Professional Documents

Culture Documents

Commercial Bank

Uploaded by

Anjali SharmaCopyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Commercial Bank

Uploaded by

Anjali SharmaCopyright:

Available Formats

TYBBI

Commercial Banking

EXECUTIVE SUMMARY Commercial banks occupy a dominant place in the money market. They, as a matter of fact, form the largest component in the banking structure of any country. They are the oldest, largest and fastest growing financial institutions in India. They are profit making institutions, dealing in money and credit. Commercial banks play a major role in the growth and development of the country due to the modern organi ation and functioning, huge funds and wide network all over the country. Thus, they are like a reservoir into which flow the savings, the idle surplus money of households and from which loans are given on interest to businessmen and others who need them for investment or productive uses. Commercial banks are very important source of institutional credit as they are the major depository of people!s savings. They are very important devices for providing short term credit to trade and commerce. Commercial Banks being repositories of deposits have played significant role in garnering savings of the people particularly after the nationali ation. Thus, they have made praiseworthy efforts in pooling the savings. Rationale of the study The "ationale of the study can be considered as follows#$ ability.

%hri Chinai College &

The study includes essential core topics. It aims at giving a thorough grounding on the subject. The study is comprehensive. It helps to improve the research and investigation

TYBBI

Commercial Banking

Hypothesis:

It enables to think logically and practically

The hypothesis being put forth for this study about Commercial banking is that awareness of Commercial banks is &''(, but there are still many people who do not know about the Commercial banks and the amenities provided by them. Commercial banks are coming up with new innovative ideas and schemes for increasing their customer base and fulfilling the needs of the general public. Research Methodolo y: The research methodology is data collection through#$ )"I*+"Y %,-"C.% %.C,/0+"Y %,-"C.% !ri"ary Sources: %urvey by distributing 1uestionnaire to the people taking sample si e of &'', Interviews conducted with bankers2 accumulating knowledge and help from friends, professors, etc. Secondary Sources: 3athering data through books, journals, maga ines, websites, newspapers, etc. E#pected Contri$ution .4pectations from the study are that it may contribute to the real scenario of commercial banking demand and accordingly the banks can go for new innovative schemes. It will also specify some recommendations and based

%hri Chinai College

TYBBI

Commercial Banking

on that banks can make suitable arrangements in a particular sector. It will also make people aware about Commercial banking.

%hri Chinai College

TYBBI

Commercial Banking

Introduction of $an%in : anking, in its crude form, is an age$old phenomenon. It was in e4istence even in ancient times, too. It is the business of providing financial services to consumers and businesses. They

are the single major source of institutional finance in the country. +ccording to %ection 7 8c9 of the Banking "egulation +ct, &:;: $ <Banking company means any company which transacts the business of banking in India=. %ection 7 8b9 of the act defines banking as accepting for the purpose of lending or investment of deposits of money fro the public repayable on demand or otherwise and withdrawable by che1ue, draft, order or otherwise. Banking services also serve two primary purposes. &irst, by supplying customers with the basic mediums$of$e4change 8cash, checking accounts, and credit cards9, banks play a key role in the way goods and services are purchased. >ithout these familiar methods of payment, goods could only be e4changed by barter 8trading one good for another9, which is e4tremely time$consuming and inefficient. Second, by accepting money deposits from savers and then lending the money to borrowers, banks encourage the flow of money to productive use and investments. This in turn allows the economy to grow. >ithout this flow, savings would sit idle in someone!s safe or pocket, money would not be available to borrow, people would not be able to purchase cars or houses, and businesses would not be able to build new factories the economy needs to produce more goods and

%hri Chinai College ;

TYBBI

Commercial Banking

grow. .nabling the flow of money from savers to investors is called financial intermediation, and thus, banking is e4tremely important to a free market economy. 'ri in and E(olution of Indian )an%in ,pinions differ as to the origin of the work ?Banking?. The word ?Bank? is said to be of 3ermanic origin, cognate with the @rench word ?Ban1ue? and the Italian word ?Banca?, both meaning ?bench?. It is surmised that the word would have drawn its meaning from the practice of the Aewish money$changers of Bombardy, a district in /orth Italy, who in the middle ages used to do their business sitting on a bench in the market place. +gain, the etymological origin of the word gains further relevance from the derivation of the word ?Bankrupt? from the @rench word ?Ban1ue route? and the Italian word ?Banca$rotta? meaning ?Broken bench? due probably to the then prevalent practice of breaking the bench of the money$ changer, when he failed. Banking is different from money$lending but two terms have in practice been taken to convey the same meaning. Banking has two important functions to perform, one of accepting deposits and other of lending monies andCor investment of funds. It follows from the above that the rates of interest allowed on deposits and charged on advances must be known and reasonable. The money$lender advances money out of his own private wealth hardly accepts deposits and usually charges high rates of interest. *ore often, the rates of interest relate to the needs of the borrower. *oney$ lending was practiced in all countries including India, much earlier than the recent type of Banking came on scene.

%hri Chinai College

TYBBI

Commercial Banking

Si nificance of )an%s

The importance of a bank to modern economy, so as to enable them to develop, can be stated as follows# 8i9 The banks collect the savings of those people who can save and allocate them to those who need it. These savings would have remained idle due to ignorance of the people and due to the fact that they were in scattered and oddly small 1uantities. But banks collect them and divide them in the portions as re1uired by the different investors. 8ii9 Banks preserve the financial resources of the country D it is e4pected that they allocate them appropriately in the suitable D desirable manner. 8iii9 They make available the means for sending funds from one place to another and do this in cheap, safe and convenient manner. 8iv9 Banks arrange for payments by che1ues, order or bearer, crossed and uncrossed, which is the easiest and most convenient. Besides they also care for making such payments as safe as possible. 8v9 Banks also help their customers, in the task of preserving their precious possessions intact and safe. To advance money, the basis of modern industry and economy and essential for financing the developmental process, is governed by banks. 8vii9 It makes the monetary system elastic. %uch elasticity is greatly desired in the present economy, where the phase of economy goes on changing and with such changes, demand for money is re1uired. It is 1uite proper and convenient for the government and ".B.I. to change its currency and credit policy fre1uently, This is done by "BI, by changing the supply of money with the changing needs of the public.

%hri Chinai College E

TYBBI

Commercial Banking

+lthough traditionally, the main business of banks is acceptance of deposits and lending, the banks have now spread their wings far and wide into many allied and even unrelated activities. Structure of )an%in Syste"

+t present, the organi ed banking system in India can be broadly divided into three categories# i9 ii9 iii9 The Central Bank of the country, the "eserve Bank of India The Commercial Banks The Cooperative Banks. The "BI is the ape4 monetary and banking authority in the country and has the responsibility to control the banking system in India. Co""ercial $an%s play a major role in the growth and development of the country. They mobili e savings and make them available to large and small industrial enterprise and traders for working capital re1uirements. +fter &:E:, commercial banks are broadly classified into nationali ed or public sector banks and private sector banks. The %BI and its associate banks along with another 5' banks are the public sector banks. The private sector banks include Indian scheduled banks which have not been nationali ed and branches of foreign banks operating in India. The "egional "ural Banks came into e4istence since the middle of &:F's with the specific objective of providing credit and deposits facilities to the small and marginal farmers, agricultural labourers and artisans and small entrepreneurs.

%hri Chinai College

TYBBI

Commercial Banking

)an%in in India

Banking in India act as a connected link between the borrowers and lenders of money. The banks main activity should be to do the business of banking

%hri Chinai College G

TYBBI

Commercial Banking

which should not be subsidiary to any other business. Thus, a bank should always add the word <Bank= to its name to enable people to know that it is a bank and is dealing in money.

(From small to large, commercial banking have got u covered, as In banking there is no such thing as one size fits all )

%hri Chinai College

TYBBI

Commercial Banking

I*TR'+UCTI'* T' C'MMERCIA, )A*-S: Commercial banks play a vital role in the economic development of a

nation. They are the most important source of institutional credit in the money market as they provide short term loans and advances to its customers. They perform a variety of functions and are the main source of credit which is the main input for trade and business activity. Credit created by commercial banks is a major component of money supply in a modern economy. *odern economies depend on the banking sector for production, e4change and distribution. + Commercial bank is a type of financial intermediary and a type of bank. Commercial bank has two possible "eanin s: a9 It is the term used for a normal bank to distinguish it from an investment bank. b9 Commercial banking can also refer to a bank or a division of a bank that mostly deals with deposits and loans from corporations or large businesses, as opposed to normal individual members of the public 8retail banking9. + commercial bank is a profit seeking organi ation dealing in the other people!s money, in the sense that it accepts deposits of money from the public to keep them in its custody for safety. %o also, it deals in credit, i.e., it creates credit by making advances out of the funds received as deposits to needy people. It charges higher rate of interests for the loans sanctioned and

%hri Chinai College

&'

TYBBI

Commercial Banking

offers lower rate of interest for the deposits. The difference between the two is the profit earned by the bank. Thus, a commercial bank functions as a mobiliser of saving in the economy. The most distinctive feature of a commercial bank is that it accepts deposits called demand deposits from the public which are che1uable, i.e., withdrawable by means of che1ue. +cceptance of che1uable deposits alone, however, does not give it a status of bank. Its another essential function is to make use of these deposits for lending to others. Commercial banks ordinarily are simple business or commercial concerns which provide various types of financial services to Hcustomers in return for payments in one form or another, such as interest, discounts, fees, commission, and so on. %o, we can say that their objective is to make profits. + commercial bank is therefore like a reservoir into which flow the savings, the idle surplus money of households and from which loans are given on interest to businessmen and others who need them for investment or productive uses. +efinition: .conomists have defined a Commercial Bank in various ways. $ +ccording to )rof. Crowther, <a banker is a dealer in debt, his own and other people!s.= $ +ccording to )rof. says, <Commercial Banks are institutions whose debts I usually referred to as bank deposits I are commonly accepted in final settlement of other people!s deposits.= Thus, all these definitions clearly indicate the essential function of a bank namely dealing in money and credit.

