You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 0010a Kill Them With Paper WorkDocument21 pages0010a Kill Them With Paper Workrhouse_192% (12)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Jose Ferreira Criminal ComplaintDocument4 pagesJose Ferreira Criminal ComplaintDavid Lohr100% (1)

- Security Awareness TrainingDocument95 pagesSecurity Awareness TrainingChandra RaoNo ratings yet

- 1 - Instructions - Enforcement ProcessDocument5 pages1 - Instructions - Enforcement Processrhouse_1No ratings yet

- William Cooper HOTT Facts Expose of IRS Fraudulent RacketeeringDocument272 pagesWilliam Cooper HOTT Facts Expose of IRS Fraudulent Racketeeringrhouse_1No ratings yet

- 0001 Cheryl Wiker-Affirmation of National-As Amended 05.19.2014 PDFDocument4 pages0001 Cheryl Wiker-Affirmation of National-As Amended 05.19.2014 PDFrhouse_1No ratings yet

- Federalist Papers 15Document1 pageFederalist Papers 15rhouse_1No ratings yet

- 0001 When You Are BornDocument3 pages0001 When You Are Bornrhouse_1100% (2)

- Federalist Papers 15Document1 pageFederalist Papers 15rhouse_1No ratings yet

- DwightAvis-TaxVoluntaryDocument3 pagesDwightAvis-TaxVoluntaryrhouse_1No ratings yet

- Federal Jurisdiction Tax Question AnsweredfedjurisdictionDocument2 pagesFederal Jurisdiction Tax Question Answeredfedjurisdictionrhouse_1No ratings yet

- 26CFR1 871-1Document1 page26CFR1 871-1rhouse_1No ratings yet

- Avis Testimony Feb 53Document3 pagesAvis Testimony Feb 53rhouse_1No ratings yet

- Definition VoluntaryDocument1 pageDefinition Voluntaryrhouse_1No ratings yet

- LegalBasisForTermNRAlien PDFDocument0 pagesLegalBasisForTermNRAlien PDFmatador13thNo ratings yet

- Eye of The Eagle Volume 1 Number 5Document12 pagesEye of The Eagle Volume 1 Number 5rhouse_1No ratings yet

- 0002a Legisl Intent 16thaDocument3 pages0002a Legisl Intent 16tharhouse_1No ratings yet

- CDP Hearing RequestDocument4 pagesCDP Hearing Requestrhouse_1No ratings yet

- 0005b SampleaDocument1 page0005b Samplearhouse_1No ratings yet

- Steps To Terminate IRS 668 Notice of LienDocument10 pagesSteps To Terminate IRS 668 Notice of Lienrhouse_1100% (3)

- 0005c SamplebDocument1 page0005c Samplebrhouse_1No ratings yet

- Jurisdiction Is The Key FactorDocument6 pagesJurisdiction Is The Key Factorrhouse_1100% (1)

- Notary Verification: Andrea K GindeleDocument1 pageNotary Verification: Andrea K Gindelerhouse_1No ratings yet

- 0002a Legisl Intent 16thaDocument3 pages0002a Legisl Intent 16tharhouse_1No ratings yet

- Power Authority Power PointDocument7 pagesPower Authority Power Pointrhouse_1No ratings yet

- Gov Exists in Two FormsDocument2 pagesGov Exists in Two Formsrhouse_1100% (1)

- 9b Corp Political Society - PsDocument52 pages9b Corp Political Society - Psrhouse_1No ratings yet

- Mecanica Moderna Del Dinero PDFDocument50 pagesMecanica Moderna Del Dinero PDFHarold AponteNo ratings yet

- First Estate Comprehensive DiagramDocument1 pageFirst Estate Comprehensive Diagramrhouse_1No ratings yet

- Treatise SovereigntyDocument46 pagesTreatise Sovereignty1 watchman100% (1)

- 9 Natural Order - PsDocument53 pages9 Natural Order - Psrhouse_1100% (1)

- Lesson Plan Curriculum IntegrationDocument12 pagesLesson Plan Curriculum Integrationapi-509185462No ratings yet

