You might also like

- 9swap Trading FT April 2013Document1 page9swap Trading FT April 2013Rajat KaushikNo ratings yet

- FICM Class Evaluation 2013 14Document1 pageFICM Class Evaluation 2013 14Rajat KaushikNo ratings yet

- Swap Traders' Morning Fix Under Scrutiny: by Michael Mackenzie, Tom Braithwaite and Kara Scannell in New YorkDocument4 pagesSwap Traders' Morning Fix Under Scrutiny: by Michael Mackenzie, Tom Braithwaite and Kara Scannell in New YorkRajat KaushikNo ratings yet

- 9dollar As Reserve Currency FT Mar13 2013Document8 pages9dollar As Reserve Currency FT Mar13 2013Rajat KaushikNo ratings yet

- 7final Guidelines On Securitisation of Standard Assets - Aug2012Document28 pages7final Guidelines On Securitisation of Standard Assets - Aug2012Rajat KaushikNo ratings yet

- 9NYSE Euronext To Take Over Tainted Libor - ET Dt. 10-07-13Document1 page9NYSE Euronext To Take Over Tainted Libor - ET Dt. 10-07-13Rajat KaushikNo ratings yet

- 5the Real Gold Man at Goldman Sachs He Called Gold Crash Right - ET Dt. 19-04-13Document2 pages5the Real Gold Man at Goldman Sachs He Called Gold Crash Right - ET Dt. 19-04-13Rajat KaushikNo ratings yet

- 5FMC Suspends Two Brokers For Guar Trade Irregularities - ET Dt. 24-01-12Document1 page5FMC Suspends Two Brokers For Guar Trade Irregularities - ET Dt. 24-01-12Rajat KaushikNo ratings yet

- 4IPOs Fail To Live Up To Their Price - ET Dt. 16-04-13Document3 pages4IPOs Fail To Live Up To Their Price - ET Dt. 16-04-13Rajat KaushikNo ratings yet

- 5sebi Has Completely Changed The Way Trading Takes Place in India - ET Dt. 22-05-2013Document2 pages5sebi Has Completely Changed The Way Trading Takes Place in India - ET Dt. 22-05-2013Rajat KaushikNo ratings yet

- 5indian Bond Market WP Nipfp 2012Document22 pages5indian Bond Market WP Nipfp 2012Rajat KaushikNo ratings yet

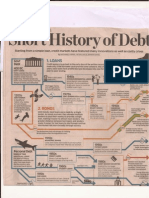

- 5history of Debt-2Document1 page5history of Debt-2Rajat KaushikNo ratings yet

- 5release of Data April2013 WSJDocument4 pages5release of Data April2013 WSJRajat KaushikNo ratings yet

- 5RIL Plans To Borrow $2 B To Refinance Debt - ET Dt. 06-04-13Document1 page5RIL Plans To Borrow $2 B To Refinance Debt - ET Dt. 06-04-13Rajat KaushikNo ratings yet

- 5history of Debt-1Document1 page5history of Debt-1Rajat KaushikNo ratings yet

- Debt Funds Are Not As "Safe" As They Sound.: Safety Is Not AssuredDocument5 pagesDebt Funds Are Not As "Safe" As They Sound.: Safety Is Not AssuredRajat KaushikNo ratings yet

- 5fiis and Mkts em Apr8 2013Document4 pages5fiis and Mkts em Apr8 2013Rajat KaushikNo ratings yet

- 4the Side Effects of The Cyprus Cure - ET Dt. 20-03-13Document2 pages4the Side Effects of The Cyprus Cure - ET Dt. 20-03-13Rajat KaushikNo ratings yet

- 5commodity Cycle-April 2013Document3 pages5commodity Cycle-April 2013Rajat KaushikNo ratings yet

- 3rupee Collapse An Unnecessary Scare - ET Dt. 12-04-13Document1 page3rupee Collapse An Unnecessary Scare - ET Dt. 12-04-13Rajat KaushikNo ratings yet

- 4partnership Enterprise - ET Dt. 05-03-2012Document4 pages4partnership Enterprise - ET Dt. 05-03-2012Rajat KaushikNo ratings yet

- 5BSE Becomes The Hub For SMEs - ET Dt. 16-04-13Document1 page5BSE Becomes The Hub For SMEs - ET Dt. 16-04-13Rajat KaushikNo ratings yet

- 4IPO MCX Overbid 54 Imes To Rs.35000 Cr. ET Dt. 25-02-2012Document2 pages4IPO MCX Overbid 54 Imes To Rs.35000 Cr. ET Dt. 25-02-2012Rajat KaushikNo ratings yet

- 2ready For The Swan Song - ET Dt. 01-05-13Document3 pages2ready For The Swan Song - ET Dt. 01-05-13Rajat KaushikNo ratings yet

- 2panel Moots 2 Financial Regulators - ET Dt.23!03!13Document1 page2panel Moots 2 Financial Regulators - ET Dt.23!03!13Rajat KaushikNo ratings yet