%hri Chinai College

&&

TYBBI

Commercial Banking

&U*CTI'*S '& C'MMERCIA, )A*-S Commercial banks perform many functions. They satisfy the financial

needs of the sectors such as agriculture, industry, trade, communication, so they play very significant role in a process of economic social needs. The functions performed by banks, since recently, are becoming customer$ centred and are widening their functions. 3enerally, the functions of commercial banks are divided into two categories# primary functions and the secondary functions. The following chart simplifies the functions of commercial banks. Commercial banks perform various primary functions, some of them are given below#

Commercial banks accept various types of deposits from public especially from its clients, including saving account deposits, recurring account deposits, and fi4ed deposits. These deposits are payable after a certain time period Commercial banks provide loans and advances of various forms, including an overdraft facility, cash credit, bill discounting, money at call etc. They also give demand and demand and term loans to all types of clients against proper security. Credit creation is most significant function of commercial banks. >hile sanctioning a loan to a customer, they do not provide cash to the borrower. Instead, they open a deposit account from which the borrower can withdraw. In other words, while sanctioning a loan, they

%hri Chinai College

&5

TYBBI

Commercial Banking

automatically create deposits, known as a credit creation from commercial banks. +long with primary functions, commercial banks perform several secondary functions, including many agency functions or general utility functions. The secondary functions of commercial banks can be divided into agency functions and utility functions. The agency functions are the following#

To collect and clear che1ue, dividends and interest warrant. To make payments of rent, insurance premium, etc. To deal in foreign e4change transactions. To purchase and sell securities. To act as trusty, attorney, correspondent and e4ecutor. To accept ta4 proceeds and ta4 returns. To provide safety locker facility to customers. To provide money transfer facility. To issue travellerHs che1ue. To act as referees. To accept various bills for payment# phone bills, gas bills, water bills, etc. To provide merchant banking facility. To provide various cards# credit cards, debit cards, smart cards, etc.

The utility functions are the following#

%hri Chinai College

&6

TYBBI

Commercial Banking

!ER&'RMA*CE '& C'MMERCIA, )A*-S I* THE !'ST .*ATI'*A,I/ATI'* !ERI'+ Achie(e"ents:

01

2a3 ,ead )an% Sche"e# +fter nationali ation, it was felt that banks should be allotted particular districts where they would take the lead in studying the need and scope for banking development. -nder the scheme, districts were allotted to the %tate Bank 3roup, &; nationalised banks and 6 private banks. .ach bank was assigned the status of Jlead bank! in a particular district. The lead bank had to study and understand the socio$economic condition of the district and undertake surveys for this purpose. Through the surveys the lead bank would collect useful information about the credit needs, development needs and pattern of production and nature of employment in the district. +fter such informations were gathered, the lead bank would then plan and implement development programmes in the area, with the help of other banks and financial institutions. This scheme was a uni1ue e4periment and it helped in branch e4pansion, deposit mobili ation and e4pansion of priority sector lending. 2$3 )ranch E#pansion: +fter nationali ation, there was massive e4pansion of bank branches, especially in the rural areas. The Bead Ban k scheme played played a major role in this. 0uring the first fifteen years after nationali ation, branches e4panded at about 5,;'' per year. Total number of bank branches has increased from G5E5 in &:E: to EF,5G6 in 5''F.

%hri Chinai College

&;

TYBBI

Commercial Banking

,ver G'( of bank offices are located in backward states and in semi$urban areas and rural areas. This, to some e4tent took care of regional imbalance in the spread of banking. 2c3 +eposit Mo$ili4ation: +s a result of e4pansion of banking facilities, there was a large increase in deposits. In &:E:, deposits amounted to &6( of the 30), by 5''; this ratio increased 67' times. The increase in rural deposits as production of total has been from 6( to &7(. Bank deposits now constitute about ;'( of financil assets held by households. 2d3 )an% ,endin : Traditionally, banks in India had concentrated in providing working capital to industry and trade. ,nly after nationali ation, loans are being given for agricultural operations. Bank credit stood at "s. 6, 6:: crore in &:E:. In the ne4t 6 decades, his increased by about 5'' times. In &:EG, large and medium industries accounted for about 5'' times. In &:EG, large and medium industries accounted for about E'( of aggregate bank credit. +griculture accounted for about 5(. This changed drastically after nationali ation and bank credit to priority sector, including agriculture was close to ;'( of total credit. 2e3 +irected Credit !ro ra""es: + major objective of bank

nationali ation was to make bank credit available the priority sector, comprising of agriculture, small scale industries, e4ports, transporters and small traders at concessional rates. This system of directed bank credit was e4pected to contribute to contribute to economic growth as well as social justice. %uccess was achieved in this direction after nationali ation.

%hri Chinai College

&7

TYBBI

Commercial Banking

51 2a3

Shortco"in s# Inade6uate )an%in facilities# 0espite achievements in branch

e4pansion, banking facilities continue to remain inade1uate to meet the needs of the large population. The national average population per bank branch is still very high at about &5'''. This ratio is higher than the national average in some states like Bihar, ,rissa, >est Bengal and *adhya )radesh. Banking facilities are still not e1uitably distributed among all states. 2$3 Inade6uate +eposit Mo$ili4ation: Banking habits of people in India

are still not very good. + large part of the population still prefer to carry out transactions in cash and are not covered by the banking system . Therefore, there is a large scope for further increasing deposits and bring in more money in the banking system. 2c3 Inade6uate lendin : .ven though there has been significant increase

in lending to priority sectors, it is still inade1uate in comparison to the needs of these sectors. Because of these small farmers and traders have to still depend on the unorgani ed sector for meeting their credit re1uirements. 2d3 Increased E#penditure: +fter nationali ation, there has been

significant increase in e4penditure on banking operations. This is due to aggressive and sometimes irrational branch e4pansion. There has been over$

%hri Chinai College

&E

TYBBI

Commercial Banking

staffing in nationali ed banks and some of their operations in rural areas are simply not economically feasible. 2e3 ,o7 ,e(el of Efficiency: )ublic sector banks have suffered from lack

of proper supervision and control. 0ue to high degree of political interference and lack of competition, these banks have become highly insufficient. There work culture was poor compared to private sector banks. Kowever, this scenario has now changed with these banks becoming more profit oriented and autonomous. Thus, nationali ation of Commercial banks was done with the objective of social and economic development. But this resulted in several problems and desortions in the banking system. Till &::'s public sector banks operated with low profitability and efficiency. In early &::'s, the government implemented the /arsimham Committee "ecommendations in order to bring about much needed reforms in the banking sector. %ince then, the sector has been performing with higher profitability and efficiency.

%hri Chinai College

&F

TYBBI

Commercial Banking

C'MMERCIA, )A*-S I* I*+IA

+s part of the financial services industry, insurance, commercial banking, and capital markets companies worldwide are attempting to compete better

%hri Chinai College &G

TYBBI

Commercial Banking

by improving core operations and differentiating the customer e4perience. Kowever, this is not easily achieved because of the volume of business challenges financial services companies deal with today.

%hri Chinai College

&:

TYBBI

Commercial Banking

Ser(ices typically offered $y Co""ercial )an%s +lthough the basic type of services offered by a commercial bank depends upon the type of bank and the country, services provided usually include#

$

Taking deposits from their customers and issuing current 8-L9 or checking 8-%9 accounts and savings accounts to individuals and businesses.

$ $

.4tending loans to individuals and businesses2 Cashing che1ues @acilitating money transactions such as wire transfers and cashierHs checks Issuing credit cards, +T* cards, and debit cards %toring valuables, particularly in a safe deposit bo4 Cashing and distributing bank rolls )ension D retirement planning.

