Professional Documents

Culture Documents

Annual Report 2013

Uploaded by

Wafi StalinofskivitchdavitovichskyCopyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Annual Report 2013

Uploaded by

Wafi StalinofskivitchdavitovichskyCopyright:

Available Formats

ANNUAL REPORT 2013

C O N T E N T S

4 Vision

6 Transmittal Letter

7 Notice of the 24th Annual General Meeting

8 Corporate Directory

9 Company at a Glance

10 Products and Services

13

The Pattern of Shareholding by the

Directors & Executives

14 Range of Shareholding

15 Last fve Years Financial Summary

16 Board of Directors

17 List of Senior Management

18 Chairmans Message

22 Managing Director and CEOs Message

26 Directors Report

42 Corporate Governance

45 Report of the Audit Committee

46 Picture Gallery

52 Auditors Report and Financial Statements

58 Notes to the Financial Statements

90 Notes

91 Proxy Form

VISION

Recognizing the fundamental need for efective systems

integration is what distinguishes the companies of aamra.

Our vision is to empower companies and individuals to

access personalized solutions, products and services when,

where and how they may choose. We integrate all elements

of a system, new and existing, into a single solution that

addresses strategic growth, outstanding service, and

community involvement.

4

aamra technologies limited I ANNUAL REPORT 2013

5

Performance is our passion

The motivation that drives us in all business area emerges delivering higher performance

products and services to our customers. Combining technological, economic and personal

aspects of performance make the diference at aamra.

Creating value with

aamra recognizes the power that partnership and cooperation have in achieving any goal.

We believe that by harnessing the strength of togetherness with all our stakeholders,

we will be able to surmount any obstacle in our path and scale new height. Accordingly

our products and services are meant to create value of unity in relations to our business

partners, shareholders as well as to our employees and society in general.

hhhh

that partnership and cooperatio

6

aamra technologies limited I ANNUAL REPORT 2013

Date: November 26, 2013

To

The shareholders,

Bangladesh Securities and Exchange Commission,

Registrar of Joint Stock Companies & Firms,

Dhaka Stock Exchange Limited

Chittagong Stock Exchange Limited

Sub: Annual Report for the year ended June 30, 2013

Dear Sir:

We are pleased to enclose a copy of the Annual Report together with the Audited Financial Statements for

the year ended June 30, 2013 for your record/necessary action.

Sincerely Yours

Md. Anamul Haque

Company Secretary

TRNSMITAL

LETER

7

NOTICE OF THE 24

th

ANNUAL GENERL MEETING

Notice is hereby given that the 24

th

Annual General Meeting of aamra technologies limited will be held

at Bashundhara Convention Center 2, Bashundhara, Dhaka, on Sunday, December 22, 2013 at 10:00 a.m.

to transact the following business:

1. To receive, consider and adopt the Audited Financial Statements of the Company for the year ended

June 30, 2013 together with the Reports of the Directors and Auditors thereon.

2. To declare dividend for the year ended June 30, 2013.

3. To elect Directors of the Company as per its Articles of Association.

4. To appoint Auditors for the Financial Year 2014 and fx their renumeration.

5. To transact any other business with the permission of the Chair.

By order of the Board

Md. Anamul Haque

Company Secretary

Dated: November 24, 2013

Notes:

1. November 7, 2013 is scheduled as Record Date. Shareholders whose names will appear on the Register

of Members or in the Depository Register on the Record Date will be eligible to attend the meeting and

qualify for dividend.

2. A member entitled to attend and vote at the general meeting is also entitled to appoint a proxy to

attend the meeting and vote on his/her behalf. The proxy form duly completed, must be af xed with a

revenue stamp of Tk. 10/- and deposited at the registered of ce no later than 48 hours before the time

of holding the meeting.

3. Admission into the meeting room will be allowed upon presenting the attendance slip duly signed by

the member/proxy/attorney/representative, as the case may be.

