You might also like

- European Financial Supervision PDFDocument18 pagesEuropean Financial Supervision PDFChiliban CristieanNo ratings yet

- De Larosiere Report enDocument86 pagesDe Larosiere Report enMortimer37No ratings yet

- Key Regional and International Bodies and Fora For The Financial MarketsDocument9 pagesKey Regional and International Bodies and Fora For The Financial MarketsdanoantaNo ratings yet

- OECDocument3 pagesOECAncaIlieNo ratings yet

- When The Crowd Fights CorruptionDocument8 pagesWhen The Crowd Fights CorruptionAlexandra Ştefania OpreaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- US Internal Revenue Service: p1438Document518 pagesUS Internal Revenue Service: p1438IRSNo ratings yet

- Inter-regional disparities in industrial growthDocument100 pagesInter-regional disparities in industrial growthrks_rmrctNo ratings yet

- Ud. Wirastri Jurnal Penerimaan Kas Desember 2015Document40 pagesUd. Wirastri Jurnal Penerimaan Kas Desember 2015Raihan FatihaNo ratings yet

- Neoliberalising The Urban New Geographies of Power and Injustice in Indian CitiesDocument13 pagesNeoliberalising The Urban New Geographies of Power and Injustice in Indian CitiesHash SinghNo ratings yet

- Chapter One - Part 1Document21 pagesChapter One - Part 1ephremNo ratings yet

- Optional Credit RemovalDocument3 pagesOptional Credit RemovalKNOWLEDGE SOURCENo ratings yet

- Travel Insurance CertificateDocument2 pagesTravel Insurance CertificateLee Mccray100% (1)

- 12 Jun 2019 PDFDocument12 pages12 Jun 2019 PDFAnonymous dy7g4jzo7No ratings yet

- Preparing The Philippines For The 4th Industrial Revo PIDS Report 2017-2018Document120 pagesPreparing The Philippines For The 4th Industrial Revo PIDS Report 2017-2018Rico EstarasNo ratings yet

- Dissertation Ulrich BobeDocument5 pagesDissertation Ulrich BobeBuyPapersForCollegeOnlineCanada100% (1)

- 2012 - Communities Cagayan Incorporated Vs Nanol, GR 176791, November 14, 2012Document1 page2012 - Communities Cagayan Incorporated Vs Nanol, GR 176791, November 14, 2012Lyka Lim Pascua100% (1)

- Recovery Catalytic Converters RefiningDocument20 pagesRecovery Catalytic Converters RefiningAFLAC ............80% (5)

- Week 8Document2 pagesWeek 8Nikunj D Patel100% (1)

- Employment Growth Informalisation and Other IssuesDocument23 pagesEmployment Growth Informalisation and Other IssuesRiya Singh100% (1)

- Immelt's Reinvention of GEDocument5 pagesImmelt's Reinvention of GEbodhi_bg100% (1)

- Form 32 A Central: Treasury or Sub TreasuryDocument1 pageForm 32 A Central: Treasury or Sub TreasuryMuhammad AsifNo ratings yet

- Prime HR & Security Solutions PVT LTD: SUB: Appointment As HR ExecutiveDocument3 pagesPrime HR & Security Solutions PVT LTD: SUB: Appointment As HR ExecutivesayalikNo ratings yet

- More Unanswered QuestionsDocument8 pagesMore Unanswered QuestionspermaculturistNo ratings yet

- Monopoly: Principles of Microeconomics Douglas Curtis & Ian IrvineDocument36 pagesMonopoly: Principles of Microeconomics Douglas Curtis & Ian IrvineNameNo ratings yet

- PDFDocument16 pagesPDFAnil KhadkaNo ratings yet

- Booking ConfirmationDocument5 pagesBooking ConfirmationAnonymous uqL4XaNo ratings yet

- Time-Table - BBA 3rd SemesterDocument2 pagesTime-Table - BBA 3rd SemesterSunny GoyalNo ratings yet

- Steel CH 1Document34 pagesSteel CH 1daniel workuNo ratings yet

- Case 03 - Walmart Case NoteDocument3 pagesCase 03 - Walmart Case Notemarcole198440% (5)

- Comparative Analysis of Public & Private Bank (Icici &sbi) - 1Document108 pagesComparative Analysis of Public & Private Bank (Icici &sbi) - 1Sami Zama100% (1)

- Local Business EnvironmentDocument3 pagesLocal Business EnvironmentJayMoralesNo ratings yet

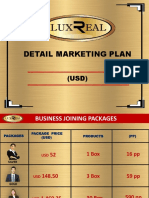

- Luxreal Detail Marketing Plan (2019) UsdDocument32 pagesLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- Portfolio Management - Chapter 7Document85 pagesPortfolio Management - Chapter 7Dr Rushen SinghNo ratings yet

- Can China Keep Rising Despite US PushbackDocument9 pagesCan China Keep Rising Despite US PushbackVidas ŽūkasNo ratings yet

- Opportunity CostDocument1 pageOpportunity Costvaibhav67% (3)