$ $ $

$ Consumer D commercial financial advisory services

$

@inancial transactions can be performed through many different channels# $ + branch, banking centre or financial centre is a retail location where a bank or financial institution offers a wide array of face to face service to its customers. $ +T* is a computerised telecommunications device that provides a financial institutionHs customers a method of financial transactions in a public space without the need for a human clerk or bank teller. $ *ail is part of the postal system which itself is a system wherein written documents typically enclosed in envelopes, and also small

%hri Chinai College

5'

TYBBI

Commercial Banking

packages containing other matter, are delivered to destinations around the world. $ Telephone banking is a service provided by a financial institution which allows its customers to perform transactions over the telephone. $ ,nline banking is a term used for performing transactions, payments etc. over the Internet through a bank, credit union or building societyHs secure website.

+E)IT CAR+

CRE+IT CAR+

MAI,

ATM

'*,I*E )A*-I*8

TE,E!H'*E )A*-I*8

%hri Chinai College

5&

TYBBI

Commercial Banking

E&&ECT '& C'MMERCIA, )A*-I*8 '* )USI*ESS A*+ I*+USTRY I* I*+IA9

T

&. 5.

he term Commercial Bank is not meant only for Business and industry. Commercial bank is meant primarily for personal banking and secondarily for commercial developments. The banks

looking mainly deposits from public and lending small and short term loans to public and short businessmen. Banking sector is called the </erve centres of the nationHs economy= and <Backbones of modern Industries and Commerce=. + minor change in the basis points by the nationHs central bank can make a huge impact on the nationHs production and inflation.

Commercial banks facilitate the growth of the business. Be it rural small scale 8Cottage industries9 or Mery large scale investments. The deposits from public is mobilised to fund the commercial activities. These activities in turn generate income which is added to the gross domestic product of the nation. Thus, banks are the most crucial sector that helps a nation grow economically.

%hri Chinai College

55

TYBBI

Commercial Banking

CHA,,E*8ES )E&'RE I*+IA* C'MMERCIA, )A*-S

*ajor challenges which Indian commercial banks are facing today and which are likely to be more poignant in the ensuing years in view of the irreversible process of the reforms and resultant verisimilitude of more players entering the banking sector are discussed below. !ro$le" of pressure on profita$ility: The greatest challenge which )%Bs are facing in recent years arises out of pressure on their profitability. >ith continuous e4pansion in number of branches and manpower, thrust on social and rural banking, directed sector lending, maintenance of higher reserve ratios, waiver of loans under +"0"$type concessions, repayment defaults by large industrial corporate and other borrowers etc. had their telling impact on the profitability of the banks. @urther with the introduction of prudential norms, to be effective from *arch &::6 a majority of the commercial banks balance sheets had shown huge losses. In order to improve financial health of these banks the 3overnment provided a dose of hybrid capital and in return these banks were made to sign a memorandum of understanding with "BI. +ccordingly, the focus of operation of banks shifted from deposit mobili ation to services marketing. @urther, accent of banks operation shifted to non$fund based business with an eye on capital ade1uacy achievement and other ancillary business which may cross subsidi e the cost of certain unremunerative services, the banks have to offer.

%hri Chinai College 56

TYBBI

Commercial Banking

!ro$le" of lo7 producti(ity: +nother furious challenge which indian commercial banks are

confronting is low productivity. The low productivity has been due to huge surplus manpower, absence of good work culture, andbabsence of employees commitment to the organi ation. . The management have continued to prefer not to see the problem in its proper perspective due to the fear of strong unions. They have camouflaged the issue by diverting their attention to such apparent face saving devices like redeployment, repositioning , retraining, etc.. There are various ways of minimi ing the si e of the staff, such as voluntary retirement scheme or golden shakehand. The problem before the management at present is how to cut si e of the staff and improve productivity of the bank. !ro$le" of *on.!erfor"in Assets2*!A3: + serious threat to the survival and success of Indian banking system is uncomfortably high level of non$performing assets. In its "eport on trend and )rogress of banking In India, &::F$:G, the "BI reported that gross /)+s as percentage of advances of )%Bs was &E percent as on *arch 6&, 5''' with a colossal amount of about "s. 75,''' crore being locked up. This might have recently recorded further increase due to default in repayment by the industrial units affected by the two$year old recession. This is much higher than the international level of below 7(. %piraling non$ performing assets are hurting bank!s profitability and even the basic inability of the banking system by way of both non$recognition of interest income and loan loss provisioning.

%hri Chinai College

5;

TYBBI

Commercial Banking

!ro$le" fro" custo"ers: In view of unleashing of competitive forces and fast changing

life styles and values of customers who are now better informed and more sophisticated and discerning and who have a wide choice to choose from various banking and non$banking intermediaries have become more demanding and their e4pectations in terms of products, delivery and price are increasing, the )%Bs lacking in customers! orientation are finding it difficult to even retain their highly valued customers what to talk of attracting the new clients particularly when the foreign banks are also the new breed of private sector banks have embarked upon aggressive marketing programme aiming at niche markets. The telebanking, anywhere banking, virtual or internet banking, +T*, credit cards and newly introduced interest rate swap, forward rate agreements, etc. are some of the products innovated by the new players. +lthough the )%Bs are trying to computeri e their operations, the pace of progress in this direction has been decidedly slow. The rather tardy progress in the area has been due to the initial reservation of the staff unions against computeri ation for the lurking fear of employment cut, as also the e4istence of huge number of branches in the rural areas, where suitable logistics are not available. *arket share of )%Bs both in deposits and lending has declined. This has already become a serious cause of concern for )%Bs regulating strategic efforts for thwarting the challenges from the new players. Co"petition fro" *e7 )an%s: The commercial banks in India which enjoyed monopoly position until recently are facing perilous challenges particularly on 1uality, cost and fle4ibility fronts from the newly emerging players who by dint of their

%hri Chinai College 57

TYBBI

Commercial Banking

invigorating ambience and work culture supported by pragmatic leadership committed, courteous, affable and trained staff and modern ultra gadgets are offering e4cellent customers services and making inroads in the business centres. The new banks have set the tone and to e4tent also the standard for technological improvements and product innovations which the vastly dominating )%Bs will have to bring about in their own operations if they have to maintain their present position of dominance. @or instance, Bank of )unjab has opened a new savings bank product$swagat with a minimum balance re1uirement . K0@C has launched 1 new retail account$@reedom$for customers who would be using the non$branch infrastructure of the bank like +T*, phone banking and internet banking . The ICICI Bank has product offerings tailor$made to specific categories of customers, such as students, traders, /"Is as well as the salary customers.It is going to offer a special scheme for senior citi ens. By resorting to latest methods in human resources management as well as information technology, the new entrants in the field have suddenly sensitised even the ordinary user of the banking services in India to the type and 1uality of services he can e4pect from his bank. The market has become highly competitive and largely customers centric. This calls for an ability to reach the client at his door step and meet his re1uirements of products and services in a customi ed manner. The race for customers could at times lead to adverse selections. This situation demands aggression laced with caution, in turn, calls for highly efficient management by the banks of both liabilities and assets.

%hri Chinai College

5E

TYBBI

Commercial Banking

These banks have to work in a market which will not know any geographical barriers and therefore will have to develop abilities of product innovation and delivery comparable to the best in the world. Co"petition fro" lo$al "a:ors 3lobalisation and integration of Indian financial market with world and the conse1uent entry of foreign players in domestic market has infused, in its wake, brutal competitive pressure on the Indian commercial banks. @oreign players endowed with robust capital ade1uacy, high 1uality assets, world$wide connectivity, benefits of economies of scale and stupendous risk management skills are posing serious threats to the e4isting business of the Indian banks. In order to compete successfully with the new entrants, Indian banks need to possess matching financial muscle, as fair competition is possible only along the e1uals. +verage si e of an Indian bank is niggardly low in comparison to a foreign bank. The 1uestion before the major Indian Commercial Banks, therefore, is how to ac1uire competitive si e. !ro$le" of Mana in +uality of '7nership # *anaging duality of ownershipis a peculiar problem which the )%Bs have to encounter because of participation of the private shareholders in their capital. + public sector bank to survive and grow successfully is e4pected to operate according to the e4pectations if one of its principal shareholders. In the changed scenario, there would be two major groups of shareholders, vi ., the government of India and "BI on the one hand and the private shareholder , on the other . %ince the e4pectations of these two categories of owners are not necessarily identical, the bankers will have to manage conflicting interests.

