Group: Company Profilesajd1No ratings yet

- Financial InstrumentsDocument8 pagesFinancial Instrumentscretuiulia1984No ratings yet

- Sip PDFDocument81 pagesSip PDFMayuri TetwarNo ratings yet

- Hedge Fund ActivismDocument17 pagesHedge Fund ActivismjamesNo ratings yet

- Uttara Bank Mba ReportDocument36 pagesUttara Bank Mba ReportAbu Rasel Mia100% (1)

- Micro-Cap Review Magazine Fall 2010Document80 pagesMicro-Cap Review Magazine Fall 2010Planet MicroCap Review MagazineNo ratings yet

- About Union Bank: Acquisition of Emirates Bank InternationalDocument47 pagesAbout Union Bank: Acquisition of Emirates Bank Internationalapi-19759801No ratings yet

- Derivatives Market: DR L.Krishna VeniDocument14 pagesDerivatives Market: DR L.Krishna VeniDinesh MunjetiNo ratings yet

- Foreign Exchange ManagementDocument11 pagesForeign Exchange ManagementVinit MehtaNo ratings yet

- Institutional Price Action TopicsDocument9 pagesInstitutional Price Action Topicsudaya kumarNo ratings yet

- Pitchfork Trader Vol3 - ExcerptsDocument42 pagesPitchfork Trader Vol3 - Excerptsmr.ajeetsingh100% (1)

- Candlestick Pattern Full PDFDocument25 pagesCandlestick Pattern Full PDFM Try Trader Kaltim80% (5)

- Buy Call: Top 9 Trading Strategies in DerivativesDocument12 pagesBuy Call: Top 9 Trading Strategies in DerivativesAmit KumarNo ratings yet