You might also like

- Fiduciary Handbook for Understanding and Selecting Target Date Funds: It's All About the BeneficiariesFrom EverandFiduciary Handbook for Understanding and Selecting Target Date Funds: It's All About the BeneficiariesNo ratings yet

- RIN 1210-AB33 Page I of 10 PagesDocument10 pagesRIN 1210-AB33 Page I of 10 PagescheaussieNo ratings yet

- See 76 Fed. Reg. 8068 (Feb. 11, 2011) (The "Joint Proposing Release")Document9 pagesSee 76 Fed. Reg. 8068 (Feb. 11, 2011) (The "Joint Proposing Release")MarketsWikiNo ratings yet

- Via Electronic Mail:: April 24, 2012Document6 pagesVia Electronic Mail:: April 24, 2012MarketsWikiNo ratings yet

- Chapter 12 IMSMDocument19 pagesChapter 12 IMSMZachary Thomas CarneyNo ratings yet

- Case Study 1Document5 pagesCase Study 1Tameran Bruch100% (1)

- Sarbanes Oxley News May 2011Document21 pagesSarbanes Oxley News May 2011George LekatisNo ratings yet

- SarbanesDocument16 pagesSarbanessreedhar72No ratings yet

- Re: Announcement Regarding Rule 14a-8 (I)Document4 pagesRe: Announcement Regarding Rule 14a-8 (I)api-249785899No ratings yet

- Financial Reporting and The Securities and Exchange CommissionDocument18 pagesFinancial Reporting and The Securities and Exchange CommissionJordan YoungNo ratings yet

- Fmu NPR FinalDocument63 pagesFmu NPR FinalMarketsWikiNo ratings yet

- ESOPs What They Are and How They WorkDocument60 pagesESOPs What They Are and How They WorkYuliana TungabdiNo ratings yet

- Research Paper On 401kDocument4 pagesResearch Paper On 401kgw15ws8j100% (1)

- Apr 07 Dip Pi Is Pre PortDocument7 pagesApr 07 Dip Pi Is Pre PortJamie ZueNo ratings yet

- Law of Torts: Name: Nikhil Gupta. BATCH: BALLB 2020-2025. STUDENT NUMBER: 81012019148Document27 pagesLaw of Torts: Name: Nikhil Gupta. BATCH: BALLB 2020-2025. STUDENT NUMBER: 81012019148Vansh SharmaNo ratings yet

- The Sarbanes-Oxley Act: Summary of Section 302Document4 pagesThe Sarbanes-Oxley Act: Summary of Section 302Mustafa BahramiNo ratings yet

- Via EmailDocument38 pagesVia EmailMarketsWikiNo ratings yet

- 43-JORP - 10-03-07 - Morrow (May 15, 2009)Document15 pages43-JORP - 10-03-07 - Morrow (May 15, 2009)ldelde777No ratings yet

- Tax-Exempt Bonds For 501 (C)Document12 pagesTax-Exempt Bonds For 501 (C)victoria medinaNo ratings yet

- Via Email FilingDocument4 pagesVia Email FilingMarketsWikiNo ratings yet

- FRM 2016 Part 1 Revision CourseDocument4 pagesFRM 2016 Part 1 Revision CoursemohamedNo ratings yet

- s70511 29Document8 pagess70511 29MarketsWikiNo ratings yet

- Avoid The Pending Tax Disaster Facing Employer-Owned Life InsuranceDocument11 pagesAvoid The Pending Tax Disaster Facing Employer-Owned Life InsuranceSheilaAlcaparazDelaCruzNo ratings yet

- 401 (K) Plan The Complete GuideDocument6 pages401 (K) Plan The Complete Guide9xw8phvcm4No ratings yet

- ProspectusDocument9 pagesProspectusRakesh BhoirNo ratings yet

- Mitigation of Conflicts of Interest: 75 FR 63732 (Oct. 18, 2010)Document7 pagesMitigation of Conflicts of Interest: 75 FR 63732 (Oct. 18, 2010)MarketsWikiNo ratings yet

- House Bill 4164: New Sections Are in Boldfaced TypeDocument17 pagesHouse Bill 4164: New Sections Are in Boldfaced TypeStatesman JournalNo ratings yet

