You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Basic Concepts of Income Tax ActDocument14 pagesBasic Concepts of Income Tax ActRaghu CkNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hra Rule 2aDocument3 pagesHra Rule 2aRaghu CkNo ratings yet

- Bonded Labour in IndiaDocument16 pagesBonded Labour in IndiaRaghu CkNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Electoral System in IndiaDocument13 pagesElectoral System in IndiaRaghu CkNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Income Tax Changes For FY 2017-18 (AY 2018-19)Document22 pagesIncome Tax Changes For FY 2017-18 (AY 2018-19)soumyaviyer@gmail.comNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- 07 Chapter 2Document21 pages07 Chapter 2Raghu CkNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Computerized Accounting SystemsDocument5 pagesComputerized Accounting SystemsRaghu Ck100% (1)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Benami Transactions Prohibition Amendment Act 2015Document33 pagesBenami Transactions Prohibition Amendment Act 2015Latest Laws TeamNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Sa 200 AuditingDocument32 pagesSa 200 AuditingRaghu CkNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Composition Scheme Short NotesDocument1 pageComposition Scheme Short NotesRaghu CkNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Composition Scheme Under GSTDocument8 pagesComposition Scheme Under GSTRaghu CkNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- SBI Computer QuizDocument2 pagesSBI Computer QuizRaghu CkNo ratings yet

- 1Document11 pages1thecoltNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Composition Levy Under GSTDocument65 pagesComposition Levy Under GSTRaghu CkNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Important Acts Related To BankingDocument1 pageImportant Acts Related To BankingRaghu CkNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- HTMLDocument8 pagesHTMLRaghu CkNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Business EthicsDocument9 pagesBusiness Ethicskartikeya1067% (3)

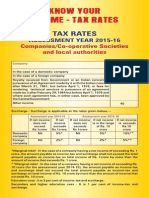

- Companies Tax RatesDocument2 pagesCompanies Tax RatesRaghu CkNo ratings yet

- Being As A Team Leader Why You Are Not Looking For Same Kind of Position Instead Why Are You Looking For Associate Level of JobDocument2 pagesBeing As A Team Leader Why You Are Not Looking For Same Kind of Position Instead Why Are You Looking For Associate Level of JobRaghu CkNo ratings yet

- Competency Mapping TelcoDocument64 pagesCompetency Mapping TelcoRaghu CkNo ratings yet

- Balance of PaymentDocument12 pagesBalance of PaymentAkhil James XaiozNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Competency Mapping TelcoDocument64 pagesCompetency Mapping TelcoRaghu CkNo ratings yet

- International Harmonization of Financial ReportingDocument8 pagesInternational Harmonization of Financial ReportingRaghu Ck100% (1)

- Basic Concept of AccountingDocument24 pagesBasic Concept of AccountingRaghu CkNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Value Added TaxDocument4 pagesValue Added TaxRaghu CkNo ratings yet

- Business EthicsDocument9 pagesBusiness Ethicskartikeya1067% (3)

- Corporate GovernanceDocument8 pagesCorporate GovernanceRaghu CkNo ratings yet

- Categories of E-CommerceDocument5 pagesCategories of E-CommerceRaghu CkNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- A Study On Training & DevelopmentDocument76 pagesA Study On Training & DevelopmentPradeepnspNo ratings yet

- Online Shopping ProjectDocument11 pagesOnline Shopping ProjectRaghu CkNo ratings yet

- Information Activity and RubricDocument2 pagesInformation Activity and RubricGlaiza FloresNo ratings yet

- Retirement WorksheetDocument55 pagesRetirement WorksheetRich AbuNo ratings yet

- Pfif PDFDocument1 pagePfif PDFcrystal01heartNo ratings yet

- MACROECONOMICS For PHD (Dynamic, International, Modern, Public Project)Document514 pagesMACROECONOMICS For PHD (Dynamic, International, Modern, Public Project)the.lord.of.twitter101No ratings yet

- Offtake Agreement For Maize: WHEREAS The Seller Has Offered To Supply The Buyer and The Buyer Has Agreed To PurchaseDocument3 pagesOfftake Agreement For Maize: WHEREAS The Seller Has Offered To Supply The Buyer and The Buyer Has Agreed To PurchaseChiccoe Joseph100% (1)

- Decision Trees Background NoteDocument14 pagesDecision Trees Background NoteibrahimNo ratings yet

- 1 InvoiceDocument1 page1 InvoiceMohit GargNo ratings yet

- TR 39 PDFDocument31 pagesTR 39 PDFSaifullah SherajiNo ratings yet

- London School of Commerce Colombo Campus Sri Lanka: MODULE ASSIGNMENT: Marketing ManagementDocument12 pagesLondon School of Commerce Colombo Campus Sri Lanka: MODULE ASSIGNMENT: Marketing ManagementRomali KeerthisingheNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- UPS Marketing PlanDocument8 pagesUPS Marketing PlanmaverickgmatNo ratings yet

- CHAPTER - 01 Agri. Business ManagementDocument187 pagesCHAPTER - 01 Agri. Business Management10rohi10No ratings yet

- Code of Business Ethics and ConductDocument7 pagesCode of Business Ethics and ConductShane NaidooNo ratings yet

- pp2 FinalDocument118 pagespp2 FinalRohan ToraneNo ratings yet

- Sukhvindersingh (13 0)Document4 pagesSukhvindersingh (13 0)Shadab KhanNo ratings yet

- Lecture 31 - 32 - 33 - 34 - Oligopoly MarketDocument8 pagesLecture 31 - 32 - 33 - 34 - Oligopoly MarketGaurav AgrawalNo ratings yet

- K. Marx, F. Engels - The Communist Manifesto PDFDocument77 pagesK. Marx, F. Engels - The Communist Manifesto PDFraghav vaid0% (1)

- SEBI Order On Jet-EtihadDocument17 pagesSEBI Order On Jet-EtihadBar & BenchNo ratings yet

- Form PDF 927448140281220Document7 pagesForm PDF 927448140281220Arvind KumarNo ratings yet

- Chipotle 2013 Organizational AnalysisDocument7 pagesChipotle 2013 Organizational Analysistarawneh92No ratings yet

- Gisella Cindy 115180047 JADocument32 pagesGisella Cindy 115180047 JAYuyun AnitaNo ratings yet

- Case Study 3 - Heldon Tool Manufacturing CaseDocument3 pagesCase Study 3 - Heldon Tool Manufacturing CasethetinkerxNo ratings yet

- Supply Chain DefinitionsDocument59 pagesSupply Chain DefinitionskathumanNo ratings yet

- BUSI1633 L5 - Value ChainDocument23 pagesBUSI1633 L5 - Value ChainBùi Thu Hươngg100% (1)

- Means of Avoiding or Minimizing The Burdens of TaxationDocument6 pagesMeans of Avoiding or Minimizing The Burdens of TaxationRoschelle MiguelNo ratings yet

- Characteristics of State Monopoly Capitalism in The USSRDocument4 pagesCharacteristics of State Monopoly Capitalism in The USSRΠορφυρογήςNo ratings yet

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- SUMP Brochure FinalDocument12 pagesSUMP Brochure FinalindraandikapNo ratings yet

- Role of Financial Markets and InstitutionsDocument8 pagesRole of Financial Markets and InstitutionsTabish HyderNo ratings yet

- Taxation LawDocument7 pagesTaxation LawJoliza CalingacionNo ratings yet

- Research Proposal of Role of Cooperatives On Women EmpowermentDocument9 pagesResearch Proposal of Role of Cooperatives On Women EmpowermentSagar SunuwarNo ratings yet

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo ratings yet