You might also like

- Presented by - Kshitiz Deepanshi Bhanu Pratap Singh Manali Aditya AnjulDocument13 pagesPresented by - Kshitiz Deepanshi Bhanu Pratap Singh Manali Aditya AnjulBhanu NirwanNo ratings yet

- ExcelDocument1 pageExcelJosh KempNo ratings yet

- Rs. RS.: Compass Company Balance Sheet, March 31Document2 pagesRs. RS.: Compass Company Balance Sheet, March 31aditi4garg-10% (1)

- Term V: Private Equity and Venture CapitalDocument3 pagesTerm V: Private Equity and Venture CapitalJitesh ThakurNo ratings yet

- Biyani's Think Tank: Concept Based NotesDocument49 pagesBiyani's Think Tank: Concept Based NotesGuruKPO71% (7)

- CH 09Document52 pagesCH 09Cyrus Zack100% (6)

- Oceanview Marine Company Audit Programs 30-3, 30-4, 30-5Document3 pagesOceanview Marine Company Audit Programs 30-3, 30-4, 30-5rebecca0% (2)

- Financial Management (MBOF 912 D) 1Document5 pagesFinancial Management (MBOF 912 D) 1Siva KumarNo ratings yet

- Question Sheet: (Net Profit Before Depreciation and After Tax)Document11 pagesQuestion Sheet: (Net Profit Before Depreciation and After Tax)Vinay SemwalNo ratings yet

- Financial ManagementDocument16 pagesFinancial ManagementManish FloraNo ratings yet

- LLM (G&S) 2020 - 38Document46 pagesLLM (G&S) 2020 - 38Shuvro AhsanNo ratings yet

- Research On Nesquik For Pakistani MarketDocument58 pagesResearch On Nesquik For Pakistani MarketUmair_ghNo ratings yet

- Leading-Change SU08Document8 pagesLeading-Change SU08harshnvicky123No ratings yet

- A Study of Mergers and Acquisitions in India and Their Impact On The Operating Performance and Shareholder WealthDocument41 pagesA Study of Mergers and Acquisitions in India and Their Impact On The Operating Performance and Shareholder WealthJarina JohnsonNo ratings yet

- IMT CastrolDocument6 pagesIMT CastrolRahul PandeyNo ratings yet

- Case StudyDocument3 pagesCase Studyjohnleh1733% (3)

- Director's Personal Liability - Hindrance To Business Decision?Document3 pagesDirector's Personal Liability - Hindrance To Business Decision?ADITYA BANERJEENo ratings yet

- 4p Analysis of Chota CokeDocument7 pages4p Analysis of Chota CokerosbindanielNo ratings yet

- Money and Capital Markets - OverviewDocument16 pagesMoney and Capital Markets - OverviewSarthak GuptaNo ratings yet

- 1Document8 pages1Snehak KadamNo ratings yet

- Group 13 AirtelDocument53 pagesGroup 13 AirtelShilpa Ravindran100% (1)

- Tata Sons Vs Cyrus MistryDocument12 pagesTata Sons Vs Cyrus MistryRahul Dinesh Kekane100% (1)

- Imt 69Document4 pagesImt 69arun1974No ratings yet

- Case Study CompilationDocument12 pagesCase Study CompilationanggaNo ratings yet

- Corporate Accounting - IiDocument26 pagesCorporate Accounting - Iishankar1287No ratings yet

- Swap RatioDocument11 pagesSwap RatioVaibhav Singla100% (1)

- IPL - A Group 9 - FinalDocument8 pagesIPL - A Group 9 - Finalvibhor1990No ratings yet

- Itc LimitedDocument21 pagesItc LimitedAnuradha Tomar67% (3)

- Bond With Pidilite: by Team The Right WritersDocument3 pagesBond With Pidilite: by Team The Right WritersPrabuNo ratings yet

- A Report On: Analysis of Financial Statements OF Tata Consultancy Services & Maruti SuzukiDocument38 pagesA Report On: Analysis of Financial Statements OF Tata Consultancy Services & Maruti SuzukiSaurabhNo ratings yet

- Business Law: Institute of Management TechnologyDocument5 pagesBusiness Law: Institute of Management Technologyarun1974No ratings yet