- 3mon Pol-State of Financial Sector Regulation and Competition in India-November 13-2011Document21 pages3mon Pol-State of Financial Sector Regulation and Competition in India-November 13-2011Rajat KaushikNo ratings yet

- 3india Lending Rate April2013 WSJDocument2 pages3india Lending Rate April2013 WSJRajat KaushikNo ratings yet

- 2will Hit 60 On Worsening Pitch - ET Dt. 12-04-13Document1 page2will Hit 60 On Worsening Pitch - ET Dt. 12-04-13Rajat KaushikNo ratings yet

- 2RBI Panel On Mon Pol-WSJ-Jan21-2014Document2 pages2RBI Panel On Mon Pol-WSJ-Jan21-2014Rajat KaushikNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Demonetisation Essay Download Demonetisation Essay PDF For UPSC PreparationDocument11 pagesDemonetisation Essay Download Demonetisation Essay PDF For UPSC PreparationRahul NimmagaddaNo ratings yet

- MFS PPT FinalDocument18 pagesMFS PPT FinalvijaybharvadNo ratings yet

- Exposure NormsDocument30 pagesExposure Normspadam_09No ratings yet

- Priority Sector Lending & Doubling Farmer's Income: C.C.S National Institute of Agricultural MarketingDocument33 pagesPriority Sector Lending & Doubling Farmer's Income: C.C.S National Institute of Agricultural MarketingPrathap G MNo ratings yet

- International Financial SystemDocument19 pagesInternational Financial Systemnavya782003No ratings yet

- Alternative Sources of Finance - Private and SocialDocument13 pagesAlternative Sources of Finance - Private and SocialSkanda KumarNo ratings yet

- Research Paper On Credit Appraisal in BanksDocument7 pagesResearch Paper On Credit Appraisal in Banksh02ngq6c100% (1)

- January 2022 Current Affairs File 2Document21 pagesJanuary 2022 Current Affairs File 2siddNo ratings yet

- Project On HDFC BankDocument32 pagesProject On HDFC BankJeevan Patel100% (1)

- Credit Recovery ManagementDocument75 pagesCredit Recovery ManagementSudeep Chinnabathini75% (4)

- Forward ContractsDocument31 pagesForward ContractsDeepthi Ravichandhran100% (1)

- Sip Report On Motilal Oswal Asset Management LTDDocument51 pagesSip Report On Motilal Oswal Asset Management LTDSudish SinghNo ratings yet

- CPSPM 66127250 1675446430Document36 pagesCPSPM 66127250 1675446430Vikas100% (2)

- Asset Quality & Risk Management Practices - An Analysis On Yes BankDocument10 pagesAsset Quality & Risk Management Practices - An Analysis On Yes BankParth Hemant PurandareNo ratings yet

- Narasimham Committee On Banking Sector ReformsDocument10 pagesNarasimham Committee On Banking Sector ReformsNilofer AneesNo ratings yet

- 7 Pratts JBankr L552Document30 pages7 Pratts JBankr L552VinayNo ratings yet

- 2000 Banking Awareness MCQsDocument193 pages2000 Banking Awareness MCQsSniper Souravsharma100% (1)

- Evolution of Monetary Policy in India Early PhaseDocument15 pagesEvolution of Monetary Policy in India Early PhaseNitesh kuraheNo ratings yet

- Causes For The Growth of Public Expenditure in IndiaDocument4 pagesCauses For The Growth of Public Expenditure in IndiaAbhi RamNo ratings yet

- Elysium Capital India Commentary 090609Document2 pagesElysium Capital India Commentary 090609oontiverosNo ratings yet

- Performance of Indian Banking SystemDocument21 pagesPerformance of Indian Banking SystemMukund TiwariNo ratings yet

- 75 RBI Grade B Interview Transcripts - Part 1 of 5 - Supriyo PandaDocument28 pages75 RBI Grade B Interview Transcripts - Part 1 of 5 - Supriyo PandaUnprecedented ScienceTVNo ratings yet

- RBI and Its FunctionDocument3 pagesRBI and Its Functionprahlad sharmaNo ratings yet

- Bank MCQSDocument27 pagesBank MCQSSanjeev SubediNo ratings yet

- Catholic Syrian BankDocument29 pagesCatholic Syrian BanksherwinmitraNo ratings yet

- SH-NBFC - Retail & Commercial Finance-Q2-1-April 2020 PDFDocument7 pagesSH-NBFC - Retail & Commercial Finance-Q2-1-April 2020 PDFDhrubajyoti DattaNo ratings yet

- India: Amarchand & Mangaldas & Suresh A. Shroff & CoDocument6 pagesIndia: Amarchand & Mangaldas & Suresh A. Shroff & CofaizlpuNo ratings yet

- JiboDocument33 pagesJibojyottsna67% (3)

- Rbi Fema PDFDocument22 pagesRbi Fema PDFPriyahemani100% (1)

- Training Project: A Study ofDocument45 pagesTraining Project: A Study ofAnkur Malhotra0% (1)