4. Annual Report 2013 is available in the Company Website.

5. No gift or beneft in cash or kind shall be paid to the holder of equity securities at the AGM as

per Bangladesh Securities and Exchange Commission notifcation No. SEC/SRMI/2000-953/1950

dates 24

th

October 2000 (c).

8

aamra technologies limited I ANNUAL REPORT 2013

CORPORTE

DIRECTORY

Registered Of ce

BTA Tower (10

th

Floor),

29 Kemal Ataturk Avenue

Banani C/A, Dhaka-1213

Business Address

F.R Tower (9

th

Floor),

32 Kemal Ataturk Avenue

Banani C/A, Dhaka-1213

Chittagong Of ce

SSFA Estate

132 Panchlaish R/A

Chittagong

Auditors

Masih Muhith Haque & Co.

Chartered Accountants

Level # 13, UTC Building

8 Panthopoth

Dhaka-1215

Legal Adviser

Syed Ishtiaq Ahmed & Associates

Concord Ovilash (1

st

Floor)

House 62, Road 11A

Dhanmondi, Dhaka-1205

Bankers

Bank Asia Ltd

ONE Bank Ltd

The City Bank Ltd

Dutch Bangla Bank Ltd

Dhaka Bank Ltd

Insurer

Green Delta Insurance Co. Ltd

9

COMPANY

AT A GLANCE

Company Name : aamra technologies limited

Registered Of ce :

BTA Tower (10

th

Floor)

29 Kemal Ataturk Avenue, Banani C/A,

Dhaka-1213

Business Address :

F.R Tower (9

th

Floor), 32 Kemal Ataturk

Avenue Banani C/A, Dhaka-1213

Date of Incorporation : On March 14, 1990

Date of Commercial Operation : On March 14, 1990

Legal Status : Public Limited Company

Authorized Share Capital : BDT 1000 million

Paid-Up Share Capital : BDT 503 million

Number of Shareholder : 16,568 (as on 7 November, 2013)

Line of Business :

ATL provides high-tech and customized

solutions to address a broad range of IT

Business needs. As a complete service

solutions company, we address all aspects

of a product/project development life

cycle, ranging from preliminary analysis and

design to programming, hardware and soft

ware specifcation, project implementation,

and training. Our team members have

extensive experience in the Financial

Industry, Manufacturing, and Internet based

application services.

Number of Employee : 109 (One Hundred & Nine)

10

aamra technologies limited I ANNUAL REPORT 2013

PRODUCTS AND SERVICES

We are the authorized distributor of the world renowned brands that cater to the Financial Services Industry,

Telecommunications Industry, Network Equipment Provider, Internet Service Provider, Independent Software

Vendor and Small & Medium Business in Bangladesh. Not only we sell the products but also provide services

and our Product & Service Portfolio is given below:

Brand Products Company Origin

Oracle

Servers, Soft ware &

Storage Solution

Oracle Corporation U.S.A

VeriFone

POS Terminals & NAC VeriFone U.S.A

Finacle

Core Banking Solution Infosys Technologies Ltd. India

NBS

Card Personalization

Solutions

NBS Technologies Inc. U.S.A

Thales Host Security Module Thales E-Security Inc. U.S.A

Cisco Network Product Cisco Systems Inc. U.S.A

Juniper

Network Product Juniper Networks U.S.A

Microsoft

Software Microsoft Corporation U.S.A

CA

Network Management

Software

CA Technologies Ltd. U.S.A

11

Some of our Clients

(by Products)

Diebold:

Bank Asia Limited

BRAC Bank Limited

Cynergon IntelliSys Limited

Commercial Bank of Ceylon

Dutch Bangla Bank Limited

Electronic Transactions Network (ETN) Limited

Islami Bank Bangladesh Limited

Mutual Trust Bank Limited

Networld BD Limited

Premier Bank Limited

Prime Bank Limited

Southeast Bank Limited

The City Bank Limited

Oracle-Sun Systems:

