You might also like

- Factors Determining The Working CapitalDocument4 pagesFactors Determining The Working CapitalSanctaTiffanyNo ratings yet

- Feasibility StudyDocument17 pagesFeasibility Studyjameson0% (1)

- LEGASPI - Porter's AnalysisDocument1 pageLEGASPI - Porter's AnalysisErika Mae LegaspiNo ratings yet

- Discounted Payback PeriodDocument10 pagesDiscounted Payback Periodbasanth babuNo ratings yet

- Ch02 Suppl Case XeroxDocument2 pagesCh02 Suppl Case XeroxPamela50% (2)

- CHAPTER 5.overview of Risk and ReturnDocument61 pagesCHAPTER 5.overview of Risk and ReturnDimple EstacioNo ratings yet

- Marr Calculation and ExamplesDocument4 pagesMarr Calculation and ExamplesAi manNo ratings yet

- Chap 8 Bond Valuation and RiskDocument37 pagesChap 8 Bond Valuation and RiskYasin ArAthNo ratings yet

- CH 12Document31 pagesCH 12Mochammad RidwanNo ratings yet

- Waiting Lines and Queuing Theory ModelsDocument65 pagesWaiting Lines and Queuing Theory ModelsMuhammad Shazwan NazrinNo ratings yet

- Chapter 07S SlidesDocument25 pagesChapter 07S SlidesSayadi AdiihNo ratings yet

- Module 4 - LINDO Optimization Tool KitDocument5 pagesModule 4 - LINDO Optimization Tool KitDiana Bunagan100% (1)

- IrrDocument11 pagesIrrnitishNo ratings yet

- Fnce 220: Business Finance: Lecture 6: Capital Investment DecisionsDocument39 pagesFnce 220: Business Finance: Lecture 6: Capital Investment DecisionsVincent KamemiaNo ratings yet

- What Is A Trade BarrierDocument6 pagesWhat Is A Trade BarrierShah AzeemNo ratings yet

- Specific Factors and Income DistributionDocument41 pagesSpecific Factors and Income DistributionAa LimNo ratings yet

- Inflation AccountingDocument13 pagesInflation AccountingtrinabhagatNo ratings yet

- Chapter 6Document13 pagesChapter 6Mariell Joy Cariño-Tan100% (1)

- Techniques Data CollectionDocument19 pagesTechniques Data CollectionMuhammad Akram KhanNo ratings yet

- Lecture Note On Project AppraisalDocument36 pagesLecture Note On Project Appraisalmatiwos samuel100% (3)

- 2.6 Activity Based Costing Abc Activity Based Management AbcDocument22 pages2.6 Activity Based Costing Abc Activity Based Management AbcだみNo ratings yet

- Chapter 4 - Limitations of FunctionalDocument1 pageChapter 4 - Limitations of FunctionalHafizah MardiahNo ratings yet

- Capital Budgeting: Dr. Sadhna BagchiDocument28 pagesCapital Budgeting: Dr. Sadhna Bagchiarcha agrawalNo ratings yet

- Chapter 4-Depreciation and Tax IncomeDocument39 pagesChapter 4-Depreciation and Tax IncomeSaeed KhawamNo ratings yet

- Internal Rate of ReturnDocument5 pagesInternal Rate of ReturnCalvince OumaNo ratings yet

- Management of Transaction ExposureDocument10 pagesManagement of Transaction ExposuredediismeNo ratings yet

- Net Present ValueDocument8 pagesNet Present ValueDagnachew Amare DagnachewNo ratings yet

- Calculate Compound InterestDocument5 pagesCalculate Compound InterestKyler GreenwayNo ratings yet

- Capital Investment and Appraisal MethodsDocument34 pagesCapital Investment and Appraisal MethodsAnesu ChimhowaNo ratings yet

- A. What Percentage of Parts Will Not Meet The Weight Specs?Document10 pagesA. What Percentage of Parts Will Not Meet The Weight Specs?Allen KateNo ratings yet