%hri Chinai College

5F

TYBBI

Commercial Banking

)ASIC !R'),EM '& A C'MMERCIA, )A*The basic problem facing a bank manager is to have a satisfactory trade off between li1uidity and profitability $ the two principal but conflicting goals of a bank. + bank deals in the money of the people. The success of the business of a bank depends partly on the efficiency with which it can provide services to its creditors 8depositories9, but mainly on the confidence it inspires among the depositors. It has been able to attract the deposits of the people not only by promising some returns on their money but also by committing itself to repayment on demand. This is why the public accepts bank deposits as being <as good as cash.= The banker must, therefore, ensure an ade1uate amount of li1uidity in his assets so that he may be able to meet any claims upon it in cash on demand. The perfectly li1uid asset is cash itself because it can fully satisfy the depositors! claims. The more cash a banker holds, the more obviously he can, without difficulty of any kind, offer cash in e4change for deposits. @urther, the banker with an ade1uate amount of cash in hand can meet the credit needs of the community and can make speculative gains. Kowever, cash is a sterile asset which earns no income at all. + banker cannot afford to ignore income because the ultimate object of a bank is to make earnings on its business which are sufficient to compensate it for the cost which it incurs on raising funds, besides paying the wages of the staff and meeting other e4penses. If a banker holds a large portion of his funds in ready cash without earning any income on it, his business will result in losses, and sound the death$knell of the bank after some time. Ke must therefore, employ the bulk of the bank!s resources in giving loans and advances, and in investing them in high$

%hri Chinai College

5G

TYBBI

Commercial Banking

yielding securities. %uch investments are, however, subject to credit risk I the risk arising from default in repayment money lent out and the money rate risk I the risk arising out of fluctuations in the market rate of interest. The banker will not be able to satisfy the cash re1uirements of the depositors on demand with the funds deployed in the other investments. ,nce the depositor!s che1ues are not honored, the bank will lose the confidence of the public, which will result in a mass run on the bank!s counters and jeopardi e the li1uidity position of the bank. -ltimately, the very survival of the bank is endangered. Bi1uidity and profitability are, therefore, inimical to each other. Cash has perfect li1uidity but lacks yield. +t the other ends are some loans and investments which yield a high rate of interest, but are hardly li1uid at all. The conflict between li1uidity and income is not as sharp as it appears. In order to ensure long$run earnings, the commercial bank must retain public confidence in order to continue to survive and provide for the li1uidity needs of the bank. The art of commercial banking lies in the resolution of the conflicts between li1uidity and profitability. <It is an art because science ha not furnished inviolable rules2 banks must be managed with discrimination and good judgement. "ules and scientific procedures for doing the whole job cannot be framed.=& + number of approaches, ways and means of resolving the conflicts have been developed from time$to$time. These approaches subse1uently came to be known as theories of li1uidity management.

%hri Chinai College

5:

TYBBI

Commercial Banking

)A*- +E!'SITS A*+ THEIR STRUCTURE:

Commercial banks being repositories of deposits have played significant role in garnering savings of the people particularly after their nationali ation, as is evidenced from Table below. It may e noted from the Table that bank deposits boomed by over "s. F,G;,''' crores between &:;F and 5'''6. There was acceleration in deposit mobili ation after nationali ation of banks. This was because of tremendous branch e4pansion, growth in interest rates and introduction of innovative deposit schemes. +s a result, per capita deposits to national income rose significantly from &7.7( as on Aune &:E: to over ;&( as at the end of Auly 5'''. +mount of bank deposits soared to "s. :, :&,6&G crore as on *ay ;, 5''& with per capital deposits of the order of "s. :,:''. +eposits of Co""ercial )an%s durin 0;<=. 5>>=

Year

As on +ece"$er

A"ount in crore of Rs

0?>@> <?CC0 0D?5DD ;5?5AA 5?>>?DC; D?>A?D;C C?=;?@;< =?C0?C=@ =?@D?0CD ;?;0?A0@

!er capita +eposits 2Rs13

A5 << 0?0;@ 5?AC@ D?<>5 =?0D= =?C0= =?@D0 ;?;>> ;?;>>

+eposits as or of *ational Inco"e

*A 0D1D 551@ <01D <510 <01> <51C <51< <01> *A

0;<= Bune 0;C; Bune 0;=C Bune 0;@C March 0;;0 March 0;;= +ec1 5>>> Sept1 5>>A Buly? 5>>D May? 5>>=

ASSET.,IA)I,ITY MA*A8EME*T 2A,M3

%hri Chinai College

6'

TYBBI

Commercial Banking

In the recent past, banks in India have started using the +sset$Biability *anagement 8+B*9 as the techni1ue or strategy for financial management. +B* aims at planning, directing, and regulating the levels, changes, mi4es of assets and liabilities of banks in the short$run, usually three to twelve months, with a view to enable them to achieve their long$term objectives. The net interest margin and its variability are the focus of its attention so as to ma4imise "eturn ,n .1uity 8",.9, and to minimise fluctuations in ",.. It also links capital, non$interest income and e4penses, and strategic choices regarding products, markets, and bank structure. +B* involves giving balanced emphasis necessary in a competitive environment characterised by deregulatiom. and greater viability 8volatility9 of interest rates, variable rates pricing, and the use of interest rates derivatives. +B* is an integrated strategic managerial approach of managing a total Balance %heet dynamics having regard to the si e and 1uality in such a way that the net earnings from interest are ma4imi ed. This is done by matching of liabilities and assets in terms of maturity, cost and yield rates. The focus of +B* is not to build up deposits and loansCassets in isolation, but on net interest income and recogni ing interest rates and li1uidity risks. Thus, +B* is essentially a guide for survival of a bank in deregulated environment. 0iagramatic presentation of +B* is brought out in the following chart#

Asset.,ia$ility Mana e"ent Structure

%hri Chinai College 6&

TYBBI

Commercial Banking

Asset-Liability Management

8eneral Asset? ,ia$ility E Capital Mana e"ent

Specific

,ia$ility Mana e"ent &inancial

Asset Mana e"ent

)alance Sheet Mana e"ent

Inco"e E E#penditure Mana e"ent

. '$:ecti(es of A,M )rimary objective of +B* approach is to manage market risk in such away as to minimi e the impact of net interest income fluctuations in the short run and protect the net economic value of the bank in the long run. )recisely speaking, +B* has the following objectives# &. To control the volatility of net interest income and net economic value of a bank.

%hri Chinai College

65

TYBBI

Commercial Banking

5. 6. ;.

To control volatility in all target accounts . To control li1uidity risk, and To ensure an acceptable Balance profitability and growth rate.

$ A,M And Co""ercial )an%s: &9 "eformed process in India has emerged mew players, new instrument and new products at competitive rates has increased banks risks. 59 This new development forced the Commercial banks to take a re$look on +B* to remain competitive D withstand the risk. 69 "BI also advised Commercial Banks to tighten their +sset$Biability management and to furnish data in a format outlined by it. In the recent past, banks in India have started using the +sset$Biability *anagement 8+B*9 as the techni1ue or strategy for financial management. +B* aims at planning, directing, and regulating the levels, changes, mi4es of assets and liabilities of banks in the short$run, usually three to twelve months, with a view to enable them to achieve their long$term objectives. The net interest margin and its variability are the focus of its attention so as to ma4imise "eturn ,n .1uity 8",.9, and to minimise fluctuations in ",.. It also links capital, non$interest income and e4penses, and strategic choices regarding products, markets, and bank structure. +B* involves giving balanced emphasis necessary in a competitive environment characterised by deregulatiom. and greater viability 8volatility9 of interest rates, variable rates pricing, and the use of interest rates derivatives.

)A*-S )A,A*CESHEET E !'RT&',I' MA*A8EME*T

%hri Chinai College

66

TYBBI

Commercial Banking

Conventionally, banks publish balance sheets in their annual reports. The balance sheets contains particulars of a Bank!s current assets and current liabilities. +ssets items refer to all credit items in indicating the wealth and claims possessed by the bank. Biability items refer to all debit items indicating the obligations of the bank. Thus, the balance sheet indicates the manner in which the bank has raised funds and invested them in various types of assets. It is the means by which the banks financial position I its solvency and li1uidity I is judged. There is, of course the e1uity of assets and liabilities in the balance sheet of a bank, as in the case of any other balance sheet. In a balance sheet, it is customary to state the liabilities on the left and assets on the right. The liabilities of the banks are the items which are to be paid by it either to its shareholders or depositors. The assets of the banks are those items fro which it hopes to get an income. Thus, the assets include all the amounts owed by others to the bank. + much simplified format of a bank!s balance sheet may be illustrated as follows#

%hri Chinai College

6;

TYBBI

Commercial Banking

The &or"at of )alance Sheet of A )an% ,ia$ilities Assets

01 Share capital 51 Reser(e &unds A1 +eposits: a3 Ti"e deposits $3 +e"and deposits c3 Sa(in s deposits <1 )orro7in s D1 'ther ite"s 01 Cash in hand FF 7ith central $an% FF 7ith other $an%s 51 Money at call and short notice1 A1 )ills discounted? includin treasury $ills1 <1 In(est"ents D1Ad(ances C1'ther Ite"s

. '$:ecti(es of portfolio "ana e"ent# + commercial bank has to manage its assets and liabilities with three considerations in mind namely, li1uidity, profitability and solvency. Bi1uidity means the capacity of the bank to give cash on demand in e4change for deposits. But since a bank is a commercial concern, it aims at profitability. )rofits come from the income accruing from the assets the bank holds. The banker must arrange hiss assets in such a way that he makes more income. Kence, in ac1uiring assets, the banker will be influenced by the consideration of profit. + bank ac1uires assets mainly out of the deposits of the public. )ublic confidence in the bank, however, depends on the belief that the bank will always be able to e4change deposits for cash. + bank, therefore, must keep a sufficient amount of cash balance to meet the actual demand, while for meeting the potential demand, it has to keep its assets sufficiently li1uid. Cash has perfect li1uidity, but yields no returns at all, while other income$yielding assets such as loans are profitable but have no

%hri Chinai College

67

TYBBI

Commercial Banking

li1uidity. Bi1uidity and profitability are, therefore, conflicting consideration for the bankers. +nother consideration of the bank is its solvency and security. This refers to the li1uidity and shiftability of assets. Bi1uidity is the capacity to produce cash on demand. %hiftability means that type of assets ac1uired by a bank be easily shiftable to other banks or to the central bank. Therefore a banker will prefer securities which can be 1uickly disposed of and which are easily shiftable without any loss to the bank or to those which are highly risky but more profitable. But a bank is li1uid only to the e4tent that it can turn its assets into cash to meet the demands of depositors and other creditors. Thus, the two motives of a banks li1uidity and profitability are contradictory, but have to be reconciled. + good banker is one who follows a wise investment policy and distributes the assets in such a way both the re1uirements of li1uidity and profitability are satisfied. The assets should bring in ma4imum profit and should provide ma4imum security to the depositors. The secret of success of a bank lies in striking a sound balance between li1uidity and profitability. In reading a balance sheet of a bank, we have to e4amine the liabilities and assets portfolios which reveals how best the two objectives of li1uidity and profitability have been reconciled by the banker.