Telecommunications Industry:

Axiata Limited (Robi)

Getco Communication

Grameenphone Limited

MIR Telecom

MnH Telecom

National Telecom

Pacifc Bangladesh Telecom Limited (Citycell)

Banglalink Telecom Ventures Limited

(Previously Orascom Telecom Ventures Limited)

S A Telecommunication System Limited

Warid Telecom (Pvt.) Limited

Network Equipment Provider (NEP):

Alcatel-Lucent

Ericsson AB

HUAWEI

Motorola Inc,

Nokia Siemens Networks (NSN)

Independent Software Vendor (ISV):

Comviva

Fundamo

Interblocks

Roamware

Sysbase 365

Ushacomm

Financial Service Industry (FSI):

Bank Alfalah Limited

Bank Asia Limited

BRAC Bank Limited

Dhaka Bank Limited

Dutch Bangla Bank Limited

Islami Bank Bangladesh Limited

National Bank Limited

Southeast Bank Limited

Standard Chartered Bank

The City Bank Limited

United Commercial Bank Limited

Internet Service Provider (ISP):

aamra Networks Limited

BRAC BD Mail Network Limited

Delta Soft Limited

Delta Network

Dominox Technologies Limited

Global Access Limited

Grameen Cyber Net Limited

Grameen IT Park Limited

System Limited

Education Industry:

Independent University of Bangladesh

North South University

Other Industries:

Alliance TG-Supply

Army Head Quarter

Bangladesh Bureau of Statistics

Bangladesh Petroleum Institute

Bangladesh Space Research and Remote

Sensing Organization (SPARRSO)

Berger Paints Bangladesh Limited

OTOBI Limited

Proshika Computer System

SAARC Meteorological Research Centre

Shakti Foundation

Shell Bangladesh Exploration and

Development B.V.

Network Solution (Cisco, Juniper, CA):

AB Bank Limited

Axiata Limited (Robi)

BELST (Alap Communication Limited)

Berger Paints Bangladesh Limited

Citi Bank N.A

Grameenphone Limited

LankaBangla Securities Limited

National Bank Limited

Otto International Limited

Banglalink Telecom Ventures Limited

(Previously Orascom Telecom Ventures Limited)

Pacifc Bangladesh Telecom Limited (Citycell)

Prime Bank Limited

Reckitt Benckiser

Roamware

Shahjalal Islami Bank Limited

Southeast Bank Limited

Transparency International Bangladesh (TIB)

UNDP Bangladesh

Unilever Bangladesh

12

aamra technologies limited I ANNUAL REPORT 2013

Finacle Core Banking Solution:

BRAC Bank Limited

The City Bank Limited

Interblocks Switching Solution:

Islami Bank Bangladesh Limited

United Commercial Bank Limited

Remittance Solution:

BRAC Bank Limited (EL Dorado)

Payment Gateway Solution:

BRAC Bank Limited (iPay and iMobile Solution)

Credit Card Management System:

Dhaka Bank Limited

Islami Bank Bangladesh Limited

Hypercom Point of Sale (POS):

American Express Bank

BRAC Bank Limited

Dutch Bangla Bank Limited

EXIM Bank Limited

Islami Bank Bangladesh Limited

LankaBangla Finance Limited

Mutual Trust Bank Limited

National Bank Limited

Premier Bank Limited

Prime Bank Limited

The City Bank Limited

Network Access Control (NAC):

American Express Bank Limited

Bank Alfalah Limited

BRAC Bank Limited

Dutch Bangla Bank Limited

ITCL

LankaBangla Finance Limited

National Bank Limited

Premier Bank Limited

Prime Bank Limited

Thales:

Bank Alfalah Limited

BRAC Bank Limited

Electronic Transactions Network

Islami Bank Bangladesh Limited

LankaBangla Finance Limited

Mutual Trust Bank Limited

Premier Bank Limited

Prime Bank Limited

Standard Chartered Bank Limited

The City Bank Limited

United Commercial Bank Limited

NBS:

BRAC Bank Limited

Dhaka Bank Limited

Dutch Bangla Bank Limited

Electronic Transactions Network

IFIC Bank Limited.