- Ass 2Document5 pagesAss 2albert cumabigNo ratings yet

- RBC Wealth Management Comment LetterDocument16 pagesRBC Wealth Management Comment LetterMeganLeonhardtNo ratings yet

- 2011-10-03 Garrett Letter To Schapiro Net Equity Reconsideration (N0003034)Document3 pages2011-10-03 Garrett Letter To Schapiro Net Equity Reconsideration (N0003034)Investor ProtectionNo ratings yet

- Life After CPO Registration Select CFTC and NFA Compliance Obligations That Lie Ahead - 11 Mar 13Document12 pagesLife After CPO Registration Select CFTC and NFA Compliance Obligations That Lie Ahead - 11 Mar 13m3nycpeterNo ratings yet

- s73610 32Document7 pagess73610 32MarketsWikiNo ratings yet

- T 2-P A E, T P L BT, P P T M B T P A S D P R I M - PDocument23 pagesT 2-P A E, T P L BT, P P T M B T P A S D P R I M - PMarketsWikiNo ratings yet

- Melissa MacgregorDocument18 pagesMelissa MacgregorMarketsWikiNo ratings yet

- Crowdfunding Regulation SummaryDocument25 pagesCrowdfunding Regulation SummaryAnonymous ukqEbKTNo ratings yet

- FAS 140 Setoff Isolation Letter 51004 PDFDocument15 pagesFAS 140 Setoff Isolation Letter 51004 PDFMikhael Yah-Shah Dean: Veilour100% (1)

- Sifma': Invested in AmericaDocument19 pagesSifma': Invested in AmericaMarketsWikiNo ratings yet

- Roth 401 (K) Plans For Private Equity PositionsDocument8 pagesRoth 401 (K) Plans For Private Equity PositionsThree Bell CapitalNo ratings yet

- SEC Whistleblower Practice GuideDocument41 pagesSEC Whistleblower Practice GuideBen Tugendstein100% (1)

- Houseman - Corporate Law - 71UTorontoFacLRev28Document49 pagesHouseman - Corporate Law - 71UTorontoFacLRev28May2014PresentationNo ratings yet

- CH 4Document6 pagesCH 4Mona Adila PardedeNo ratings yet

- Commentary Great West v. KnudsonDocument40 pagesCommentary Great West v. KnudsonEd ClintonNo ratings yet

- Econo Legal Opinion On A Series A Investment in A Startup 1591528511Document31 pagesEcono Legal Opinion On A Series A Investment in A Startup 1591528511ShekinahNo ratings yet

- What Is A 401Document6 pagesWhat Is A 401KidMonkey2299No ratings yet

- Carl B. Wilkerson: Vice President & Chief Counsel Securities & Litigation (202) 624-2118 T (866) 953-4096 FDocument4 pagesCarl B. Wilkerson: Vice President & Chief Counsel Securities & Litigation (202) 624-2118 T (866) 953-4096 FMarketsWikiNo ratings yet

- 2020 SEC Whistleblower Practice GuideDocument43 pages2020 SEC Whistleblower Practice GuideBen Tugendstein100% (2)

- Schiff Hardin Derivatives & Futures Update (May 2012)Document12 pagesSchiff Hardin Derivatives & Futures Update (May 2012)mfearonNo ratings yet

- Actuarial MethodsDocument30 pagesActuarial MethodsOmar Garcia FloresNo ratings yet

- CDA MC 2015-06 Philippine Financial Reporting Framework CooperativesDocument87 pagesCDA MC 2015-06 Philippine Financial Reporting Framework CooperativesJon DonNo ratings yet

- Eb 14-11Document7 pagesEb 14-11AdminAliNo ratings yet

- Chapter 5 - Social Insurance: Project and Program Issues: 13883-Asia - Book Page 183 Tuesday, December 11, 2001 11:37 AMDocument51 pagesChapter 5 - Social Insurance: Project and Program Issues: 13883-Asia - Book Page 183 Tuesday, December 11, 2001 11:37 AMraviNo ratings yet

- Morgan Lewis Private Offering Dos and Dont'sDocument6 pagesMorgan Lewis Private Offering Dos and Dont'sB.C. MoonNo ratings yet

