You might also like

- Chapter 5Document5 pagesChapter 5Abrha636No ratings yet

- ACTBAS 2 - Lecture 7 Internal Control and Cash, Bank ReconciliationDocument5 pagesACTBAS 2 - Lecture 7 Internal Control and Cash, Bank ReconciliationJason Robert MendozaNo ratings yet

- ch08 ProblemDocument9 pagesch08 Problemapi-281193111No ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document18 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- 2009 F-1 Class NotesDocument4 pages2009 F-1 Class NotesgqxgrlNo ratings yet

- ACTBAS 2 - Lecture 1 Merchandising Business and Inventory SystemDocument7 pagesACTBAS 2 - Lecture 1 Merchandising Business and Inventory SystemJason Robert MendozaNo ratings yet

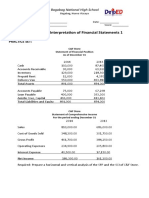

- Practice Set - Analysis of FS1Document1 pagePractice Set - Analysis of FS1marissa casareno almueteNo ratings yet

- Chapter 2b Bank ReconciliationDocument17 pagesChapter 2b Bank ReconciliationFreziel Jade NatividadNo ratings yet

- Financial Accounting and Reporting 1Document16 pagesFinancial Accounting and Reporting 1LIM HUI NI STUDENTNo ratings yet

- Chapter 2 Problems and Solutions EnglishDocument8 pagesChapter 2 Problems and Solutions EnglishyandaveNo ratings yet

- Rancho Foods Deposits All Cash Receipts Each Wednesday and FridayDocument1 pageRancho Foods Deposits All Cash Receipts Each Wednesday and FridayAmit PandeyNo ratings yet

- Financial Accounting (International) : Fundamentals Pilot Paper - Knowledge ModuleDocument19 pagesFinancial Accounting (International) : Fundamentals Pilot Paper - Knowledge ModuleNguyen Thi Phuong ThuyNo ratings yet

- Accounts - Bank Reconciliation StatementDocument18 pagesAccounts - Bank Reconciliation StatementAnuj KutalNo ratings yet

- Accounting Business Law FinanceDocument8 pagesAccounting Business Law FinanceromeeNo ratings yet

- Merchandising Operations - CRDocument21 pagesMerchandising Operations - CRNicole CagasNo ratings yet

- Chapter 2 - Accounting PrinciplesDocument36 pagesChapter 2 - Accounting PrinciplesIbni Amin100% (2)

- I Practice of Horizontal & Verticle Analysis Activity IDocument3 pagesI Practice of Horizontal & Verticle Analysis Activity IZarish AzharNo ratings yet

- Journal, Ledger, TB & Final AccountsDocument11 pagesJournal, Ledger, TB & Final AccountsSanjay Dutta100% (1)

- Financial Accounting and ReportingDocument9 pagesFinancial Accounting and ReportingSisir ShowNo ratings yet

- Auditing The Revenue Cycle: ©Mcgraw-Hill EducationDocument36 pagesAuditing The Revenue Cycle: ©Mcgraw-Hill EducationNabila SedkiNo ratings yet

- ACC 211 - Review 2 (Chapters 5, 6, & 7)Document4 pagesACC 211 - Review 2 (Chapters 5, 6, & 7)Brennan Patrick WynnNo ratings yet

- 2016-17 Skilled Occupation List: Submission From Cpa Australia To The Department of EducationDocument50 pages2016-17 Skilled Occupation List: Submission From Cpa Australia To The Department of EducationgamunozdNo ratings yet

- Not For Profit EntitiesDocument57 pagesNot For Profit EntitiesGreg DomingoNo ratings yet

- ACCY 201 Exam 2 Study GuideDocument42 pagesACCY 201 Exam 2 Study GuideKelly WilliamsNo ratings yet

- Chapter 1 ExerciseDocument11 pagesChapter 1 ExerciseUsama MukhtarNo ratings yet

- FAR Notes Chapter 3Document3 pagesFAR Notes Chapter 3jklein2588No ratings yet

- AssignmentDocument8 pagesAssignmentNegil Patrick DolorNo ratings yet

- Advanced Accounting: Solutions Manual For Use WithDocument3 pagesAdvanced Accounting: Solutions Manual For Use Withlottie100% (1)

- CPAR Intro To Income Tax and Tax On Individuals (Batch 89) - HandoutDocument29 pagesCPAR Intro To Income Tax and Tax On Individuals (Batch 89) - HandoutMark LapidNo ratings yet

- Chapter 3 Inventories and Cost of Goods SoldDocument84 pagesChapter 3 Inventories and Cost of Goods SoldSampanna Shrestha100% (1)

- Understanding Capital MarketsDocument15 pagesUnderstanding Capital MarketsSakthirama VadiveluNo ratings yet

- Answer Key Theories BQTAP Review 2018 2019Document12 pagesAnswer Key Theories BQTAP Review 2018 2019Illion IllionNo ratings yet

