You might also like

- Economic Analysis of Indian Construction IndustryDocument23 pagesEconomic Analysis of Indian Construction Industryaishuroc100% (2)

- India Special Report - Assessing The Economic Impact of India's Real Estate Sector - CREDAI CBREDocument20 pagesIndia Special Report - Assessing The Economic Impact of India's Real Estate Sector - CREDAI CBRErealtywatch108No ratings yet

- Indian Construction Industry Report 2009-10: Overview, Macro Trends & Growth OutlookDocument52 pagesIndian Construction Industry Report 2009-10: Overview, Macro Trends & Growth OutlookAshish DesaiNo ratings yet

- "A Study On Fundamental Analysis of Indian Infrastructure IndustryDocument18 pages"A Study On Fundamental Analysis of Indian Infrastructure IndustrySaadgi AgarwalNo ratings yet

- Real Estate: (Industry Guide) By:-Aamir SaleemDocument18 pagesReal Estate: (Industry Guide) By:-Aamir SaleemAamir SaleemNo ratings yet

- Assessing India's Real Estate Sector's Economic Impact and Future GrowthDocument20 pagesAssessing India's Real Estate Sector's Economic Impact and Future GrowthChenna Vivek KumarNo ratings yet

- India Infrastructure InvestmentDocument5 pagesIndia Infrastructure Investmentneha_64No ratings yet

- Fdocuments - in Wipro Project FileDocument80 pagesFdocuments - in Wipro Project FilekavyaNo ratings yet

- IndianDocument5 pagesIndianambikaraniNo ratings yet

- China Import Forum 2013: Presentation On Indian IndustryDocument19 pagesChina Import Forum 2013: Presentation On Indian IndustryGourav Batheja classesNo ratings yet

- Question Paper Integrated Case Studies - II (352) : July 2006Document27 pagesQuestion Paper Integrated Case Studies - II (352) : July 2006Wise MoonNo ratings yet

- Session 12 Secondary SectorDocument9 pagesSession 12 Secondary Sectorkaushtubh_496909036No ratings yet

- The Role of Small Scale Industries in IndiaDocument23 pagesThe Role of Small Scale Industries in IndiaHemantSharmaNo ratings yet

- Aspects of Industrial Policy, Role of Small Sector Industry, Public Sector, Privatization Aspects, Infrastructure Economic DevelopmentDocument16 pagesAspects of Industrial Policy, Role of Small Sector Industry, Public Sector, Privatization Aspects, Infrastructure Economic DevelopmentNilesh MishraNo ratings yet

- Construction Sector Growth in IndiaDocument30 pagesConstruction Sector Growth in IndiaSUKHVINDER SINGH SAININo ratings yet

- United Institute of Management: "Future Prospects of Infrastructure"Document20 pagesUnited Institute of Management: "Future Prospects of Infrastructure"Amritesh MishraNo ratings yet

- 202003291623596416roli_mishra_Uttar_Pradesh_IndustryDocument15 pages202003291623596416roli_mishra_Uttar_Pradesh_IndustryAMIT JaiswalNo ratings yet

- Equity ValuationDocument18 pagesEquity ValuationAbhishek NagpalNo ratings yet

- Development With Special Emphasis On SEZ: Need, Performance and Government Strategy For InfrastructuralDocument5 pagesDevelopment With Special Emphasis On SEZ: Need, Performance and Government Strategy For InfrastructuralSimran SimieNo ratings yet

- Group4 IVM Project FinalDocument60 pagesGroup4 IVM Project FinalVaibhav GargNo ratings yet

- DLF Industry Analysis: Real Estate Giant Poised for GrowthDocument29 pagesDLF Industry Analysis: Real Estate Giant Poised for GrowthZeba BidikarNo ratings yet

- Research Proposal: A Study On Capital Productivity of Small & Medium Scale Industries in KarnatakaDocument6 pagesResearch Proposal: A Study On Capital Productivity of Small & Medium Scale Industries in Karnatakashashikiranl858050% (2)

- Dashboard For SajidsfaDocument7 pagesDashboard For SajidsfasajidsfaNo ratings yet

- On Indian Economy Features and DevelopmentDocument36 pagesOn Indian Economy Features and DevelopmentSaima Arshad67% (9)

- Economic Infrastructure & Key Indicator of Economic PerspectiveDocument13 pagesEconomic Infrastructure & Key Indicator of Economic PerspectiveSagar ShetkarNo ratings yet

- An Organizational Study (Project File)Document87 pagesAn Organizational Study (Project File)y_harshNo ratings yet

- Fundamental AnalysisDocument21 pagesFundamental AnalysisSanjeet Singh0% (1)

- Indian Cement Industry ReportDocument92 pagesIndian Cement Industry ReportShone ThattilNo ratings yet

- Executive Summary: Cement IndustryDocument92 pagesExecutive Summary: Cement Industrypratap_sivasaiNo ratings yet

- Indian Cement Industry ReportDocument92 pagesIndian Cement Industry ReportShone ThattilNo ratings yet