- Um Tagum CollegeDocument12 pagesUm Tagum Collegeneil0522No ratings yet

- Lesson 2 - BasicDocument7 pagesLesson 2 - BasicMichael MccormickNo ratings yet

- Difference Between Reptiles and Amphibians????Document2 pagesDifference Between Reptiles and Amphibians????vijaybansalfetNo ratings yet

- Seryu Cargo Coret CoreDocument30 pagesSeryu Cargo Coret CoreMusicer EditingNo ratings yet

- AR Reserve Invoice - 20005152 - 20200609 - 094424Document1 pageAR Reserve Invoice - 20005152 - 20200609 - 094424shady masoodNo ratings yet

- FM - Amreli Nagrik Bank - 2Document84 pagesFM - Amreli Nagrik Bank - 2jagrutisolanki01No ratings yet

- Toms River Fair Share Housing AgreementDocument120 pagesToms River Fair Share Housing AgreementRise Up Ocean CountyNo ratings yet

- This PDF by Stockmock - in Is For Personal Use Only. Do Not Share With OthersDocument4 pagesThis PDF by Stockmock - in Is For Personal Use Only. Do Not Share With OthersPdffNo ratings yet

- Account Statement 2012 August RONDocument5 pagesAccount Statement 2012 August RONAna-Maria DincaNo ratings yet

- Wa0256.Document3 pagesWa0256.Daniela Daza HernándezNo ratings yet

- Analysis of Chapter 8 of Positive Psychology By::-Alan CarrDocument3 pagesAnalysis of Chapter 8 of Positive Psychology By::-Alan CarrLaiba HaroonNo ratings yet

- Letter of Appeal Pacheck Kay Tita ConnieDocument2 pagesLetter of Appeal Pacheck Kay Tita ConnieNikko Avila IgdalinoNo ratings yet

- Terminal Injustice - Ambush AttackDocument2 pagesTerminal Injustice - Ambush AttackAllen Carlton Jr.No ratings yet

- LAZ PAPER Ethics Ethical Conduct Challenges and Opportunities in Modern PracticeDocument15 pagesLAZ PAPER Ethics Ethical Conduct Challenges and Opportunities in Modern PracticenkwetoNo ratings yet

- Fundamentals of Accounting I Accounting For Manufacturing BusinessDocument14 pagesFundamentals of Accounting I Accounting For Manufacturing BusinessBenedict rivera100% (2)

- Department of Environment and Natural Resources: Niño E. Dizor Riza Mae Dela CruzDocument8 pagesDepartment of Environment and Natural Resources: Niño E. Dizor Riza Mae Dela CruzNiño Esco DizorNo ratings yet

- Principles of ManagementDocument107 pagesPrinciples of ManagementalchemistNo ratings yet

- Quotation 017-2019 - 01-07-2019Document8 pagesQuotation 017-2019 - 01-07-2019Venkatesan ManikandanNo ratings yet

- Municipal Development Plan 1996 - 2001Document217 pagesMunicipal Development Plan 1996 - 2001TineNo ratings yet

- Hymns by John Henry NewmanDocument286 pagesHymns by John Henry Newmanthepillquill100% (1)

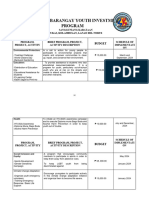

- Annual Barangay Youth Investment ProgramDocument4 pagesAnnual Barangay Youth Investment ProgramBarangay MukasNo ratings yet

- Luke 1.1-56 Intros & SummariesDocument8 pagesLuke 1.1-56 Intros & SummariesdkbusinessNo ratings yet

- Course SyllabusDocument9 pagesCourse SyllabusJae MadridNo ratings yet

- GAAR Slide Deck 13072019Document38 pagesGAAR Slide Deck 13072019Sandeep GolaniNo ratings yet

- Juarez, Jenny Brozas - Activity 2 MidtermDocument4 pagesJuarez, Jenny Brozas - Activity 2 MidtermJenny Brozas JuarezNo ratings yet

- Bài Tập Tiếng Anh Cho Người Mất GốcDocument8 pagesBài Tập Tiếng Anh Cho Người Mất GốcTrà MyNo ratings yet

- Nature of Vat RefundDocument7 pagesNature of Vat RefundRoselyn NaronNo ratings yet