You might also like

- The Carry Trade and FundamentalsDocument36 pagesThe Carry Trade and FundamentalsJean-Jacques RousseauNo ratings yet

- Exchange Rate Determination Puzzle: Long Run Behavior and Short Run DynamicsFrom EverandExchange Rate Determination Puzzle: Long Run Behavior and Short Run DynamicsNo ratings yet

- Bond Spreads - Leading Indicator For CurrenciesDocument6 pagesBond Spreads - Leading Indicator For CurrenciesanandNo ratings yet

- Risk On Risk Off 1Document16 pagesRisk On Risk Off 1ggerszteNo ratings yet

- Strategic and Tactical Asset Allocation: An Integrated ApproachFrom EverandStrategic and Tactical Asset Allocation: An Integrated ApproachNo ratings yet

- Carry Trade and Liquidity Risk Evidence From Forward and Cross-Currency Swap Markets - Y Chang E Schlogl - 2012Document35 pagesCarry Trade and Liquidity Risk Evidence From Forward and Cross-Currency Swap Markets - Y Chang E Schlogl - 2012Duncan van TongerenNo ratings yet

- Sectors and Styles: A New Approach to Outperforming the MarketFrom EverandSectors and Styles: A New Approach to Outperforming the MarketRating: 1 out of 5 stars1/5 (1)

- Predictive Power of Weekly Fund Flows: Equity StrategyDocument32 pagesPredictive Power of Weekly Fund Flows: Equity StrategyCoolidgeLowNo ratings yet

- The High Frequency Game Changer: How Automated Trading Strategies Have Revolutionized the MarketsFrom EverandThe High Frequency Game Changer: How Automated Trading Strategies Have Revolutionized the MarketsNo ratings yet

- JPM Flows Liquidity 2016-10-07 2145906Document18 pagesJPM Flows Liquidity 2016-10-07 2145906chaotic_pandemoniumNo ratings yet

- FX Composite InstitutionalDocument1 pageFX Composite InstitutionalDanger AlvarezNo ratings yet

- Understanding Eurodollar FuturesDocument24 pagesUnderstanding Eurodollar FuturesOrestis :. KonstantinidisNo ratings yet

- Lifespan Investing: Building the Best Portfolio for Every Stage of Your LifeFrom EverandLifespan Investing: Building the Best Portfolio for Every Stage of Your LifeNo ratings yet

- CBOT-Understanding BasisDocument26 pagesCBOT-Understanding BasisIshan SaneNo ratings yet

- Stock Volatility Predictability in Bull and Bear MarketsDocument20 pagesStock Volatility Predictability in Bull and Bear MarketsnonameNo ratings yet

- The IBS Effect Mean Reversion in Equity ETFsDocument31 pagesThe IBS Effect Mean Reversion in Equity ETFstylerduNo ratings yet

- Sortino - A "Sharper" Ratio! - Red Rock CapitalDocument6 pagesSortino - A "Sharper" Ratio! - Red Rock CapitalInterconti Ltd.No ratings yet

- FX Deal ContingentDocument23 pagesFX Deal ContingentJustinNo ratings yet

- Credit Quant SightDocument26 pagesCredit Quant SightmarioturriNo ratings yet

- Nomura Correlation PrimerDocument16 pagesNomura Correlation PrimershortmycdsNo ratings yet

- Information Theory and Market BehaviorDocument25 pagesInformation Theory and Market BehaviorAbhinavJainNo ratings yet

- Saxo Asset Allocation - 20090804Document5 pagesSaxo Asset Allocation - 20090804Trading Floor100% (2)

- Proprietary Trading Activities in TVSCCDocument26 pagesProprietary Trading Activities in TVSCCTrang Cao ThượngNo ratings yet

- DeutscheBank FX Guide May 02Document160 pagesDeutscheBank FX Guide May 02michaelruanNo ratings yet

- Demystifying Managed FuturesDocument29 pagesDemystifying Managed Futuresjchode69No ratings yet

- Quant FinanceDocument43 pagesQuant FinanceEpahNo ratings yet

- An Introduction To Volatility, VIX, and VXX: What Is Volatility? Volatility. Realized Volatility Refers To HowDocument8 pagesAn Introduction To Volatility, VIX, and VXX: What Is Volatility? Volatility. Realized Volatility Refers To Howchris mbaNo ratings yet

- FX 102 - FX Rates and ArbitrageDocument32 pagesFX 102 - FX Rates and Arbitragetesting1997No ratings yet

- CDO Base CorrelationsDocument7 pagesCDO Base Correlationsmexicocity78No ratings yet

- Ambrus Capital - Volatility and The Changing Market Structure Driving U.S. EquitiesDocument18 pagesAmbrus Capital - Volatility and The Changing Market Structure Driving U.S. EquitiespiwipebaNo ratings yet

- Central Banks Blowing BubblesDocument11 pagesCentral Banks Blowing BubblesBisto MasiloNo ratings yet

