You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Decision Support and Business Intelligence SystemsDocument57 pagesDecision Support and Business Intelligence SystemsAru BhartiNo ratings yet

- Management, Kathmandu Nepal, 27-30 April, pp.271-278Document9 pagesManagement, Kathmandu Nepal, 27-30 April, pp.271-278Aru BhartiNo ratings yet

- 6 Meera Arora 1730 Review Article VSRDIJBMR April 2013 PDFDocument8 pages6 Meera Arora 1730 Review Article VSRDIJBMR April 2013 PDFAru BhartiNo ratings yet

- Kingfisher AirlinesDocument8 pagesKingfisher AirlinesAru BhartiNo ratings yet

- Corporate Governance GuidelinesDocument8 pagesCorporate Governance GuidelinesAru BhartiNo ratings yet

- Income Saving and Investment Behaviour in India A Profile: VKRV (1980), Op - Cit., p.965Document44 pagesIncome Saving and Investment Behaviour in India A Profile: VKRV (1980), Op - Cit., p.965Radha Raman PandeyNo ratings yet

- Customer Relation Management in The Vodafone GroupDocument7 pagesCustomer Relation Management in The Vodafone GroupAru BhartiNo ratings yet

- CG HulDocument18 pagesCG HulAru BhartiNo ratings yet

- Data StreamDocument14 pagesData StreamAru BhartiNo ratings yet

- 01 2 RDocument48 pages01 2 RAru BhartiNo ratings yet

- English - Final Udaan Web Ad 31.01.2014Document9 pagesEnglish - Final Udaan Web Ad 31.01.2014Surya TejNo ratings yet

- Brand Equity: Capitalizing On Intellectual Capital: Ckohli@fullerton - EduDocument16 pagesBrand Equity: Capitalizing On Intellectual Capital: Ckohli@fullerton - EduManoj Kumar SinghNo ratings yet

- Uploaded FileDocument23 pagesUploaded FileVineet GargNo ratings yet

- Indian Banking IndustryDocument19 pagesIndian Banking IndustryCarlos BaileyNo ratings yet

- Sanjay KothariDocument25 pagesSanjay KothariKishore JamsutkarNo ratings yet

- Management of Non-Performing Assets in Indian Public Sector Banks With Special Santanu Das - Submission - 45Document25 pagesManagement of Non-Performing Assets in Indian Public Sector Banks With Special Santanu Das - Submission - 45jholerNo ratings yet

- A Comparative Study of Growth Analysis of Punjab National Bank of India and HDFC Bank LimitedDocument8 pagesA Comparative Study of Growth Analysis of Punjab National Bank of India and HDFC Bank LimitedInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- 7 Ijs May2012Document12 pages7 Ijs May2012Aru BhartiNo ratings yet

- Nguyen ThitdDocument51 pagesNguyen ThitdAru BhartiNo ratings yet

- 65 206 1 PBDocument9 pages65 206 1 PBPandit AnshumanNo ratings yet

- Group ISMDocument1 pageGroup ISMAru BhartiNo ratings yet

- Securitisation of Financial AssetsDocument16 pagesSecuritisation of Financial AssetsShivi JoshiNo ratings yet

- Capital MarketDocument31 pagesCapital MarketAru BhartiNo ratings yet

- Cross-Culture Communication and NegotiationDocument18 pagesCross-Culture Communication and NegotiationAru BhartiNo ratings yet

- Application of JIT in Toyota in IndiaDocument2 pagesApplication of JIT in Toyota in IndiaAru BhartiNo ratings yet

- Security Analysis - Investment ManagementDocument0 pagesSecurity Analysis - Investment ManagementAru BhartiNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- How To Organize A CooperativeDocument12 pagesHow To Organize A CooperativeKAKKAMPI100% (35)

- 8 - Capital Structure PT 1Document32 pages8 - Capital Structure PT 1Rohan SinghNo ratings yet

- Shoba LTD PDFDocument72 pagesShoba LTD PDFkasperNo ratings yet

- Question: Wembley Travel Agency Specializes in Ights Between Los AnDocument2 pagesQuestion: Wembley Travel Agency Specializes in Ights Between Los AnShweta RayNo ratings yet