%hri Chinai College

6E

TYBBI

Commercial Banking

,ia$ilities !ortfolio

The liabilities portfolio of a bank is comparatively simple. It shows how the bank raises funds. .very commercial bank usually gets its funds in three ways# by share capital, reserve fund and deposits from the general public. @or instance, liabilities may be incurred by accepting or endorsing bills of e4change on behalf of customers. o Assets !ortfolio

The assets portfolio of the bank is both comple4 and interesting. It represents more faithfully the varied nature and ramification of the banks functions and investment policies. In fact the asset side of the balance sheet indicates the manner in which the funds entrusted to the bank are deployed. -sually, every banker seems to arrange its assets in an ascending order of profitability and descending order of li1uidity. Thus, the structure of a balance sheet indicates assets appearing in the descending order or li1uidity.

%hri Chinai College

6F

TYBBI

Commercial Banking

CURRE*T SCE*ARI' '& C'MMERCIA, )A*-I*8: Currently 85>>=9, overall, banking in India is considered as fairly mature in terms of supply, product range and reach$even though reach in rural India still remains a challenge for the private sector and foreign banks. .ven in terms of 1uality of assets and capital ade1uacy, Indian banks are considered to have clean, strong and transparent balance sheets$as compared to other banks in comparable economies in its region. The "eserve Bank of India is an autonomous body, with minimal pressure from the government. The stated policy of the Bank on the Indian "upee is to manage volatility$ without any stated e4change rate$and this has mostly been true. >ith the growth in the Indian economy e4pected to be strong for 1uite some time$ especially in its services sector, the demand for banking services$especially retail banking, mortgages and investment services are e4pected to be strong. *D+s, takeovers, asset sales and much more action 8as it is unravelling in China9 will happen on this front in India. In *arch 5''E, the "eserve Bank of India allowed >arburg )incus to increase its stake in Lotak *ahindra Bank 8a private sector bank9 to &'(. This is the first time an investor has been allowed to hold more than 7( in a private sector bank since the "BI announced norms in 5''7 that any stake e4ceeding 7( in the private sector banks would need to be vetted by them. Currently, India has GG scheduled commercial banks 8%CBs9 $ 5G public sector banks 8that is with the 3overnment of India holding a stake9, 5: private banks 8these do not have government stake2 they may be publicly listed and traded on stock e4changes9 and 6& foreign banks. They have a combined network of over 76,''' branches and &F,''' +T*s. +ccording to a report by IC"+ Bimited, a rating agency, the public sector banks hold over F7 percent of total assets of the banking industry, with the private and foreign banks holding &G.5( and E.7( respectively.

%hri Chinai College 6G

TYBBI

Commercial Banking

>e know that, in banking, there is no such thing as ?one si e fits all.? But todayHs commercial banks are more diverse than ever. YouHll find a tremendous range of opportunities in Commercial banking, starting at the branch level because Commercial bankers, now are highly e4perienced in working with businesses to develop the right financial package to meet your uni1ue business needs. Thus, Commercial lending today is a very intense activity, with banks carefully analysing the financial condition of their business clients to determine the level of risk in each loan transaction

%hri Chinai College

6:

TYBBI

Commercial Banking

%hri Chinai College

;'

TYBBI

Commercial Banking

'VERVIEG '& ICICI )A*- E S)I )A*-

ICICI )an% is IndiaHs second$largest bank with total assets of "s. 6,;;E.7G billion 8-%N F: billion9 at *arch 6&, 5''F and profit after ta4 of "s. 6&.&' billion for fiscal 5''F. ICICI Bank is the most valuable bank in India in terms of market capitali ation and is ranked third amongst all the companies listed on the Indian stock e4changes in terms of free float market capitali ation. The Bank has a network of about :7' branches and 6,6'' +T*s in India and presence in &F countries. ICICI Bank offers a wide range of banking products and financial services.

HYPERLINK imgurl=http:// "http://images.google.co.in/imgres? .apitco.or

.apitco.org/images/s!i"logo.#pg$imgre%url=http://

g/our"promoters.html$h=&'($ =&'($s)='$hl=en$start=(*$t!ni+=,-P.o/guL 01g#1:$t!nh=2/$t!n =2/$pre,=/images3'453'6logo3/7o%3/787I3/7 3/7!an93/:start3'6':3/:g!,3'6/3/:n+sp3'6&*3/:s,num 3'6&03/:hl3'6en3/:sa3'6N" "http://t!n0.google.com/images? 5=t!n:,-P.o/guL01g#1:http:// .apitco.org/images/s!i"logo.#pg" => IN;L-6EPI;<-RE

1ER?E4@R1A<INE<

%hri Chinai College

;&

TYBBI

Commercial Banking

The origin of the State )an% of India goes back to the first decade of the ninet eenth century with the establishment of the Bank of Calcutta in Calcutta on 5 Aune &G'E and three years later, it was re$designed as the Bank of Bengal 85 Aanuary &G':9. + uni1ue institution, it was the first joint$stock bank of British India sponsored by the 3overnment of Bengal. The Bank of Bombay 8&7 +pril &G;'9 and the Bank of *adras 8& Auly &G;69 followed the Bank of Bengal. These three banks remained at the ape4 of modern banking in India till their amalgamation as the Imperial Bank of India on 5F Aanuary &:5&.

%hri Chinai College

;5

TYBBI

Commercial Banking

ICICI Bank today

Large capital base Vast talent pool Low operating costs Technology focus Strong corporate relationships

Indias Indiaslargest largest private privatesector sector bank bankand andone one of thefinancial top financial stop solution solutions provider providerwith witha a diversified diversifiedand and de de-risked -risked business businessmodel model

!erfor"ance of ICICI )an%

ICICI Bank, IndiaHs largest bank in the private sector. It is IndiaHs second$ largest bank with total assets of "s. 6,;;E.7G billion at *arch 6&, 5''F. ICICI Bank is the most valuable bank in India in terms of market capitali ation.The Bank has a network of about :7' branches and 6,6'' +T*s in India and presence in &F countries. ICICI Bank offers a wide range of banking products and financial services to corporate and retail customers through a variety of delivery channels and through its specialised subsidiaries and affiliates in the areas of investment banking, life and non$ life insurance, venture capital and asset management. The Bank currently has subsidiaries in the -nited Lingdom, "ussia and Canada, branches in %ingapore, Bahrain, Kong Long, %ri Banka and 0ubai International @inance Centre and representative offices in the -nited %tates, -nited +rab .mirates,

%hri Chinai College

;6

TYBBI

Commercial Banking

China, %outh +frica, Bangladesh, Thailand, *alaysia and Indonesia. ,ur -L subsidiary has established a branch in Belgium. ICICI offers various products and services in India in areas of commercial banking, online stock trading, loans 8home, auto, personal etc9, insurance, foreign e4change trading and mutual funds. It also offers services to non$ resident Indians like money transfer, /". and /", savings accounts and certain investment options as well.