- Introduction To Interest Rate Trading: Andrew WilkinsonDocument44 pagesIntroduction To Interest Rate Trading: Andrew WilkinsonLee Jia QingNo ratings yet

- SSRN Id2607730Document84 pagesSSRN Id2607730superbuddyNo ratings yet

- Nyc VolDocument112 pagesNyc VolelftyNo ratings yet

- Volatility DerivativesDocument21 pagesVolatility DerivativesjohamarNo ratings yet

- Understanding Convertibles IES 016Document2 pagesUnderstanding Convertibles IES 016Arjun GhoseNo ratings yet

- Stock Gap Research Paper Dow AwardDocument21 pagesStock Gap Research Paper Dow AwardContra_hourNo ratings yet

- Final Project On Volatility - New 2Document99 pagesFinal Project On Volatility - New 2vipul099No ratings yet

- Man AHL Analysis CTA Intelligence - On Trend-Following CTAs and Quant Multi-Strategy Funds ENG 20140901Document1 pageMan AHL Analysis CTA Intelligence - On Trend-Following CTAs and Quant Multi-Strategy Funds ENG 20140901kevinNo ratings yet

- Index Futures RMFDDocument17 pagesIndex Futures RMFDAbhi_The_RockstarNo ratings yet

- Gamma Vanna and Higher Greek Exposure - Compiling The Dealer Order BookDocument9 pagesGamma Vanna and Higher Greek Exposure - Compiling The Dealer Order BookArnaud FreycenetNo ratings yet

- Introduction & Research: Factor InvestingDocument44 pagesIntroduction & Research: Factor InvestingMohamed HussienNo ratings yet

- Default Risk Contagion - NomuraDocument26 pagesDefault Risk Contagion - NomuraJeff McGinnNo ratings yet

- 07a Hedge Funds and Performance EvaluationDocument66 pages07a Hedge Funds and Performance EvaluationdesbiauxNo ratings yet

- A Quantitative Approach To Tactical Asset Allocation Mebane FaberDocument47 pagesA Quantitative Approach To Tactical Asset Allocation Mebane FaberaliasadsjNo ratings yet

- Trade Score PDFDocument30 pagesTrade Score PDFvenkat.sqlNo ratings yet

- Fair Value Model - Hardcoded DateDocument9 pagesFair Value Model - Hardcoded DateforexNo ratings yet

- Volatility Radar: Profit From Low Vol and High SkewDocument14 pagesVolatility Radar: Profit From Low Vol and High SkewTze ShaoNo ratings yet

- Risk Management Through Forex Derivatives: Presented ByDocument31 pagesRisk Management Through Forex Derivatives: Presented ByRoma ManwaniNo ratings yet

- Structured Note On Emerging Market Currency BasketDocument4 pagesStructured Note On Emerging Market Currency Basketchandkhand2No ratings yet

- Practical Relative-Value Volatility Trading: Stephen Blyth, Managing Director, Head of European Arbitrage TradingDocument23 pagesPractical Relative-Value Volatility Trading: Stephen Blyth, Managing Director, Head of European Arbitrage TradingArtur SilvaNo ratings yet

- Pricing and Hedging of Japan Equity-Linked Power Reverse Dual NoteDocument59 pagesPricing and Hedging of Japan Equity-Linked Power Reverse Dual NoteFrank FungNo ratings yet

- Creating A Heirarchy of Trading DecisionsDocument6 pagesCreating A Heirarchy of Trading DecisionsWayne H WagnerNo ratings yet

- BofA - FX Quant Signals For The FOMC and ECB 20230130Document9 pagesBofA - FX Quant Signals For The FOMC and ECB 20230130G.Trading.FxNo ratings yet

- Dow TheoryDocument17 pagesDow TheoryrahmathahajabaNo ratings yet

- Deep HedgingDocument21 pagesDeep HedgingRaju KaliperumalNo ratings yet

- Goldman Sachs 2013 Macro ConfDocument133 pagesGoldman Sachs 2013 Macro ConfIbn Faqir Al ComillaNo ratings yet

- Tips InvestingDocument12 pagesTips InvestingIbn Faqir Al ComillaNo ratings yet

- Cboe Vix IndexDocument19 pagesCboe Vix IndexdimitrioschrNo ratings yet

- Repo Market PrimerDocument11 pagesRepo Market PrimerVictor SwishchukNo ratings yet

- 2012 Ibm Annual PDFDocument146 pages2012 Ibm Annual PDFIbn Faqir Al ComillaNo ratings yet

- Gold Renminbi Multi-Currency Reserve SystemDocument44 pagesGold Renminbi Multi-Currency Reserve SystemIbn Faqir Al ComillaNo ratings yet

- Bursting The Bond BubbleDocument10 pagesBursting The Bond BubbleIbn Faqir Al ComillaNo ratings yet