- Assignment Classification Table: Topics Brief Exercises Exercises ProblemsDocument125 pagesAssignment Classification Table: Topics Brief Exercises Exercises ProblemsYang LeksNo ratings yet

- Solved Mocha Company Has Four Employees and Each Employee Earned 50 000Document1 pageSolved Mocha Company Has Four Employees and Each Employee Earned 50 000Anbu jaromiaNo ratings yet

- Return of IncomeDocument18 pagesReturn of IncomeTania SharmaNo ratings yet

- Life Insurance Corporation of India - Policyholder Information FormDocument1 pageLife Insurance Corporation of India - Policyholder Information FormSri RamNo ratings yet

- Trial Balance (PD JAYA MOTOR)Document1 pageTrial Balance (PD JAYA MOTOR)Arum AnnisaNo ratings yet

- TAXATION001Document31 pagesTAXATION001Boqorka AmericaNo ratings yet

- 3 Economic Questions by Economic SystemDocument10 pages3 Economic Questions by Economic SystemGeraldine WilsonNo ratings yet

- CBZ Dividend AnnouncementDocument1 pageCBZ Dividend AnnouncementBusiness Daily ZimbabweNo ratings yet

- Circular No 4 2023Document2 pagesCircular No 4 2023NESL WebsiteNo ratings yet

- Accounts - Track 1B2 - Class Notes NovDec 2022Document237 pagesAccounts - Track 1B2 - Class Notes NovDec 2022chandsultana45690No ratings yet

- Examining Business Potential and Growth in Textile and Apparel Industry: A Case Study in MalaysiaDocument20 pagesExamining Business Potential and Growth in Textile and Apparel Industry: A Case Study in MalaysiaAhmad Hirzi AzniNo ratings yet

- PROBLEM 1 and 2Document3 pagesPROBLEM 1 and 2Thea MisolaNo ratings yet

- 1st Year Answer Key Online Quiz 2021 1st WaveDocument9 pages1st Year Answer Key Online Quiz 2021 1st Wavegigi meiNo ratings yet

- PM - LearnsignalDocument70 pagesPM - LearnsignalEbtisam HanifNo ratings yet

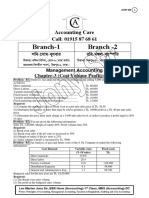

- CVP (4th) - SheetDocument11 pagesCVP (4th) - SheetMahabubur RahmanNo ratings yet

- Chapter 3: Working With Financial StatementsDocument10 pagesChapter 3: Working With Financial StatementsNafeun AlamNo ratings yet

- Chapter 2 - Taxes, Tax Laws, and Tax AdministrationDocument7 pagesChapter 2 - Taxes, Tax Laws, and Tax Administrationreymardico100% (2)

- Gross Profit Variation AnalysisDocument1 pageGross Profit Variation AnalysisJulie Ann Canlas100% (2)

- Istiqlal Ramadhan Rasyid - 11180820000040 - Latihan Soal AKM 1Ch.23Document4 pagesIstiqlal Ramadhan Rasyid - 11180820000040 - Latihan Soal AKM 1Ch.23Istiqlal RamadhanNo ratings yet

- ACCT1115 - Group Case Section A17 Part 2 Group 1Document7 pagesACCT1115 - Group Case Section A17 Part 2 Group 1Maria Jana Minela IlustreNo ratings yet

- Income Taxation - Final Taxes and CGTDocument3 pagesIncome Taxation - Final Taxes and CGTDrew BanlutaNo ratings yet

- 1 Points: Save and SubmitDocument34 pages1 Points: Save and SubmitnyxNo ratings yet

- Ar Cy 2015 PDFDocument258 pagesAr Cy 2015 PDFMudit KediaNo ratings yet

- Mas Chapter 6 PDFDocument33 pagesMas Chapter 6 PDFJohanna Vidad100% (1)

- CH 07Document19 pagesCH 07Ahmed Al EkamNo ratings yet

- Analysis of Financial Performance For AlphabetDocument6 pagesAnalysis of Financial Performance For AlphabetPham Ha AnNo ratings yet