- Fintech Alliance Position Paper (SEC Sandbox)Document3 pagesFintech Alliance Position Paper (SEC Sandbox)Jason YinNo ratings yet

- Ab 2506Document8 pagesAb 2506Scott DauenhauerNo ratings yet

- Fundamental Ethical and Professional Principles (A) : Acca Strategic Business Reporting (SBR)Document109 pagesFundamental Ethical and Professional Principles (A) : Acca Strategic Business Reporting (SBR)Pratham BarotNo ratings yet

- Private Sector Vs Public Sector 2Document8 pagesPrivate Sector Vs Public Sector 2Christine GandiNo ratings yet

- Private Wealth: Wealth Management In PracticeFrom EverandPrivate Wealth: Wealth Management In PracticeRating: 3 out of 5 stars3/5 (1)

- CFIRA Response To Investor Advisory CommitteeDocument3 pagesCFIRA Response To Investor Advisory CommitteeCrowdfundInsiderNo ratings yet

- LSW Non-ERISA TripsDocument2 pagesLSW Non-ERISA TripsScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Fiduciary Duties and Obligations in Administering 457 (B) Plans Under California LawDocument21 pagesFiduciary Duties and Obligations in Administering 457 (B) Plans Under California LawScott Dauenhauer100% (2)

- National Life Group DestinationsDocument6 pagesNational Life Group DestinationsScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- LSW 2018Document2 pagesLSW 2018Scott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Annuity Investors RevealedDocument1 pageAnnuity Investors RevealedScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Annuity CommissionsDocument18 pagesAnnuity CommissionsScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- LSW 2017Document2 pagesLSW 2017Scott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- LSW Advisor ResourcesDocument1 pageLSW Advisor ResourcesScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Ntsa SB 1297Document2 pagesNtsa SB 1297Scott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Teacher PostcardDocument2 pagesTeacher PostcardScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- NLG Sicily Chairman's Club 2016 Qualification FlyerDocument2 pagesNLG Sicily Chairman's Club 2016 Qualification FlyerScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- 2017 Cabos ConferenceDocument2 pages2017 Cabos ConferenceScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- AXA Methodological SummaryDocument6 pagesAXA Methodological SummaryScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- 19586-PS B RetirementPlanTrends HigherEducation LOWREZVIEWONLY FINAL 122315 Tcm73-55252Document32 pages19586-PS B RetirementPlanTrends HigherEducation LOWREZVIEWONLY FINAL 122315 Tcm73-55252Scott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- 457 (B) Awareness MeetingDocument12 pages457 (B) Awareness MeetingScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- MNL Bora Bora 2014Document1 pageMNL Bora Bora 2014Scott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- MNL Costa Rica TripDocument1 pageMNL Costa Rica TripScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- ValuTeachers Letter To SECDocument1 pageValuTeachers Letter To SECScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- MNL Bora Bora 2014Document1 pageMNL Bora Bora 2014Scott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Midland NL Premier Agent ClubDocument16 pagesMidland NL Premier Agent ClubScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

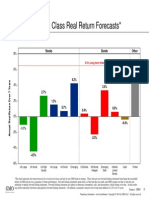

- GMO-Valuation Study and Forward ReturnsDocument8 pagesGMO-Valuation Study and Forward Returnsstreettalk700No ratings yet

- MNL Costa Rica TripDocument1 pageMNL Costa Rica TripScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Midland NL Premier Agent ClubDocument16 pagesMidland NL Premier Agent ClubScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- VL 19724 0510 1 1Document6 pagesVL 19724 0510 1 1Scott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- TDS Aspire LetterDocument8 pagesTDS Aspire LetterScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- GMO 7 Year Asset Forecast - Jan 2014Document1 pageGMO 7 Year Asset Forecast - Jan 2014CanadianValueNo ratings yet

- St. Vrain Plan Transition SummaryDocument2 pagesSt. Vrain Plan Transition SummaryScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- NTSAA Iowa TestimonyDocument16 pagesNTSAA Iowa TestimonyScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Schools First Letter 10-14-09Document2 pagesSchools First Letter 10-14-09Scott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- TDS Group Sued by Former RepDocument66 pagesTDS Group Sued by Former RepScott Dauenhauer, CFP, MSFP, AIFNo ratings yet