- Indian Construction IndustryDocument5 pagesIndian Construction IndustryValerie PittmanNo ratings yet

- Executive Summary: Cement IndustryDocument81 pagesExecutive Summary: Cement IndustrySankaraharan ShanmugamNo ratings yet

- Assignment On Business Communication and Managerial Skill DevelopmentDocument8 pagesAssignment On Business Communication and Managerial Skill DevelopmentSatyapriya PangiNo ratings yet

- SWOT AnalysisDocument38 pagesSWOT Analysissukhi9291100% (1)

- India Industry Business Environment ProjectDocument41 pagesIndia Industry Business Environment Projectpramit_chhetriNo ratings yet

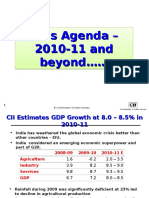

- CII's AgendaDocument31 pagesCII's AgendaPremkumarJittaNo ratings yet

- Executive Summary: Cement IndustryDocument97 pagesExecutive Summary: Cement Industryst miraNo ratings yet

- India's cement industry outpaces China's growthDocument92 pagesIndia's cement industry outpaces China's growthAbdulgafoor NellogiNo ratings yet

- GDP Growth by Sector Over Five Year PlansDocument23 pagesGDP Growth by Sector Over Five Year PlansRahul KadamNo ratings yet

- Promotion of Small Scale IndustriesDocument13 pagesPromotion of Small Scale IndustriesChandan KumarNo ratings yet

- KSFC Lending Policy 2013-14Document57 pagesKSFC Lending Policy 2013-14ajayterdalNo ratings yet

- Beml CompanyDocument21 pagesBeml CompanyArun NijaguliNo ratings yet

- MSMEs in IndiaDocument4 pagesMSMEs in IndiaManisana LuwangNo ratings yet

- Small Scale IndustriesDocument28 pagesSmall Scale IndustriesMohit Gupta25% (4)

- Priyanka H MCP FINAL..........Document129 pagesPriyanka H MCP FINAL..........Shrivatsa JoshiNo ratings yet

- Retail Industry AnalysisDocument33 pagesRetail Industry Analysisshantanu_malviya_1No ratings yet

- Risk Analysis of Infrastructure Projects PDFDocument27 pagesRisk Analysis of Infrastructure Projects PDFMayank K JainNo ratings yet

- Risk Assessment in Bop ProjectsDocument22 pagesRisk Assessment in Bop ProjectsHarishNo ratings yet

- KUWAIT India New OpportunitiesDocument21 pagesKUWAIT India New OpportunitiesRicha DhanukaNo ratings yet

- Indian Manufacturing Technology ReportDocument47 pagesIndian Manufacturing Technology ReportJust_Jobless100% (1)

- Impact of Global Financial Crisis On FDI Flows in India - A Special Reference To Housing SectorDocument7 pagesImpact of Global Financial Crisis On FDI Flows in India - A Special Reference To Housing SectorJignesh ThakarNo ratings yet

- Welfare Measures ProjectDocument84 pagesWelfare Measures ProjectMathivanan AnbazhaganNo ratings yet

- Tajikistan: Promoting Export Diversification and GrowthFrom EverandTajikistan: Promoting Export Diversification and GrowthNo ratings yet

- Policies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportFrom EverandPolicies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportNo ratings yet

- Provincial Facilitation for Investment and Trade Index: Measuring Economic Governance for Business Development in the Lao People’s Democratic Republic-Second EditionFrom EverandProvincial Facilitation for Investment and Trade Index: Measuring Economic Governance for Business Development in the Lao People’s Democratic Republic-Second EditionNo ratings yet

- Estimating the Job Creation Impact of Development AssistanceFrom EverandEstimating the Job Creation Impact of Development AssistanceNo ratings yet

- Construction CompanyDocument111 pagesConstruction CompanyJames Warren0% (1)

- By Own Website 5 17 by Commercial Website 9 30 Not Advertising Through Internet 16 53Document2 pagesBy Own Website 5 17 by Commercial Website 9 30 Not Advertising Through Internet 16 53Dimitry VegasNo ratings yet

- Inrev DD Questionnaire Fof MM 201205Document40 pagesInrev DD Questionnaire Fof MM 201205Dimitry VegasNo ratings yet

- Summer Project Report on "A Study on Customer Satisfaction in XYZ BankDocument8 pagesSummer Project Report on "A Study on Customer Satisfaction in XYZ BankDimitry VegasNo ratings yet

- Project Report On Industrial Visit To Amul: Submitted By, ARUNA LAMBHA (Roll No.45)Document18 pagesProject Report On Industrial Visit To Amul: Submitted By, ARUNA LAMBHA (Roll No.45)Dimitry VegasNo ratings yet

- Reading Preference MbaDocument13 pagesReading Preference MbaDimitry VegasNo ratings yet

- ABC Analysis YKDocument6 pagesABC Analysis YKvamsibuNo ratings yet