- Harsh PDFDocument10 pagesHarsh PDFsanketmehtaNo ratings yet

- Problem 1 (Wholly Owned Subsidiary) :: Holding Companies: Problems and SolutionsDocument9 pagesProblem 1 (Wholly Owned Subsidiary) :: Holding Companies: Problems and SolutionsRafidul IslamNo ratings yet

- Final Project Tata MotorsDocument72 pagesFinal Project Tata MotorsAshfaque AlamNo ratings yet

- Financial Modeling of Automobile Industry (Maruti Suzuki)Document26 pagesFinancial Modeling of Automobile Industry (Maruti Suzuki)Harshit PoddarNo ratings yet

- Cost Sheet For The Month of January: TotalDocument9 pagesCost Sheet For The Month of January: TotalgauravpalgarimapalNo ratings yet

- Blended Training Program - Batch Commenced On: Assignment - Day 3Document4 pagesBlended Training Program - Batch Commenced On: Assignment - Day 3Shubham BhawsarNo ratings yet

- IFA & EFA and Other Matrices of Strategic Management Applied On Suzuki MehranDocument16 pagesIFA & EFA and Other Matrices of Strategic Management Applied On Suzuki MehranAzaan AbubakerNo ratings yet

- Sahrudaya HealthcareDocument6 pagesSahrudaya HealthcareAakash Singh BJ22162No ratings yet

- Marketing Research On Positioning of Hero Honda Bikes in India - Updated - 2011Document54 pagesMarketing Research On Positioning of Hero Honda Bikes in India - Updated - 2011Piyush SoniNo ratings yet

- Mid Term Test: MM 5007: Financial ManagementDocument6 pagesMid Term Test: MM 5007: Financial ManagementFriendly AlfriusNo ratings yet

- IMT-01 Dec 09Document2 pagesIMT-01 Dec 09Fin CorpNo ratings yet

- Group Activity Submission: Ocean ModelDocument3 pagesGroup Activity Submission: Ocean ModelManish Pauli100% (1)

- Case StudyDocument2 pagesCase Studyyared haftuNo ratings yet

- Diversification of Horlicks BrandDocument12 pagesDiversification of Horlicks Branddeepak_hariNo ratings yet

- Group 6 - Transforming Luxury Distribution in AsiaDocument5 pagesGroup 6 - Transforming Luxury Distribution in AsiaAnsh LakhmaniNo ratings yet

- Case Study CavinkareDocument3 pagesCase Study CavinkareKshitiz112No ratings yet

- Business Law AssignmentDocument4 pagesBusiness Law AssignmentMOHIT SINGHNo ratings yet

- Applications and Solutions of Linear Programming Session 1Document19 pagesApplications and Solutions of Linear Programming Session 1Simran KaurNo ratings yet

- SENSEX Normal Sampling EstimationDocument2 pagesSENSEX Normal Sampling EstimationAbhishek BansalNo ratings yet

- Imt 24Document3 pagesImt 24subhadipsen52100% (1)

- Kingfisher Vs Fosters With Porters Five ForcesDocument32 pagesKingfisher Vs Fosters With Porters Five Forcesvenkataswamynath channa100% (5)

- Imt 15Document5 pagesImt 15pratiksha1091No ratings yet

- Corporate Governance' Vis-À-Vis Oppression and Mismanagement': A Case Study of Mr. Ratan Tata and Mr. Cyrus Mistry DisputeDocument11 pagesCorporate Governance' Vis-À-Vis Oppression and Mismanagement': A Case Study of Mr. Ratan Tata and Mr. Cyrus Mistry DisputeRamya SelvanNo ratings yet

- PGP MAJVCG 2019-20 S3 Unrelated Diversification PDFDocument22 pagesPGP MAJVCG 2019-20 S3 Unrelated Diversification PDFBschool caseNo ratings yet

- ExercisesDocument3 pagesExercisesrhumblineNo ratings yet

- Gamification in Consumer Research A Clear and Concise ReferenceFrom EverandGamification in Consumer Research A Clear and Concise ReferenceNo ratings yet