Islami Bank Bangladesh Limited

LankaBangla Finance Limited

Mutual Trust Bank Limited

Southeast Bank Limited

The City Bank Limited

United Commercial Bank Limited

Oracle (Software):

Islami Bank Bangladesh Limited

National Bank Limited

Novotel Limited

Banglalink Telecom Ventures Limited

(Previously Orascom Telecom Ventures Limited)

The City Bank Limited

Microsoft:

A.B.S. Safdar & Co. Limited

Harpoon Securities Limited

SGS Bangladesh Limited

IIG:

Accesstel

Aftab IT Limited

Angel Drops Limited

Bangla Phone Limited

Bangladesh Internet Exchange Ltd

Chittagong Online Limited

CTG TEL

GramBangla Systems Limited

IDS Bangladesh

Information Services Network Limited

New Generation Graphics Ltd

Radiant Communication Ltd

Royal Green Online Limited

Sadiatec Limited

Spark Systems Limited

Teletalk Bangladesh Limited

ZxOnline Limited

aamra Networks Limited

13

THE PATERN OF SHARE HOLDING BY

THE DIRECTORS & EXECUTIVES

Sl No Shareholding Pattern

Number of shares held

as on 30.06.2013

i) Directors

1 Syed Faruque Ahmed 4,646,074

2 Syed Farhad Ahmed 4,646,074

3 Syeda Amina Ahmed 2,788,780

4 Syeda Farida Ahmed 1,008,201

5 Syeda Munia Ahmed 1,008,201

6 Fahmida Ahmed 1,008,201

7 K.M. Hasan (Independent Director) Nil

ii) Shareholding of Executives Nil

iii) Shareholders who are holding 10% or above shares: Nil

14

aamra technologies limited I ANNUAL REPORT 2013

RNGE OF

SHAREHOLDING

Summary of Shareholders

The distribution schedule of shareholding of aamra technologies limited as on 7

th

November, 2013 was as

presented below.

On the Basis of Share Holders Type:

Group Name No. of Shareholders No. of Shares Ownership (%)

All Investors A/C 4 571,200 1.135%

Company 91 4,870,773 9.677%

General Public 16,064 29,578,960 58.763%

NRB [Non-Resident Bangladeshi] 403 209,350 0.416%

Sponsor/Director 6 15,105,531 30.010%

Total: 16,568 50,335,814 100%

On the Basis of Share Holding:

Share Holding Range No. of Shareholders No. of Shares Ownership (%)

0000000001-0000000499 9,847 2,351,697 4.672%

0000000500-0000005000 5,599 9,346,926 18.569%

0000005001-0000010000 576 4,426,510 8.794%

0000010001-0000020000 321 4,655,500 9.249%

0000020001-0000030000 91 2,311,500 4.592%

0000030001-0000040000 49 1,751,500 3.480%

0000040001-0000050000 17 795,300 1.580%

0000050001-0000100000 37 2,727,750 5.419%

0000100001-0001000000 24 5,820,350 11.563%

0001000001-1000000000 7 16,148,781 32.082%

Total: 16,568 50,335,814 100%

15

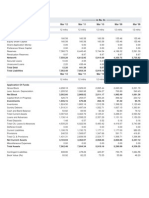

Particulars 2013 2012 2011 2010 2009

Revenue (BDT) 717,863,483 668,400,734 512,566,960 690,846,042 643,449,490

Gross Proft (BDT) 184,010,024 145,205,125 108,819,947 96,570,216 64,809,048

Net Proft Before Tax (BDT) 86,294,991 70,825,211 58,577,479 57,859,325 36,079,790

Net Proft After Tax (BDT) 73,593,961 58,854,779 48,622,772 48,432,759 25,484,808

Total Assets (BDT) 1,634,199,221 2,176,995,594 1,162,131,213 1,018,242,722 652,980,023