- Chap 7 Constraint ManagementDocument28 pagesChap 7 Constraint ManagementDasa SrmNo ratings yet

- Ilovepdf MergedDocument100 pagesIlovepdf MergedVinny AujlaNo ratings yet

- Chapter 5 Capacity PlanningDocument78 pagesChapter 5 Capacity PlanningAnthony Royupa100% (1)

- ProformaDocument4 pagesProformadevanmadeNo ratings yet

- Building and Sustaining Total Quality OrganizationsDocument17 pagesBuilding and Sustaining Total Quality OrganizationsDr Rushen SinghNo ratings yet

- Budgeting The ProjectDocument68 pagesBudgeting The ProjectnazirulNo ratings yet

- Xerox - The Bench Marking StoryDocument36 pagesXerox - The Bench Marking StoryAman Singh100% (3)

- Chapter 3 Linear ProgrammingDocument35 pagesChapter 3 Linear ProgrammingSaad ShaikhNo ratings yet

- Module 1. Hygens - PRELIM EXAM BUNAGANDocument8 pagesModule 1. Hygens - PRELIM EXAM BUNAGANDiana BunaganNo ratings yet

- Cost of Capital NotesDocument34 pagesCost of Capital Notesyahspal singhNo ratings yet

- Assignment #1 The International Financial EnvironmentDocument5 pagesAssignment #1 The International Financial EnvironmentjosephblinkNo ratings yet

- Operations Management: Processes and Supply Chains Chapter DigestDocument44 pagesOperations Management: Processes and Supply Chains Chapter DigestJohn Paul PrestonNo ratings yet

- Factors Affecting Cost of CapitalDocument40 pagesFactors Affecting Cost of CapitalKartik AroraNo ratings yet

- Economic Order Quantity ModelsDocument7 pagesEconomic Order Quantity ModelsP Singh KarkiNo ratings yet

- Testbank For Business FinanceDocument49 pagesTestbank For Business FinanceSpencer1234556789No ratings yet

- Pivot Table / Data Pilot Exercise: ExpedDocument2 pagesPivot Table / Data Pilot Exercise: Expedsensei43No ratings yet

- Exam Pointers For ReviewDocument2 pagesExam Pointers For ReviewJelly BerryNo ratings yet

- Capital Budgeting Decisions: Solutions To QuestionsDocument65 pagesCapital Budgeting Decisions: Solutions To QuestionsblahdeblehNo ratings yet

- Capital Budgeting Techniques PDFDocument57 pagesCapital Budgeting Techniques PDFMecheal ThomasNo ratings yet

- Difference Between Short Run and Long RunDocument6 pagesDifference Between Short Run and Long RunMuhammad RiazNo ratings yet

- Entry Strategies in Global BusinessDocument10 pagesEntry Strategies in Global BusinessLacie Hohenheim (Doraemon)100% (1)

- The U.S Postal Service Case Study Q1Document2 pagesThe U.S Postal Service Case Study Q1NagarajanRK100% (1)

- Location StrategyDocument15 pagesLocation Strategyhesham hassanNo ratings yet

- Telecommunications and NetworksDocument38 pagesTelecommunications and NetworksFika FebrikaNo ratings yet

- Activity Percentage of Time: Unloading 40% Counting 25 Inspecting 35Document9 pagesActivity Percentage of Time: Unloading 40% Counting 25 Inspecting 35Alia ShabbirNo ratings yet

- Net Present Value MethodDocument3 pagesNet Present Value MethodTawanda KurasaNo ratings yet

- Cost and Management - Sample QuestionDocument5 pagesCost and Management - Sample Questionfreddy kwakwalaNo ratings yet

- Net Present Value Method Net Present Value Method (Also Known As Discounted Cash Flow Method) Is A PopularDocument15 pagesNet Present Value Method Net Present Value Method (Also Known As Discounted Cash Flow Method) Is A PopularImranNo ratings yet

- Net Present ValueDocument5 pagesNet Present ValueIsrar KhanNo ratings yet

- Capital Budgeting DecisionsDocument120 pagesCapital Budgeting Decisionsgizex2013No ratings yet