- Finance Question Papers Pune UniversityDocument12 pagesFinance Question Papers Pune UniversityJincy GeevargheseNo ratings yet

- Ii Semester Endterm Examination March 2016Document2 pagesIi Semester Endterm Examination March 2016Nithyananda PatelNo ratings yet

- Management Control SystemDocument11 pagesManagement Control SystemomkarsawantNo ratings yet

- 01 LeveragesDocument11 pages01 LeveragesZerefNo ratings yet

- UntitledDocument1 pageUntitledSaraswathy ArunachalamNo ratings yet

- Applied ElectronicsDocument37 pagesApplied ElectronicsGuruKPO100% (2)

- Abstract AlgebraDocument111 pagesAbstract AlgebraGuruKPO100% (5)

- Production and Material ManagementDocument50 pagesProduction and Material ManagementGuruKPONo ratings yet

- Advertising and Sales PromotionDocument75 pagesAdvertising and Sales PromotionGuruKPO100% (3)

- Think Tank - Advertising & Sales PromotionDocument75 pagesThink Tank - Advertising & Sales PromotionGuruKPO67% (3)

- OptimizationDocument96 pagesOptimizationGuruKPO67% (3)

- Applied ElectronicsDocument40 pagesApplied ElectronicsGuruKPO75% (4)

- Algorithms and Application ProgrammingDocument114 pagesAlgorithms and Application ProgrammingGuruKPONo ratings yet

- Data Communication & NetworkingDocument138 pagesData Communication & NetworkingGuruKPO80% (5)

- Biyani Group of Colleges, Jaipur Merit List of Kalpana Chawala Essay Competition - 2014Document1 pageBiyani Group of Colleges, Jaipur Merit List of Kalpana Chawala Essay Competition - 2014GuruKPONo ratings yet

- Algorithms and Application ProgrammingDocument114 pagesAlgorithms and Application ProgrammingGuruKPONo ratings yet

- Computer Graphics & Image ProcessingDocument117 pagesComputer Graphics & Image ProcessingGuruKPONo ratings yet

- Phychology & Sociology Jan 2013Document1 pagePhychology & Sociology Jan 2013GuruKPONo ratings yet

- Biological Science Paper I July 2013Document1 pageBiological Science Paper I July 2013GuruKPONo ratings yet

- Phychology & Sociology Jan 2013Document1 pagePhychology & Sociology Jan 2013GuruKPONo ratings yet

- Fundamental of Nursing Nov 2013Document1 pageFundamental of Nursing Nov 2013GuruKPONo ratings yet

- Community Health Nursing Jan 2013Document1 pageCommunity Health Nursing Jan 2013GuruKPONo ratings yet

- Business LawDocument112 pagesBusiness LawDewanFoysalHaqueNo ratings yet

- Paediatric Nursing Sep 2013 PDFDocument1 pagePaediatric Nursing Sep 2013 PDFGuruKPONo ratings yet

- Community Health Nursing I Nov 2013Document1 pageCommunity Health Nursing I Nov 2013GuruKPONo ratings yet

- Biological Science Paper 1 Nov 2013Document1 pageBiological Science Paper 1 Nov 2013GuruKPONo ratings yet

- Community Health Nursing I July 2013Document1 pageCommunity Health Nursing I July 2013GuruKPONo ratings yet

- Biological Science Paper 1 Jan 2013Document1 pageBiological Science Paper 1 Jan 2013GuruKPONo ratings yet

- Service MarketingDocument60 pagesService MarketingGuruKPONo ratings yet

- Software Project ManagementDocument41 pagesSoftware Project ManagementGuruKPO100% (1)

- Banking Services OperationsDocument134 pagesBanking Services OperationsGuruKPONo ratings yet

- Business Ethics and EthosDocument36 pagesBusiness Ethics and EthosGuruKPO100% (3)

- BA II English (Paper II)Document45 pagesBA II English (Paper II)GuruKPONo ratings yet

- Product and Brand ManagementDocument129 pagesProduct and Brand ManagementGuruKPONo ratings yet

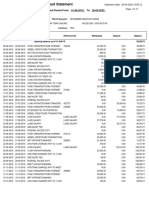

- Walter Mart Financial StatementDocument55 pagesWalter Mart Financial StatementRIANNE MARIE REYNANTE RAMOSNo ratings yet