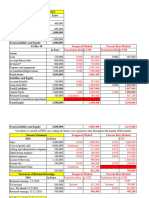

&or" HAF

B+B+/C. %K..T ,@ ICICI )A*B+B+/C. %K..T as on 6&st *arch# $ 5>>C.5>>= CA!ITA, E ,IA)I,ITIES Capital "eserves and %urplus 0eposits Borrowings ,ther liabilities D )rovisions Total Sch & 5 6 ; 7 5>>= &5,;:6,;6F 56;,&6:,5'F 5,6'7,&'&,GE6 7&5,7E',5E6 6G5,5GE,67E A?<<C?D@0?05C Rs1 in >>>Fs 5>>C &5,6:G,6;7 5&6,&E&,7F& &,E7',G6&,F&6 6G7,5&:,&6E 575,5FG,FFF 5?D0A?@@;?D<5

%hri Chinai College

;;

TYBBI

Commercial Banking

ASSETS Cash D balances with "BI Balance with banks D money at call D short notice Investments +dvances @i4ed +ssets ,ther assets Total Assets Contingent liabilities Bills for collection Co""on si4e State"ent of ICICI )an% &5 E F G : &' && &GF,'EG,F:; &G;,&;;,;75 :&5,7FG,;&G &,:7G,E77,::E 6:,56;,565 &E;,G::,56; A?<<C?D@0?05C 7,E5:,7::,'E' ;',;E7,E&' G:,6;6,F6F G&,'7G,7'G F&7,;F6,:;; &,;E&,E6&,'G: 6:,G'F,&&7 &5E,7F7,&;: 5?D0A?@@;?D<5 6,:7',66E,E77 ;6,6G;,E;G

CA!ITA, E ,IA)I,ITIES Capital "eserves and %urplus 0eposits Borrowings ,ther liabilities D )rovisions Total

Sch & 5 6 ; 7

5>>= &5,;:6,;6F 56;,&6:,5'F 5,6'7,&'&,GE6 7&5,7E',5E6 6G5,5GE,67E A?<<C?D@0?05C

I & F EF &7 &' 0>>

%hri Chinai College

;7

TYBBI

Commercial Banking

ASSETS Cash D balances with "BI E &GF,'EG,F:; &G;,&;;,;75 :&5,7FG,;&G &,:7G,E77,::E 6:,56;,565 &E;,G::,56; A?<<C?D@0?05C &5 7,E5:,7::,'E' ;',;E7,E&' 7 E 5E 7F & 7 0>> &E6 &

Balance with banks D money at call F D short notice Investments +dvances @i4ed +ssets ,ther assets Total Assets Contingent liabilities Bills for collection Co"parati(e Si4e State"ent of ICICI )an% CA!ITA, E ,IA)I,ITIES Capital "eserve and surplus 0eposit Borrowing ,ther liabilities Total ,ia$ilities Sch & & 5 6 ; 7 5>>= &5,;:6,;6F 56;,&6:,5'F G : &' &&

5>>C &5,6:G,6;7 5&6,&E&,7F&

8ro7th :7':5 5':FFE6E

I 2J3K2.3 & &' ;' 66 75 A=

5,6'7,&'&,GE6 &,E7',G6&,F&6 E7;5F'&7' 7&5,7E',5E6 6G5,5GE,67E 6G7,5&:,&6E 575,5FG,FFF &5F6;&&5F &6'''F7F:

A?<<C?D@0?05C 5?D0A?@@;?D<5 ;A5C;0D@<

%hri Chinai College

;E

TYBBI

Commercial Banking

ASSETS

Cash D balance with "BI Balance with banks D money at call D short notice Investments +dvances @i4ed +sset ,ther assets Total Assets Contingent liabilities Bills for collection

E F G : &' &&

&GF,'EG,F:; &G;,&;;,;75 :&5,7FG,;&G

G:,6;6,F6F G&,'7G,7'G F&7,;F6,:;;

:FF57'7F &'6'G7:;; &:F&';;F;

&': &5F 5G 6; 8&9 6' A= ;6 8F9

&,:7G,E77,::E &,;E&,E6&,'G: ;:F'5;:'F 6:,56;,565 &E;,G::,56; 6:,G'F,&&7 &5E,7F7,&;: 87F5GG69 6G65;'G7

A?<<C?D@0?05C 5?D0A?@@;?D<5 ;A5C;0D@< &5 7,E5:,7::,'E' 6,:7',66E,E77 &EF:5E5;'7 ;',;E7,E&' ;6,6G;,E;G 85:&:'6G9

Trend Analysis of ICICI )an%

CA!ITA, E ,IA)I,ITIES

Sch & 5 6 ; 7 5>>A :,E5E,E'' E6,5'E,76G ;G&,E:6,'E6 6;6,'5;,5'6 &F',7E:,57G I &'' &'' &'' &'' &'' 5>>< :,EE;,'&5 F6,:;&,7E& EG&,'G7,G;7 6'F,;'5,6:6 &G',&:;,:6' I &'' &&F &;& :' &'E 5>>D &',GEF,F7G &&G,&6&,:7; ::G,&GF,FF7 667,;;;,:E' 5&6,:E&,E'E I &&6 &GF 5>>C &&5,6:G,6;7 5&6,&E&,7F& I &&EG & 66F 6;6 &&5 &;G 5>>= &5,;:6,;6F 56;,&6:,5'F 5,6'7,&'&,GE6 7&5,7E',5E6 6G5,5GE,67E I &6' 6F' ;F: &;: 55;

Capital "eserve and surplus 0eposit Borrowing ,ther liabilities Total

5'F &,E7',G6&,F&6 :G &57 6G7,5&:,&6E 575,5FG,FFF

0?>C@?00;?CC5 0>> 0?5D5?5@@?=<0 00= 0?C=C?D;<?>DA 0D= 5?D0A?@@;?D<5

5AD

A?<<C?D@0?05C

A5A

ASSETS

%hri Chinai College

;F

TYBBI

Commercial Banking

Cash D balance with "BI

Balance with banks D money at call D short notice

;G,GE&,;;7

&''

7;,'F:,:EE

&&&

E6,;;:,'';

&6'

G:,6;6,F6F

&G6

&GF,'EG,F:;

6G6

&E,'5G,7G&

&''

6',E5E,6FG

&:&

E7,G7',F&:

;&&

G&,'7G,7'G

7'E

&G;,&;;,;75

&&;:

Investments

67;,E56,''5

&''

;6;,677,5&;

&55

7,';,GF6,757

&;5

F&7,;F6,:;;

5'5

:&5,7FG,;&G

57F

+dvances

765,F:;,&;;

&''

E5E,;FE,5GG

&&G

:&;,'7&,7&F

&F5 &,;E&,E6&,'G:

5F;

&,:7G,E77,::E

6EG

@i4ed +ssets

&'

;',E'F,5F;

&''

;',7E;,&;&

&''

;',6G',6E&

::

6:,G'F,&&7

:G

6:,56;,565

:F

,ther +ssets

&&

F7,5'7,5&E

&''

EE,&GE,F7;

GG

GF,:GG,:5F

&&F

&5E,7F7,&;:

&EG

&E;,G::,56;

5&:

Total Assets

0?>C@?00;?CC5 0>> 0?5D5?5@@?=<0 00= 0?C=C?D;<?>DA 0D= 5?D0A?@@;?D<5

5AD

A?<<C?D@0?05C

A5A

Contingent liabilities

&5

G:;,6G7,'F'

&'' 5,'5:,;&:,'5F 55F 5,EG&,76F,6G5 6'' 6,:7',66E,E77

;;5

7,E5:,7::,'E'

E5:

Bills for collection

&6,6EF,G;6

&''

&7,&':,675

&&6

56,:5',:55

&F:

;6,6G;,E;G

657

;',;E7,E&'

6'6

%hri Chinai College

;G

TYBBI

Commercial Banking

MAI* )RA*CH '& STATE )A*- '& I*+IA? !A*ABI

!erfor"ance of State )an% of India 2S)I3 %BI is the number one Bank in India and is regarded as IndiaHs largest commercial bank, listed in the @ortune 7'' among Banks world wide and is having more than :6'' branches world wide 8appro4imately &;( of all bank branches9 and commands one$fifth of deposits and loans of all scheduled commercial banks in India. The main Branch ,f %tate Bank ,f India is at )anaji, has the uni1ue privilege in 3oa to trace back its roots to two centuries of banking. +s there was no formal transition either in 3overnment or in banking from )ortuguese control, for a time the entire territory of 3oa was without any commercial banking facility.

%hri Chinai College

;:

TYBBI

Commercial Banking

In this backdrop, )anaji Branch then became first Branch of a Bank to start functioning in 3oa. The %tate Bank 3roup includes a network of eight banking subsidiaries and several non$banking subsidiaries offering merchant banking services, fund management, factoring services, primary dealership in government securities, credit cards and insurance. The ei ht $an%in su$sidiaries are: $ %tate Bank of Bikaner and Aaipur 8%BBA9 $ %tate Bank of Kyderabad 8%BK9 $ %tate Bank of India 8%BI9 $ %tate Bank of Indore 8%BI"9 $ %tate Bank of *ysore 8%B*9 $ %tate Bank of )atiala 8%B)9 $ %tate Bank of %aurashtra 8%B%9 $ %tate Bank of Travancore 8%BT9 The origins of %tate Bank of India date back to &G'E when the Bank of Calcutta 8later called the Bank of Bengal9 was established. In &:5&, the Bank of Bengal and two other )residency banks 8Bank of *adras and Bank of Bombay9 were amalgamated to form the Imperial Bank of India. In &:77, the controlling interest in the Imperial Bank of India was ac1uired by the "eserve Bank of India and the %tate Bank of India 8%BI9 came into e4istence by an act of )arliament as successor to the Imperial Bank of India.