Capital & Reserve (BDT) 1,102,557,653 1,028,963,691 487,042,182 461,254,190 128,376,998

No. of Shares 50,335,814 41,946,512 18,522,284 18,522,284 4,779,402

Face Value (BDT) 10 10 10 10 10

EPS (BDT) 1.46 2.46 2.39 2.61 5.33

LAST FIVE YEARS

FINANCIAL SUMMARY

Revenue

Millions

2009 2010 2011 2012 2013

643.45

690.85

512.50

668.40

717.86

Gross Profit

Millions

2009 2010 2011 2012 2013

64.81

96.57

108.80

145.20

184.01

Net Profit after Tax

Millions

2009 2010 2011 2012 2013

25.48

48.43

48.64

58.85

73.59

Five Years at a Glance

Millions

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

2009 2010 2011 2012 2013

Revenue Gross Proft

Net Proft before Tax Net Proft after Tax

16

aamra technologies limited I ANNUAL REPORT 2013

Syed Faruque Ahmed

Chairman

K.M. Hasan, FCA

Independent Director

Md. Anamul Haque

Company Secretary

Syed Farhad Ahmed

Managing Director & CEO

Syeda Munia Ahmed

Director

Fahmida Ahmed

Director

BOARD OF

DIRECTORS

17

LIST OF SENIOR

MANAGEMENT

Name of Employees Designation Wing

Sharful Alam Chief Operating Of cer Administration

Zahrul Syed Bakht Group Chief Financial Of cer Finance & Accounts

Md. Mosiur Rahman General Manager Operation

Md. Anamul Haque Company Secretary Finance & Accounts

Md. Mostofa Kamal Chowdhury Assistant General Manager Services

Serajul Alam Khan Assistant General Manager Sun Sales

Md. Mohiuddin Khan Senior Manager, Credit Recovery Finance & Accounts

Kazi Roman Ahmed Senior Manager Sales

Mashih-ul-Huq Manager Enterprise Solutions

Shariful Islam Manager Finance & Accounts

Sougata Karmakar Manager Financial Service Industries

Md. Alamgir Hossain Manager Oracle Sales

Abdullah Al Hossain Manager RnD & Pre-Sales

Mohammed Ziaul Hoque Zilani Manager RnD & Pre-Sales

Md. Monsur Rahman Chowdhury Deputy Manager Diebold Service

Rajib Uddin Khan Deputy Manager Diebold Service

Abu Hena Mostafa Kamal Deputy Manager Administration & Commercial

T.M. Abdullah-Al-Amin Deputy Manager Oracle Sun Service

Utpal Basak Deputy Manager Oracle Sales

Nazim Chowdhury Deputy Manager Share

Syed Akmal Hossain Assistant Manager Administration & Logistics

Waf Aziz Sattar Assistant Manager Communication

Md. Abdul Wahed Assistant Manager Enterprise Solutions

Md. Ashikur Rahman Assistant Manager FSI Sales

A.S.M. Nasher Assistant Manager POS Service

18

aamra technologies limited I ANNUAL REPORT 2013

As-salmu `alaykum

The projected rate for global growth estimate is

that it will stay passive at a little over 3% in 2013.

This is mostly due to the considerably frailer

domestic demand in a number of key emerging

market economies and the tenacious recession in

the euro area.

T

he economy of Bangladesh has had the misfortune of experiencing a

fuctuating economy in FY 2013 with the economy heading towards a

descending equipoise in the course of the ongoing fscal year. While

macroeconomic stability and rising infationary trends have been

CHAIRMANS

MESSAGE

19

somewhat balanced, for a second consecutive

year the economic growth has slowed down.

Events such as the Shahbag Movement, the

extremely tragic and unfortunate Savar Tragedy,

and the ongoing political rifts and tension have a

lot to do with this as well.