- SP 500 Eps EstDocument42 pagesSP 500 Eps EstIbn Faqir Al ComillaNo ratings yet

- GMAT GRE QuestionsDocument5 pagesGMAT GRE QuestionsIbn Faqir Al ComillaNo ratings yet

- Corporate Yields Interest RatesDocument12 pagesCorporate Yields Interest RatesIbn Faqir Al ComillaNo ratings yet

- SSRN Id2078535Document48 pagesSSRN Id2078535AdminAliNo ratings yet

- P 38Document26 pagesP 38Ibn Faqir Al ComillaNo ratings yet

- Final Project ReportDocument51 pagesFinal Project ReportmadhumdkNo ratings yet

- Capital MarketsDocument2 pagesCapital MarketsAzzi SabaniNo ratings yet

- Chap 022Document44 pagesChap 022ducacapupuNo ratings yet

- Summary of Fund Perf - Sept 2012 LIFE ACCOUNTDocument4 pagesSummary of Fund Perf - Sept 2012 LIFE ACCOUNTJohn SmithNo ratings yet

- Solutions To Selected End-Of-Chapter Questions Chapters 1 Through 7Document73 pagesSolutions To Selected End-Of-Chapter Questions Chapters 1 Through 7Linh Tc85% (52)

- Musings Reverse Robin HoodDocument5 pagesMusings Reverse Robin HoodZerohedgeNo ratings yet

- Far-1 4Document3 pagesFar-1 4Raymundo Eirah100% (1)

- Basics of Mutual FundsDocument10 pagesBasics of Mutual FundsKeyur ShahNo ratings yet

- Chapter 20: Options Markets: Introduction: Problem SetsDocument19 pagesChapter 20: Options Markets: Introduction: Problem SetsAuliah SuhaeriNo ratings yet

- Engineering Economics, ENGR 610: Quiz-3&4, Take Home (15%)Document2 pagesEngineering Economics, ENGR 610: Quiz-3&4, Take Home (15%)Sayyadh Rahamath BabaNo ratings yet

- Money Habits Cheat SheetDocument9 pagesMoney Habits Cheat Sheetned100% (1)

- Accounting 202 Notes - David HornungDocument28 pagesAccounting 202 Notes - David HornungAvi Goodstein100% (1)

- Corporate Finance (Chapter 4) (7th Ed)Document27 pagesCorporate Finance (Chapter 4) (7th Ed)Israt Mustafa100% (1)

- Cost Classification: Total Product/ ServiceDocument21 pagesCost Classification: Total Product/ ServiceThureinNo ratings yet

- Ap Prob 8Document2 pagesAp Prob 8jhobsNo ratings yet

- Financial EngineeringDocument18 pagesFinancial Engineeringtanay-mehta-3589100% (1)

- Dalbar Qaib 2008Document12 pagesDalbar Qaib 2008Russ Thornton100% (2)

- A Comprehensive Reviewer For Usury LawDocument4 pagesA Comprehensive Reviewer For Usury LawCarla Reyes50% (2)

- Handbook On SecurityDocument166 pagesHandbook On SecurityFile ArchiveNo ratings yet

- ACCT5170 Syllabus - 2023Document7 pagesACCT5170 Syllabus - 2023bafsvideo4No ratings yet

- Option Valuation PDFDocument264 pagesOption Valuation PDFshudhai jobe100% (1)

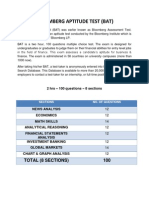

- Bloomberg Aptitude Test (BAT)Document10 pagesBloomberg Aptitude Test (BAT)Shivgan Joshi100% (1)

- Module 1 - Overview of SukukDocument36 pagesModule 1 - Overview of SukukArun Kumar MurugasuNo ratings yet

- Financial Market and InstitutionsDocument43 pagesFinancial Market and Institutionsdhiviraj100% (3)

- Gold Not Oil InflationDocument8 pagesGold Not Oil Inflationpderby1No ratings yet

- BDO v. RepublicDocument4 pagesBDO v. RepublicBojo100% (1)

- Accounting Chap 10 - Sheet1Document2 pagesAccounting Chap 10 - Sheet1Nguyễn Ngọc Mai100% (1)

- FinanceanswersDocument24 pagesFinanceanswersAditi ToshniwalNo ratings yet

- MKT IBoxx BrochureDocument12 pagesMKT IBoxx Brochurealanpicard2303No ratings yet

- Bean (Basic) : Required: (ACCA SBR Kaplan Book) 19Document1 pageBean (Basic) : Required: (ACCA SBR Kaplan Book) 19.No ratings yet

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsFrom EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsRating: 5 out of 5 stars5/5 (1)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistFrom EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistRating: 4 out of 5 stars4/5 (32)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Mind over Money: The Psychology of Money and How to Use It BetterFrom EverandMind over Money: The Psychology of Money and How to Use It BetterRating: 4 out of 5 stars4/5 (24)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)