- Biotin SupplymentsDocument2 pagesBiotin SupplymentsAkash RsNo ratings yet

- Journal of ExtrusionDocument8 pagesJournal of ExtrusionAkash RsNo ratings yet

- Recent Developments in Synthetic Marble Processing: Payel Bera, Neha Guptha, K. Priya Dasan and R. NatarajanDocument12 pagesRecent Developments in Synthetic Marble Processing: Payel Bera, Neha Guptha, K. Priya Dasan and R. NatarajanAkash RsNo ratings yet

- Behavior Based Safety: Gary Peacock Safety Consultant Ohio BWCDocument103 pagesBehavior Based Safety: Gary Peacock Safety Consultant Ohio BWCAkash Rs100% (1)

- Hazards Analysis & Risks Assessment: by Sebastien A. Daleyden Vincent M. GoussenDocument26 pagesHazards Analysis & Risks Assessment: by Sebastien A. Daleyden Vincent M. GoussenAkash RsNo ratings yet

- Recyclability and Reutilization of Carbon Fiber Fabric/epoxy CompositesDocument15 pagesRecyclability and Reutilization of Carbon Fiber Fabric/epoxy CompositesAkash RsNo ratings yet

- Marketing Management: Biyani's Think TankDocument41 pagesMarketing Management: Biyani's Think TankAkash RsNo ratings yet

- Ko Spider SilkDocument7 pagesKo Spider SilkAkash RsNo ratings yet

- Lab Manual: Rajalakshmi Engineering CollegeDocument1 pageLab Manual: Rajalakshmi Engineering CollegeAkash RsNo ratings yet

- Materials For Entertainment EngineeringDocument51 pagesMaterials For Entertainment EngineeringAkash RsNo ratings yet

- Silica Gel InfoDocument24 pagesSilica Gel InfoAkash RsNo ratings yet

- Certified Quality Engineer: Quality Excellence To Enhance Your Career and Boost Your Organization's Bottom LineDocument12 pagesCertified Quality Engineer: Quality Excellence To Enhance Your Career and Boost Your Organization's Bottom LineAkash Rs0% (1)

- FANUC Start UpDocument50 pagesFANUC Start UpAkash RsNo ratings yet

- Work-Breakdown Structure: A Simple and Powerful Tool For Project ManagementDocument57 pagesWork-Breakdown Structure: A Simple and Powerful Tool For Project ManagementAkash RsNo ratings yet

- Procurement and Vendor Management: Ordering Supplies and EquipmentDocument3 pagesProcurement and Vendor Management: Ordering Supplies and EquipmentAkash RsNo ratings yet

- Information ManagementDocument10 pagesInformation ManagementAkash RsNo ratings yet

- Budgetory ControlDocument36 pagesBudgetory ControlAkash RsNo ratings yet

- What Are Definition of Islamic Capital Market (ICM)Document45 pagesWhat Are Definition of Islamic Capital Market (ICM)Zizie2014No ratings yet

- Exercises For Corporate FinanceDocument13 pagesExercises For Corporate FinanceVioh NguyenNo ratings yet

- Audit Observation TemplateDocument10 pagesAudit Observation TemplateJoseph SalidoNo ratings yet

- Sample Memorandum of AgreementDocument3 pagesSample Memorandum of AgreementDivina Gammoot100% (1)

- Economics - Updated - Notes - by - Afreen MamDocument89 pagesEconomics - Updated - Notes - by - Afreen MamKajal RanaNo ratings yet

- Corporate Finance Institute: Financial Modeling & Valuation Analyst (FMVA) Program OverviewDocument39 pagesCorporate Finance Institute: Financial Modeling & Valuation Analyst (FMVA) Program OverviewVictor CharlesNo ratings yet

- Economy Shipping Co Case SolutionDocument7 pagesEconomy Shipping Co Case SolutionPaco Colín100% (2)