Despite all this, aamra technologies limited (ATL),

a trusted IT solutions provider to various sectors

of the economy, especially the fnancial sector for

over two decades, not only saw the expansion of

business, but witnessed the value propositions

for our clients grow stronger. During this time

of Bangladesh rebuilding, ATLs performance

for the FY 2013 remained sound and resilient, a

noteworthy achievement given the continuing

market turbulence.

As an established corporate all-rounder, ATL

implements the best practices in technology

and organizational transformation, process

design and re-engineering, human resource

management, strategic and business planning,

supply chain management, globalization

strategy, customer relationship management and

corporate governance. ATLs vision and striving

towards being rated as a top company which sets

the benchmark to be rivalled in this segment is

slowly coming to fruition for the best processes

and practices it has continuously shown over the

years.

2014 will be a time of great change with the

national election coming up. As such, there will

be many new obstacles and challenges that

Bangladesh will have to face. While the future

maybe unpredictable, ATL is prepared to aptly

tackle any uncertain situations, whether economic

or regulatory, as the organizations structure has

been formed to draw on deep capacity to adapt

and readjust as necessary to reallocate resources

rapidly. As like every year since our inception, ATL

is even better prepared than ever before to face

such challenges and capitalize on new market

opportunities.

Not only is ATL striving to enhance the fortunes of

ATL stakeholders and end users, but also putting

its absolute efort to make the company a better

place for both the employees at work and its

customers to ensure everyone associated with

ATL reaps rich dividends.

As always, I wish the very best for all of our

stakeholders and hope for continued Blessings

of The Almighty so we could meet and exceed

the ambitious targets and programs set by the

company for the upcoming years.

Syed Faruque Ahmed

Chairman

20

aamra technologies limited I ANNUAL REPORT 2013

|<|<

<||

||| ||+,

|<<|| <|< -|< -:: | +<| : |< |+

<| |+< < <|<| +<| - =< +|< - <|

<| -|| <||< || <<| ||--| =<

<| +< <|- -|...

<|

|-< ||< -|+ |-+ - -:: <<<

--| |<|| =< <| <<< || ||<

|-+ < - =+|-+ ||+ |+ ||||

=< <<| -|||< | <|- |+| |<| |+

|| << |+ <| <| -| |-<| |-|,

-t+ -|+ ||< ||< | |<| =< | <||+

21

| <|<| =< +|<< | -

=-, ||< |<| | |<<

|+ | - -+< <| << ||

<<<|-+|<| |-< |<| +||

||" << <<| |< -|| <<

|-+-< |< |<| < |+| |

+< | <||-< = <

-:: << |^|< +| | |||

||| | |<-| ||| <||< =+|

| |

=+| ||^ +|< <||< |-<

|<| +|| ||< | =<

||+ <|<, ||, =< |

+, |<- <<||, +

<<||+ |<+r|, || |,

|<|< +, |-+-+ <<|| =<

+|< |< ||-< |^| <|

<| |- <<< < << << <|

+| ++|< <|- << |<

|||-< | |-< <|

||- +< |< +||| -<|< | |

-<|<

-:- | || |<| ^|< |

<||- <|+ |<< < = <|

<||-+ + | |

+|<| +< -< = |<< <||

+<| | |<| +|| ||

|+ <| |+ +| ||+

|<|| |+|<| +< ||<

+|< -< - |<|< |

|< +<|< |< ||< < =

|^|< +||| | ||-< |^|<

<< + | <<< | = <<< |

|+|<| =< <||<< |-

|<<| | +<|< |< | |<|

|||<

|<| +|| ||-=< +-||<

=< <<-|<+|<|-< |-|<<| <|<

||-< |^| << << |<|

+|| ||-=< | | +

+|<| =< |-+-< +| = |^|+

< + |< +< <|+ |

||, |^|< | | +

|< |-|< - |<

|| |< |, ||-< + +-||<<

<| +|| +<| =< <|| ||-

|||< <|- <- || +<|,

|<| | <<| +|||++ -|

|||| || +|< <|<| ||$

||<

- |<+ |--

|<|

22

aamra technologies limited I ANNUAL REPORT 2013

Together with our customers we have

continued to demonstrate thought

leadership and have established ourselves as

a trusted partner to defne their agenda for

transformation of their business processes. For

over the past two decades, aamra technologies

limited has been fostering the profciency...