Today, %tate Bank of India 8%BI9 has spread its arms around the world and has a network of branches spanning all time ones. %BIHs International Banking 3roup delivers the full range of cross$border finance solutions through its four wings $ the 0omestic division, the @oreign ,ffices division, the @oreign 0epartment and the International %ervices division.

%hri Chinai College

7'

TYBBI

Commercial Banking

&EATURES '& STATE )A*- '& I*+IA

$ .4tended Banking Kours $ "ound the Clock +T* and Telebanking $ +ttractive 0eposit %chemes $ The first Branch in operation in )ost Biberation 3oa $ >arm unmatched ambience that you will love $ @ully computeri ed Branch with latest Technological value added services. $ Branch with the largest number of Customers among all Banks $ The number one Bank in 3oa $ )art of a group with over a century of Banking traditi

&or" HAF B+B+/C. %K..T ,@ S)I )A*- ,T+ B+B+/C. %K..T as on 6&st *arch# $ 5>>=.5>>C

CA!ITA, E,IA)I,ITIES Capital "eserve and surplus 0eposit Sch & 5 6 ; 5>>= 75E,5:,G: 6'FF5,57,F7 ;6775&,'G:; 6:F'6,66,75

Rs in >>>Fs

5>>C 75E,5:,G: 5F&&F,FG,F5 6G'';E,'7,76 6'E;&,5;,;6

%hri Chinai College

7&

TYBBI

Commercial Banking

Borrowing ,ther liabilities Total Assets Cash D balance with "BI E 5:'FE,;5,7' 5&E75,F',6: 7 E'';5,57,FG DCCDCD?5A?@@ 77E:F,7E,GG <;<>5@?;D?<D

Balance with banks D money at call D short notice

55G:5,5E,7'

55:'F,5:,F5

Investments

&;:&;G,GG,57

&E576;,5;,&'

+dvances

66F66E,;:,67

5E&G'',:6,7:

@i4ed +ssets

&'

5G&G,GE,EF

5F75:66:

,ther assets

&&

575:56'E&

556G',G;,5E

Total

DCCDCD?5A?@@

<;<>5@?;D?<D

Contingent liabilities

&5

6'E7:','&,77

55,GGG,6F,F5

Bills for collection

566EF,7&,':

5'7:5,:767

Co""on si4e State"ent of S)I )an%

CA!ITA, E ,IA)I,ITIES

Sch

5>>=

Capital "eserves and %urplus

& 5

75E,5:,G: 6'FF5,57,F7

& 7

%hri Chinai College

75

TYBBI

Commercial Banking

0eposits Borrowings ,ther liabilities D )rovisions Total lia$ilities ASSETS Cash D balances with "BI Balance with banks D money at call D short notice Investments +dvances @i4ed +ssets ,ther assets Total Assets Contingent liabilities Bills for collection

6 ; 7

;6775&,'G:; 6:F'6,66,75 E'';5,57,FG DCCDCD?5A?@@

FF F &' 0>>

E F G : &' &&

5:'FE,;5,7' 55G:5,5E,7' &;:&;G,GG,57 66F66E,;:,67 5G&G,GE,EF 575:56'E&

7 ; 5E 7: & 7 0>> 7; ;

DCCDCD?5A?@@

&5

6'E7:','&,77 566EF,7&,':

Co"parati(e Si4e state"ent of S)I $an%

Capital DBiabilities

Capital "eserves and surplus 0eposits Borrowings

Sch

& 5 6 ;

5>>=

75E,5:,G: 6'FF5,57,F7 ;6775&,'G:; 6:F'6,66,75

5>>C

75E,5:,G: 5F&&F,FG,F5 6G'';E,'7,76 6'E;&,5;,;6

8ro7th

$ 6E7;,;F,'6 77;F7.'6,;& :'E5,':,':

I 2J3K2.3

$ &6 &7 6'

%hri Chinai College

76

TYBBI

Commercial Banking

,ther liabilities

E'';5,57,FG

77E:F,7E,GG

;6;;,EG,:'

Total ,ia$ilities

DCCDCD?5A?@@

<;<>5@?;D?<D

=5DAC?5@?<A

0D

Assets Cash D balance with "BI Balance with banks D money at call D short notice Investments +dvances @i4ed +ssets ,ther assets E F G : &' && 5:'FE,;5,7' 55G:5,5E,7' &;:&;G,GG,57 66F66E,;:,67 5G&G,GE,EF 575:56'E& 5&E75,F',6: 55:'F,5:,F5 &E576;,5;,&' 5E&G'',:6,7: 5F75:66: 556G',G;,5E F;56,F5,&& 8&7,'6,559 8&66G7,67,G79 F7767,77,FE E7:65G 5:&&;E67 6; 8'.&9 8G9 5: 5 &6

Total Assets

DCCDCD?5A?@@

<;<>5@?;D?<D

=5DAC?5@?<A

0D

Contingent liabilities &5 Bills for collection

6'E7:','&,77 566EF,7&,':

55,GGG,6F,F5 5'7:5,:767

FFF'G,E6,G6 5FF;,77,F;

6; &6

%hri Chinai College

7;

TYBBI

Commercial Banking

Trend Analysis

CA!ITA, E ,IA)I,ITIES Capital "eserve and surplus 0eposit Borrowing ,ther liabilities Total ASSETS Sch & 5 6 ; 7 5>>C 75E,5:,G: 5F&&F,FG,F5 6G'';E,'7,76 6'E;&,5;,;6 77E:F,7E,GG <;<>5@?;D?<D I &'' &'' &'' &'' &'' 0>> 5>>= 75E,5:,G: 6'FF5,57,F7 ;6775&,'G:; 6:F'6,66,75 E'';5,57,FG DCCDCD?5A?@@ I $ &&6 &&7 &6' &'G 00D

Cash D balance with "BI Balance with banks D money at call D short notice Investments

E F G

5&E75,F',6: 55:'F,5:,F5 &E576;,5;,&'

&'' &'' &''

5:'FE,;5,7' 55G:5,5E,7' &;:&;G,GG,57

&6; &'' :5

+dvances

5E&G'',:6,7:

&''

66F66E,;:,67

&5:

@i4ed +ssets ,ther assets

&'

5F75:66:

&''

5G&G,GE,EF

&'5

&&

556G',G;,5E

&''

575:56'E&

&&6

Total Assets

<;<>5@?;D?<D

0>>

DCCDCD?5A?@@

00D

Contingent liabilities

&5

55,GGG,6F,F5

&''

6'E7:','&,77

&6;'

Bills for collection

5'7:5,:767

&''

566EF,7&,':

&&6

%hri Chinai College

77

TYBBI

Commercial Banking

C'MME*TS: . Co""on si4e Analysis:. @rom the above common si e statement of S)I $an% we observe that the percentage of capital is almost same as compared to ICICI bank. %BI banks percentage of major funds from deposits and advances is high. The borrowed funds are also less which is again not a good sign. Hence they should introduce $orro7in and di(ersify their assets and funds1 +s we go through common si e balance sheet of ICICI $an% we see that percentage of capital of these bank is same as compared to %BI. 0eposits and advances is less over here, but its "eserves and surplus, borrowings, call money, etc. is high and we also know that its flow of funds is spread in other sources also. Co"parati(e Analysis: . Capital of ICICI bank has increased by &(, whereas capital of %BI has remained constant, but there is growth in capital of ICICI bank which indicate that this is having sound position in market. "eserves D %urplus of ICICI bank is appro4imately around &'(. But %BI bank has &6( which indicate ICICI bank have less "eserves D %urplus which is dangerous in future to e4pand D face challenges. 0eposits of ICICI B+/L is ;'( but %BI bank!s deposit is &7( due to which it has failed to raise fresh capital from potential or present customer.

%hri Chinai College

7E

TYBBI

Commercial Banking

Borrowing of ICICI bank is 66( and that of %BI is 6'(. + bank should borrow from outside to e4pand their work and business, which will increase their profitability growth. Cash in hand balance with other bank call money deposits of ICICI bank is high as compared to %BI bank which indicates that ICICI bank has good track record. The loans D advances of ICICI bank is also higher as compared to %BI bank, which shows ICICI bank is earning more interest profit.

Trend analysis#$ >hen we go through the trend analysis of %BI bank we can observe that even they are doing a fair business and are able to increase their customer base. The total asset of ICICI is increasing year by year and they are able to gain income, profit, D public confidence.

ICICI $an%: . >hen we go through trend analysis of ICICI bank, we see that there is a tremendous growth in capital, deposits and borrowings which shows that it has gained confidence of public and also its profit has gone satisfying upwards. +s far as total assets are concerned there has been tremendous increase in assets including loans D advances, investments, etc which shows that profits and incomes of ICICI bank are increasing.

S)I $an%: . >hen we go through trend analysis of %BI bank, we can find that there has been a very slow growth in deposits, borrowing and also in

%hri Chinai College 7F

TYBBI

Commercial Banking

capital, which shows that it has failed to attract the customers which has resulted in low profit margin and less incomes as compared to ICICI. +s far as the fi4ed assets are concerned they have increased by 5(. Boans and advances of %BI bank is showing less growth as compared to that of ICICI bank. Thus? 7e can conclude that the profit of ICICI $an% is "uch "ore than S)I $an%.