- 0 Accounting For Merchandising BusinessDocument114 pages0 Accounting For Merchandising BusinessIan RanilopaNo ratings yet

- ACC 211 - Review 2 (Chapters 5, 6, & 7) SolutionDocument5 pagesACC 211 - Review 2 (Chapters 5, 6, & 7) SolutionBrennan Patrick WynnNo ratings yet

- 23 Working Capital ManagementDocument98 pages23 Working Capital ManagementMittal Shah100% (1)

- FINN 400 Quiz Set Section 1 Key Spring 2017Document32 pagesFINN 400 Quiz Set Section 1 Key Spring 2017MeherJazibAliNo ratings yet

- HRM MidtermDocument16 pagesHRM MidtermJsn Pl Cabg-sNo ratings yet

- Foreign Currency Translation - Modified.aDocument71 pagesForeign Currency Translation - Modified.asamuel debebeNo ratings yet

- Financial Accounting - TheoriesDocument5 pagesFinancial Accounting - TheoriesKim Cristian MaañoNo ratings yet

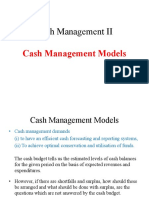

- Cash Management ModelsDocument12 pagesCash Management ModelsNayan kaki100% (1)

- Merchandising OperationsDocument27 pagesMerchandising OperationsAbegail Lheani GuiaNo ratings yet

- 4 - Bonuses & Current LiabilitiesDocument43 pages4 - Bonuses & Current Liabilitiesyatot carbonelNo ratings yet

- Chapter07 - AnswerDocument18 pagesChapter07 - AnswerkdsfeslNo ratings yet

- Financial Accounting and Reporting Part 1Document10 pagesFinancial Accounting and Reporting Part 1shelou_domantayNo ratings yet

- MS Preweek - Theories (B44)Document12 pagesMS Preweek - Theories (B44)Abigail VenancioNo ratings yet

- Accounting Cycle Exercises IIIDocument34 pagesAccounting Cycle Exercises IIIIanWest0% (1)

- Financial Mathematics For ActuariesDocument62 pagesFinancial Mathematics For ActuariesbreezeeeNo ratings yet

- Business Combinations - ASPEDocument3 pagesBusiness Combinations - ASPEShariful HoqueNo ratings yet

- What's A Bond?: What's A Bond? Types of Bonds Bond Valuation Techniques The Bangladeshi Bond Market Problem SetDocument30 pagesWhat's A Bond?: What's A Bond? Types of Bonds Bond Valuation Techniques The Bangladeshi Bond Market Problem SetpakhijuliNo ratings yet

- ACC 304 Week 2 Quiz 01 - Chapter 8Document6 pagesACC 304 Week 2 Quiz 01 - Chapter 8LereeNo ratings yet

- Wages and Salaries: What's The Difference?Document15 pagesWages and Salaries: What's The Difference?Shahriar IslamNo ratings yet

- Personal and Household FinanceDocument5 pagesPersonal and Household FinanceMuhammad SamhanNo ratings yet

- Finance Chpter 5 Time Value of MoneyDocument11 pagesFinance Chpter 5 Time Value of MoneyOmar Ahmed ElkhalilNo ratings yet

- Acct 1 Bexam 1 SampleDocument22 pagesAcct 1 Bexam 1 SampleMarvin_Chan_2123No ratings yet

- Accounting For Business Combination PDFDocument13 pagesAccounting For Business Combination PDFSamuel FerolinoNo ratings yet

- Accounting Cash Internal ControlsDocument14 pagesAccounting Cash Internal ControlsDave A ValcarcelNo ratings yet

- Accounting For Cash and ReceivableDocument7 pagesAccounting For Cash and ReceivableAbrha GidayNo ratings yet

- Step BankDocument4 pagesStep BankSamrawit MewaNo ratings yet

- Chapter 7 Question Review PDFDocument12 pagesChapter 7 Question Review PDFChit ComisoNo ratings yet

- QA Accounting For DepreciationDocument7 pagesQA Accounting For DepreciationAhmed RawyNo ratings yet

- Fa 6 CH 04 SDocument23 pagesFa 6 CH 04 SAhmed RawyNo ratings yet

- Chpater 4 SolutionsDocument13 pagesChpater 4 SolutionsAhmed Rawy100% (1)

- CHAPTER 10 Plant Assets and Intangibles: Objective 1: Measure The Cost of A Plant AssetDocument9 pagesCHAPTER 10 Plant Assets and Intangibles: Objective 1: Measure The Cost of A Plant AssetAhmed RawyNo ratings yet

- CHAPTER 7 Accounting Information SystemsDocument6 pagesCHAPTER 7 Accounting Information SystemsAhmed RawyNo ratings yet

- Long-Term Assets: 0reviewing The ChapterDocument8 pagesLong-Term Assets: 0reviewing The ChapterAhmed RawyNo ratings yet

- CHAPTER 8 Internal Control and CashDocument8 pagesCHAPTER 8 Internal Control and CashAhmed RawyNo ratings yet