W

e are delighted to announce that the FY 2012-2013 was yet another

outstanding year for aamra technologies limited (ATL). Together

with our customers we have continued to demonstrate thought

leadership and have established ourselves as a trusted partner to

defne their agenda for transformation of their business processes. For over the

MANAGING DIRECTOR &

CEOS MESSAGE

23

past two decades, aamra technologies limited

has been fostering the profciency, expertise and

acumen to become a strong, efective and trusted

partner to our customers in the FSI, Telco and

other industries. Our continuing investments in

enriching and synergizing our wide portfolios of

services have created strong value propositions

for our clients, who are now leveraging our skill

sets to drive their own transformation programs.

As we have witnessed a tremendous growth in

consulting, engineering services and package

implementation of projects, services such as

infrastructure management, business process

management and managed services are now set

to grow steadily in the years to come.

You will be pleased to know that the IIG project of

the company is doing excellently and generating

good revenue for us. The IIG license has generated

proftable business opportunity for the company

which will have a great impact on the revenue of

the Company for years to come. Team leadership

of the highest standards is always the major pillar

to our success, and it is amongst our highest

priorities to ensure its continuity. Amongst the

aamra team leaders, we have a wealth of talent,

vision and far-sight, which enable us to ensure a

long-term succession plan and allow us to plan for

our next stage of growth.

With sincere gratitude and very best wishes to all

of our investors, team members,customers and

stakeholders, we look forward to your continuous

support and prayers for aamra technologies

limited (ATL), into the future.

Syed Farhad Ahmed

Managing Director & CEO

24

aamra technologies limited I ANNUAL REPORT 2013

||-< |-+-< | | |<| |<|<| |-+

<| =< | -< |< |-< <<||+

+|< <|< <|<, |-< +| <|<| |<

<|+ |-< |-<+ ||^ +< <|...

|

<| |-< | |<| +<| , -:---::

<< | |<| +|| ||-=< =+|

| << ||-< |-+-< | | |<|

|<|<| |-+ <| =< | -< |<

|-< <<||+ +|< <|< <|<, |-< +| <|<| |< <|+

<<|| |<|+

|'< <||

25

|-< |-<+ ||^ +< <|

- -+ << ==|, +| =< |

|r ||-< |-+-< +| |||, +|+<

|< <|+ |-< |<| +||

|| -| |<|| <| -| +<

| <|+ <|< ||-< <|-

|<||< ||-< |-+-< < =

<|< ||-< +|||< <||< <|

<|<| | - |<| = |-< <|<

+| ||-< +-|< < |<|

- $ <| <|, |+ <| =<

+r-< |+ <|<| =< <+|||

<<||, <<|| || <<|| =< <|

<<||< | <| | <|<| |||

<<| |||| <| |<

||<| | -< , ||-< |||

+r -|<|< |<|| - =< =< |<

+||| || <| +< -

||| |* <<|< |

<| +< |< |< ||| <<|

+|||< <<|< <| <|+ |<

< | < <| ||<

- < |-< +| +<

=< =| |<| <|+ <|<|<||-+|< ||+

+<|< | +|< ||-< | ||<-< |

|<|< < < |< ||, <<||+

-<-| =< < ||--| |+ +<|< |

|< |< |<| -||-| |< <<|

||+ +< ||< =< =| ||-<

|< <<| <| =| -|||

+<

||-< + |<||+|<|, | ||<, '||

|-+ =< |<-||<-< ||<+ +|

=< <| -|< |< |<| ||-<

| =< |<| +|| ||-

=< |<< |< -|| +|| +<|

- <-|- |--

<<|| |<|+ |

26

aamra technologies limited I ANNUAL REPORT 2013

Dear Shareholders,

As-salmu `alaykum

On behalf of the Board of Directors of aamra technologies limited (ATL), I take this opportunity to welcome

you to the 24

th

Annual General Meeting of the company and take the privilege of presenting the Annual

Report along with the Audited Financial Statements for the year ended June 30, 2013.