- Ranjith Keerikkattil Booz Allen Offer LetterDocument6 pagesRanjith Keerikkattil Booz Allen Offer LetterGeorge RyanNo ratings yet

- Chapter 12 Employee BenefitsDocument8 pagesChapter 12 Employee Benefitsroyalroy_313027733No ratings yet

- 2022 Resume - Dashira CraigDocument2 pages2022 Resume - Dashira Craigapi-592250858No ratings yet

- Salaries in Nestle IndiaDocument3 pagesSalaries in Nestle IndiaNidhi KurianNo ratings yet

- Putnam Individual 401 (K)Document2 pagesPutnam Individual 401 (K)Putnam InvestmentsNo ratings yet

- Human Resource BPODocument7 pagesHuman Resource BPOPouniya ChinnasamyNo ratings yet

- Roth IRADocument2 pagesRoth IRAanon_757121No ratings yet

- MNGT 367 CH 14 MC Answers OnlyDocument14 pagesMNGT 367 CH 14 MC Answers OnlyDyenNo ratings yet

- Main Irs Form W 2 Wage and Tax StatementDocument11 pagesMain Irs Form W 2 Wage and Tax Statementjeffery lamarNo ratings yet

- Business Plan QuestionnaireDocument9 pagesBusiness Plan QuestionnaireoeconomopoulosNo ratings yet

- Nolo's Essential Retirement Tax GuideDocument436 pagesNolo's Essential Retirement Tax GuideabuaasiyahNo ratings yet

- 2018 Personal Financial Literacy Role Play EventsDocument22 pages2018 Personal Financial Literacy Role Play EventsDiana Manzano GuronNo ratings yet

- McKesson Benefits at A GlanceDocument2 pagesMcKesson Benefits at A GlanceKelle SuttonNo ratings yet

- Actuarial Glossary PDFDocument18 pagesActuarial Glossary PDFmiguelNo ratings yet

- Pay Slip TemplateDocument3 pagesPay Slip TemplateSujee HnbaNo ratings yet

- Employee Experience Benchmarking Report © SequoiaDocument36 pagesEmployee Experience Benchmarking Report © SequoiaJoão RibeiroNo ratings yet

- Personal Financial Planning Attitudes: A Preliminary Study of Graduate StudentsDocument7 pagesPersonal Financial Planning Attitudes: A Preliminary Study of Graduate StudentsAlia Suraya AhmadNo ratings yet

- A Doctor's Prescription To Comprehensive Financial WellnessDocument15 pagesA Doctor's Prescription To Comprehensive Financial WellnessHank WeinstockNo ratings yet

- W-2 Wage Reconciliation: This Form Details Your Final 2019 Payroll EarningsDocument2 pagesW-2 Wage Reconciliation: This Form Details Your Final 2019 Payroll EarningsChantale0% (1)

- Adp QUANIC MARTIN-converted (1st Try)Document12 pagesAdp QUANIC MARTIN-converted (1st Try)Quanic Martin100% (1)

- SMChap 013Document49 pagesSMChap 013testbank100% (5)

- Fidelity 401kDocument7 pagesFidelity 401kTom BiusoNo ratings yet

- Don't Let The Breezy, Irreverent Style of This Book Fool YouDocument3 pagesDon't Let The Breezy, Irreverent Style of This Book Fool YouArlind LleshiNo ratings yet

- End of Year Processing GuideDocument90 pagesEnd of Year Processing GuideSubramanianNo ratings yet

- 409A FLOWCHART and OutlineDocument27 pages409A FLOWCHART and OutlineSquireFinancialNo ratings yet

- Understanding Your Paycheck and Tax FormsDocument30 pagesUnderstanding Your Paycheck and Tax FormsdeepagNo ratings yet

- Keon MillerDocument4 pagesKeon MillerKeon MillerNo ratings yet

- Non Negotiable - This Is Not A Check - Non NegotiableDocument1 pageNon Negotiable - This Is Not A Check - Non NegotiableAlexa PribisNo ratings yet

- Net Unrealized Appreciation: The Untold StoryDocument2 pagesNet Unrealized Appreciation: The Untold StoryPhil_OrwigNo ratings yet

- MC 0315Document16 pagesMC 0315mcchronicleNo ratings yet