%hri Chinai College

7G

TYBBI

Commercial Banking

PERFORMANCE HIGHLIGHTS OF ICICI BANK

5% 15%

5%

1%

7%

Capital Reser es ! S"rpl"s #ep$sits B$rr$%i&'s Cas( )al* %it( RBI

67%

Fi+e, ! $t(er Assets

PERFORMANCE HIGHLIGHTS OF SBI BANK

7%

5%

5% 1% 5%

Capital Reser es ! S"rpl"s #ep$sits B$rr$%i&'s Cas( )al* %it( RBI Fi+e, ! Ot(er Assets

77%

%hri Chinai College

7:

TYBBI

Commercial Banking

CASE STU+Y '& ICICI )A*- E S)I )A*In spite of all this, the long case on ICICI is compelling. In my opinion, ICICIHs earnings growth will continue thanks to the rising middle class income in India. *ore and more people now have disposable income on their hands to buy car8s9, buy houses, invest or just plain deposit in the savings accounts. In speaking to a lot of my friends and family back in India, almost everyone from the younger generation prefers private banks like ICICI or %BI bank. The younger generation does not like government$owned banks because they do not understand the concept of ?customer service?$$ they treat you like they are doing you a favor by safe$keeping your hard$earned money. +verage salary increases in India are currently at 6'( and this alone gives people a lot of disposable income at hand. Co"petition and personal e#perience ICICI faces competition primarily from %BI bank, which is another growing bank in the private sector, as well as others like K0@C, Canara bank, and )unjab /ational Bank. But here we will focus on two banks ICICI and %BI. +lso, after having spoken to friends and family back in India, I got the impression that ICICI was more aggressive in terms of its marketing strategies as well as following$up with potential customers. ,ne of my uncle was trying to open up an /". savings account about a year back, he was e4ploring options with %BI as well as ICICI. +fter having emailed both through their respective company websites, he is still waiting on hearing back from %BI, whereas ICICI got in touch with him within ;G hours. This gave me the impression that if %BI bank did not care about a potential customer, it wouldnHt care much after we actually became their customer $ no points for guessing he finally ended up opening an account with %BI. Conclusion

+ll in all, I think ICICI has a very compelling growth story ahead of it as Indian economy continues to boom as we have seen above by doing analysis of the financial statements which is in the form of Common si e, Comparative and Trend analysis. %hri Chinai College E'

TYBBI

Commercial Banking

SHRI CHINAI COLLE E O! CO""ERCE # ECONO"ICS

Sur$ey for %ro&ect on Co''ercial (an)ing

NA"E* + ,ESI NATION* + SI NAT-RE* + CONTACT NO.* +

/0

,oes a Co''ercial (an) play a 'a&or role in growth # 1e$elop'ent of the country2 3es No

40 3ou open an account in a Co''ercial ban) for what reason2 High profits 6hy2 5uic) Ser$ices

70 How 8uic) is your Co''ercial (an) at respon1ing to your 8ueries # proble'2 %oor 6hy2 (a1 oo1 E9cellent

:0 In which areas of a co''ercial ban) you nee1 i'pro$e'ent2 Interest Ser$ice (eha$iours Sche'es Others

Co''ent for I'pro$e'ent*

%RO;ECT

-I,E* "rs. Leena Nair

Sur$ey con1ucte1 by*

%hri Chinai College

E&

TYBBI

Commercial Banking SARI<A. A. SHETT3 T3((I Roll No. <=

SI NAT-RE* ____________________

- Analysis &9 0oes a Commercial bank play a major role in growth and development of the countryO

-%

.ES NO

2/3

Analysis: @rom the above graph we can analy e that :5( of the people interviewed think that a Commercial Bank does play a major role in economic development whereas there are still G ( of them who don!t feel the same way. 59 Kow do you find depositing in a Commercial BankO

5DI

Si/ple C$/ple+

=DI

Analysis @rom the above graph we can analy e that F7( of the people interviewed find it convenient for depositing in a Commercial Bank, whereas 57( of the people find it difficult for depositing.

%hri Chinai College

E5

TYBBI

Commercial Banking

69

Kow 1uick is your Commercial Bank at responding to your 1ueries and problemO

5%

01%

P$$r Ba, G$$,

56%

E+2elle&t

15%

Analysis @rom the above graph we can analy e that 7E( of the people are contented with the way a commercial bank response to their 1ueries and problems. ;9 In which areas of a Commercial bank you need improvementO

00%

0% I&terest Ser i2e Be(a i$"r S2(e/es Ot(ers

51% -%

17%

Analysis @rom the above graph we can analy e that 7&( of the people want reasonable interest rates. +nd about 55( of the people want new, effective and efficient schemes to be introduced by the banks. +nd about

%hri Chinai College

E6

TYBBI

Commercial Banking

5F( of the people want convenient and effective services to be provided by commercial banks. C'*C,USI'*: @riends, as we know, over five decades the Commercial banks in India achieved astounding success by enormously spreading banking services in far$flung and unbanked areas of the country through their massive branch network are garnering burgeoning amount of savings which represent half of the 30) of the country. + major portion of these resources had been deployed to meet the needs of priority sectors which are critical to the economy. Kowever, it is crucial for the commercial banking industry to meet the increasingly comple4 savings and financing needs of the economy by offering a wider and fle4ible range of financial products tailored for all types of customers. In recent years, it is being felt widely that the commercial banking system has not actually grown as sound D vibrant as it needed to be. %trong capital positions and balance sheets places the Commercial banks in a better position to deal with and absorb the economic shocks. These Banks need to face competition without diluting the operating standards. In banking, there is no such thing as ?one si e fits all.? But todayHs commercial banks are more diverse than ever. YouHll find a tremendous range of opportunities in commercial banking, starting at the branch level because commercial bankers, now are highly e4perienced in working with businesses to develop the right financial package to meet your uni1ue business needs. The face of Commercial banking is changing rapidly. Competition is going to be tough Banks should avail of the e4isting and upcoming opportunities as well as address the above$discussed issues if they have to succeed, not just survive, in the changing environment. Thus, Commercial Banks occupy a dominant place in the money market, they are like a reservoir into which flow the savings, the idle

%hri Chinai College

E;

TYBBI

Commercial Banking

surplus, money of households and from which loans are given on interest to businessmen D others who need them for investment or productive uses. REC'MME*+ATI'*S

Banking in India has made a remarkable progress in its growth and e4pansion, as well as business with social perspective in the fulfillment of national objectives. Indian Commercial banking has developed, but, its perfection is yet to be seen. There still remains many tasks to be fulfilled. &. %till there are villages left without banking facilities, so many more rural banks branches need to be opened. 5. Puality of Commercial banking facilities should be improved to the atmost satisfaction of the customer. 6. ,perational costs of Commercial banks should be reduced to the minimum profitability and working results must be ma4imi ed. ;. Banking staff should be ade1uately trained. 7. *ore lending should be made in favour of priority sectors. E. *alpractices, fraud, corruption and red$tapism must be done away with. F. *ore attention should be paid to the development of e4ports. G. /ationalised banks should give more technical assistance to the small industrialists. :. Interest rates on deposits should be enhanced reasonably up to &5$&6 ( so that savers get their legitimate returns. &'. The high level of overdues of banks have become a matter of concern. %o, banks should make all possible efforts to reduce their overdues. This all re1uires that no loans should be given without proper identification and address of the deserving rural poor. Thus, in order that the association of banks with industry is more fruitful and rewarding, many innovations have to be planned and introduced

%hri Chinai College

E7

TYBBI

Commercial Banking

systematically and greater degree of managerial competence will have to be developed in Commercial banking sector. &UTURE !R'S!ECTS '& C'MMERCIA, )A*-I*8:

Indian banking has developed. But, its perfection is yet to be seen. There still remain many tasks to be fulfilled. Kistorically, profitability from lending activities has been cyclic and dependent on the needs and strengths of loan customers. In recent history, investors have demanded a more stable revenue stream and banks have therefore placed more emphasis on transaction fees, primarily loan fees but also including service charges on array of deposit activities and ancillary services 8international banking, foreign e4change, insurance, investments, wire transfers, etc9. Kowever, lending activities still provides and in future? too will provide bulk of a Commercial bankHs income. +s part of the financial services industry, commercial banking are worldwide attempting to compete better by improving core operations and differentiating the customer e4perience. The banking sector has been consolidating2 it is worth noting that far more people are employed in the Commercial banking sector than any other part of the financial services industry. Aobs in banking can be e4citing and offer e4cellent opportunities to learn about business, interact with people and build up a clientele. In future, if we are well$prepared and enthusiastic about entering the field, we are likely to find a wide variety of opportunities open to us. Thus, we can predict the future of Commercial bank, to be spreaded world wide. They will be providing an unprecedented level of service to a wide range of business clients, from small business, through to multi$national corporate clients. In future, Commercial Bank will come up with more

%hri Chinai College

EE

TYBBI

Commercial Banking