- Trading Account (Factorey) : Trading and Profit & Loss A/c With Different Groups & LedgerDocument2 pagesTrading Account (Factorey) : Trading and Profit & Loss A/c With Different Groups & Ledgersameer maddubaigariNo ratings yet

- Auditing Problems by Adrianne Paul I. Fajatin, CPA: Problem 1Document16 pagesAuditing Problems by Adrianne Paul I. Fajatin, CPA: Problem 1Moira C. Vilog100% (1)

- Forex Combo System.Document10 pagesForex Combo System.flathonNo ratings yet

- Standard, The Conceptual Framework Overrides That StandardDocument6 pagesStandard, The Conceptual Framework Overrides That StandardwivadaNo ratings yet

- Suryadev 75 InsuranceDocument15 pagesSuryadev 75 InsuranceKaran ChaudharyNo ratings yet

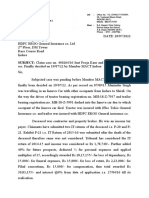

- SUBJECT: Claim Case No. 400264/16 SMT Pooja Kaur and Ors. Vs Ashok andDocument4 pagesSUBJECT: Claim Case No. 400264/16 SMT Pooja Kaur and Ors. Vs Ashok andkunal jainNo ratings yet

- Chapter - 1Document69 pagesChapter - 1111induNo ratings yet

- Hoisington Investment Management - Quarterly Review and Outlook, Second Quarter 2014Document10 pagesHoisington Investment Management - Quarterly Review and Outlook, Second Quarter 2014richardck61No ratings yet

- Unit V Responsibility Accounting: Prepared by Dr. Arvind Rayalwar Assistant Professor Department of Commerce, SSM BeedDocument13 pagesUnit V Responsibility Accounting: Prepared by Dr. Arvind Rayalwar Assistant Professor Department of Commerce, SSM BeedArvind RayalwarNo ratings yet

- Appendix 1.1 (Cir1124 - 2021)Document2 pagesAppendix 1.1 (Cir1124 - 2021)Vemula PraveenNo ratings yet

- Mountain State With NotesDocument12 pagesMountain State With NotesKeenan SafadiNo ratings yet

- FM Course Outline & Materials-Thappar UnivDocument74 pagesFM Course Outline & Materials-Thappar Univharsimranjitsidhu661No ratings yet

- AEC - 12 - Q1 - 0401 - SS2 Reinforcement - Investments, Interest Rate, and Rental Concerns of Filipino EntrepreneursDocument5 pagesAEC - 12 - Q1 - 0401 - SS2 Reinforcement - Investments, Interest Rate, and Rental Concerns of Filipino EntrepreneursVanessa Fampula FaigaoNo ratings yet

- Working Capital ManagementDocument38 pagesWorking Capital ManagementABHIJEIT BHOSALENo ratings yet

- Analisis Studi Kelayakan Bisnis Pada Kelompok UsahDocument11 pagesAnalisis Studi Kelayakan Bisnis Pada Kelompok UsahPermana Bagas SatriaNo ratings yet

- Transaction StatementDocument2 pagesTransaction StatementSatya GopalNo ratings yet

- AccountStatement 3286686240 Aug04 185310 PDFDocument2 pagesAccountStatement 3286686240 Aug04 185310 PDFDarren Joseph VivekNo ratings yet

- Chapter 23-Week 7Document7 pagesChapter 23-Week 7genessa_nelsonNo ratings yet

- ch12 PDFDocument4 pagesch12 PDFCarmela Isabelle DisilioNo ratings yet

- ExerciseDocument4 pagesExercisemuneeraaktharNo ratings yet

- Compare Housing Loan Rates in The PhilippinesDocument6 pagesCompare Housing Loan Rates in The PhilippinesAppraiser PhilippinesNo ratings yet

- Personal Account Opening Form: CommunicationdetailsDocument8 pagesPersonal Account Opening Form: CommunicationdetailsOvick AhmedNo ratings yet

- Unit Ii: Audit of IntangiblesDocument13 pagesUnit Ii: Audit of IntangiblesMarj ManlagnitNo ratings yet