- V. Internal Control & Banking Relationship: Basic ControlsDocument5 pagesV. Internal Control & Banking Relationship: Basic ControlsAhmed RawyNo ratings yet

- CHAPTER 9 ReceivablesDocument9 pagesCHAPTER 9 ReceivablesAhmed RawyNo ratings yet

- 06 OutlinesDocument5 pages06 OutlinesAhmed RawyNo ratings yet

- Revision CH 1 ManagementDocument61 pagesRevision CH 1 ManagementAhmed RawyNo ratings yet

- Revision CH 1 ManagementDocument61 pagesRevision CH 1 ManagementAhmed RawyNo ratings yet

- MCMCHistoryDocument18 pagesMCMCHistoryAli S.No ratings yet

- Ammonia Material BalanceDocument7 pagesAmmonia Material BalanceSiva KumarNo ratings yet

- Uniarch Network Video Recorders User Manual-V1.00Document99 pagesUniarch Network Video Recorders User Manual-V1.00amurjiantoNo ratings yet

- Manaloto V Veloso IIIDocument4 pagesManaloto V Veloso IIIJan AquinoNo ratings yet

- Functional Specifications For Purchase Order: 1. Business RequirementsDocument5 pagesFunctional Specifications For Purchase Order: 1. Business RequirementsTom MarksNo ratings yet

- User's Guide: Smartpack2 Master ControllerDocument32 pagesUser's Guide: Smartpack2 Master Controllermelouahhh100% (1)

- My Linux Attack Commands-ADocument51 pagesMy Linux Attack Commands-Aapogee.protectionNo ratings yet

- Invoice SummaryDocument2 pagesInvoice SummarymuNo ratings yet

- GB Programme Chart: A B C D J IDocument2 pagesGB Programme Chart: A B C D J IRyan MeltonNo ratings yet

- Autodesk Inventor Practice Part DrawingsDocument25 pagesAutodesk Inventor Practice Part DrawingsCiprian Fratila100% (1)

- Principles of Care-Nursing For Children: Principle DescriptionDocument3 pagesPrinciples of Care-Nursing For Children: Principle DescriptionSanthosh.S.UNo ratings yet

- Aerated Static Pile Composting (ASP) VS Aerated (Turned) Windrow CompostingDocument2 pagesAerated Static Pile Composting (ASP) VS Aerated (Turned) Windrow CompostingRowel GanzonNo ratings yet

- 3rd Term s1 Agricultural Science 1Document41 pages3rd Term s1 Agricultural Science 1Adelowo DanielNo ratings yet

- 3 CBLSF 50 HDocument6 pages3 CBLSF 50 HNaz LunNo ratings yet

- TUF-2000M User Manual PDFDocument56 pagesTUF-2000M User Manual PDFreinaldoNo ratings yet

- Final Report Air ConditioningDocument42 pagesFinal Report Air ConditioningAzmi Matali73% (11)

- Slid e 4-1Document67 pagesSlid e 4-1Rashe FasiNo ratings yet

- Product Sold by APPLE AustraliaDocument1 pageProduct Sold by APPLE AustraliaImran KhanNo ratings yet

- Intel Core - WikipediaDocument16 pagesIntel Core - WikipediaEEBB0% (1)

- XXX RadiographsDocument48 pagesXXX RadiographsJoseph MidouNo ratings yet

- ALP Final Test KeyDocument3 pagesALP Final Test KeyPetro Nela50% (2)

- 785 TrucksDocument7 pages785 TrucksJavier Pagan TorresNo ratings yet

- Apples-to-Apples in Cross-Validation Studies: Pitfalls in Classifier Performance MeasurementDocument9 pagesApples-to-Apples in Cross-Validation Studies: Pitfalls in Classifier Performance MeasurementLuis Martínez RamírezNo ratings yet

- SIConitDocument2 pagesSIConitJosueNo ratings yet

- United States Court of Appeals, Third CircuitDocument18 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- Node MCU CarDocument4 pagesNode MCU CarYusuf MuhthiarsaNo ratings yet

- Diesel Oil Matters 70 YrsDocument1 pageDiesel Oil Matters 70 YrsingsespinosaNo ratings yet

- Remedial Law Syllabus 2013Document6 pagesRemedial Law Syllabus 2013Mirriam Ebreo100% (1)

- 150 67-Eg1Document104 pages150 67-Eg1rikoNo ratings yet

- Santa Letters 2013Document16 pagesSanta Letters 2013Lebanon_PublishingNo ratings yet

- The Voice of God: Experience A Life Changing Relationship with the LordFrom EverandThe Voice of God: Experience A Life Changing Relationship with the LordNo ratings yet

- From Raindrops to an Ocean: An Indian-American Oncologist Discovers Faith's Power From A PatientFrom EverandFrom Raindrops to an Ocean: An Indian-American Oncologist Discovers Faith's Power From A PatientRating: 1 out of 5 stars1/5 (1)