- Tugas Akl Kelompok 2 - Chapter 17Document27 pagesTugas Akl Kelompok 2 - Chapter 17Viky Munyati100% (1)

- Curiculum Vitae Summary of ResumeDocument7 pagesCuriculum Vitae Summary of Resumehannah devinaNo ratings yet

- Corporate GovernanceDocument21 pagesCorporate GovernancePV JulianNo ratings yet

- Organisation and Function of Securities MarketsDocument19 pagesOrganisation and Function of Securities MarketsSyed Arham MurtazaNo ratings yet

- IAS7Document16 pagesIAS7Fitri Putri AndiniNo ratings yet

- IA 1 Valix 2020 Ver. Problem 27-3 - Problem 27-4Document4 pagesIA 1 Valix 2020 Ver. Problem 27-3 - Problem 27-4Ariean Joy Dequiña100% (1)

- A Primer On Reading Annual ReportsDocument229 pagesA Primer On Reading Annual ReportsTomas AriasNo ratings yet

- Par CorDocument15 pagesPar CorKim Nayve57% (7)

- Income Taxation SchemesDocument7 pagesIncome Taxation SchemesLeonard CañamoNo ratings yet

- Sbi Magnum Midcap Fund Factsheet (January-2021-34-1) PDFDocument1 pageSbi Magnum Midcap Fund Factsheet (January-2021-34-1) PDFavinash sengarNo ratings yet

- MashoodnasirDocument17 pagesMashoodnasirmashood nasirNo ratings yet

- Exercises I - Journalizing and PostingDocument7 pagesExercises I - Journalizing and PostingJowjie TV50% (2)

- BDI Org Chart For Oct 2019 WebDocument5 pagesBDI Org Chart For Oct 2019 WebbowiejkNo ratings yet

- Preface To Philippine Financial Reporting StandardsDocument5 pagesPreface To Philippine Financial Reporting StandardsSheila Mae AmbrocioNo ratings yet

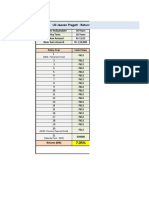

- LIC Jeevan Pragati - Returns Calculation - Example: (2010: Policy Start Year)Document2 pagesLIC Jeevan Pragati - Returns Calculation - Example: (2010: Policy Start Year)Ravi bNo ratings yet

- Financial Management, Scope, Objectives and Types of FinancesDocument13 pagesFinancial Management, Scope, Objectives and Types of Financesvenkataswamynath channa69% (13)

- Moot Problem-18 PDFDocument3 pagesMoot Problem-18 PDFbhupendra barhat100% (2)

- On October 1 2018 Jay Crowley Established Affordable Realty WhichDocument1 pageOn October 1 2018 Jay Crowley Established Affordable Realty WhichAmit Pandey0% (1)

- Sample ESOP ReportDocument18 pagesSample ESOP Reportsathish_bilagiNo ratings yet

- Mms Candy Traders 18 (Pty) LTD Abdul Aziz Arcade 6 85 Bertha Mkhize ST Durban 4001Document3 pagesMms Candy Traders 18 (Pty) LTD Abdul Aziz Arcade 6 85 Bertha Mkhize ST Durban 4001Bilal SameNo ratings yet

- 4-Financial Requirements and Sources For ACTG6144Document6 pages4-Financial Requirements and Sources For ACTG6144RylleMatthanCorderoNo ratings yet

- 12linsteel Book of Account DecemberDocument54 pages12linsteel Book of Account DecemberCarlos_CriticaNo ratings yet

- BFM - Mod - DDocument67 pagesBFM - Mod - DAbhishek KumarNo ratings yet

- Accounting 2&3 PretestDocument11 pagesAccounting 2&3 Pretestelumba michaelNo ratings yet

- Prolexus 2011Document82 pagesProlexus 2011Shakirah MazlanNo ratings yet

- CFAS Long QuizDocument4 pagesCFAS Long QuizKatrina PaquizNo ratings yet

- Definition of 'Amortizing Swap'Document4 pagesDefinition of 'Amortizing Swap'DishaNo ratings yet