Global Economy

As like in 2012, the projected rate for the global growth is estimated to stay subdued at a little over 3%

in 2013 mostly due to app substantially feebler domestic demand and slow growth in a number of key

emerging market economies as well as a lingering recession in the euro area.

Downside risks to global growth prospects still dominate. While old risks remain, new risks have emerged,

including the possibility of a slowing growth, slowing credit, and possibly tighter fnancial conditions if

the anticipated unwinding of monetary policy stimulus in the United States leads to sustained capital fow

reversals. Additional policy action is required for stronger global growth.

The one way to counter this would be for the advanced economic states to maintain a supportive

macroeconomic policy mix in conjunction with credible plans in order to achieve some sustainability and

reforms to restore ledgers and credit channels. This is required primarily due to the fact that a good number

of emerging markets and developing economies are facing a trade-of between macroeconomic policies

to support weak activity and those to contain capital outfows. Macroprudential and structural reforms can

also help lessen the harshness of this trade-of.

Financial market volatility has increased globally in May and June after a period of calm since last summer.

Financial market instability and long-term interest have also risen in advanced economies. Peripheral euro

area sovereign spreads have widened again after a period of sustained declines. However, the emerging

market economies have taken the hardest hit as they have had decline in equity price, rising local yields,

currency depreciation and some capital outfows due to weaker domestic activity, interest rates and price

volatility in advanced economies.

Global growth has increased very slightly from an annualized rate of 2.5% in the second half of 2012 to only

2.75% in the frst quarter of 2013 (ref. Figure 1). This under performance was due to 3 vital factors:

1. Less growth in emerging markets:

Capacity restrictions

Slow external growth demand

Logjams in infrastructural development

Lower commodity prices

DIRECTORS

REPORT

27

Concerns over fnancial stability

Weaker policy support

2. Profound recession in the euro area:

Weak balance sheets

Afected growth

Impacted tight fscal and fnancial conditions

Low demand

3. Slow expansion of the U.S. economy:

Due to stronger fscal contraction weighed on improving private demand.

In stark contrast to all this, Japan had a robust growth primarily driven by net exports and consumption and

later by the 20% depreciation of the Yen since 2012.

In terms of forecasts, the growth in United States

is estimated to rise by only 1% from 1.75% to

2.75% in 2014, assuming the sequestration will

stay in place until 2014, despite the pace of fscal

consolidation being still slow.

Growth in Japan will average to about 2% in

2013, largely due to the positive efects of recent

accommodative policies, confdence and private

demand, thus nullifying the previously projected

growth. However, owing to the somewhat softer

forecast for 2014 due to the weaker global

environment, the growth is moderated to about

1.25% in 2014 for the region.

Recession will remain prevalent for the euro area

in the remainder of 2013 with activity contracting by over 0.5%. Due to persistent efects of the constraints

and expected delays in policy implementation in key areas and also due to base efect from the delayed

recovery in 2013, growth will only rise by under 1% in 2014, which is weaker than was previously projected

for the region.

At 5% in 2013 and about 5.5% in 2014, growth in the emerging market and developing economies is now

expected to evolve at a more upbeat pace, approximately 0.25% slower than it was in April 2013 (according

to IMFs World Economic Outlook), thus representing the weaker prospects across all regions.

In terms of forecasts, the growth in United States is estimated

to rise by only 1% from 1.75% to 2.75% in 2014, assuming the

sequestration will stay in place until 2014...

8

7

6

5

4

3

2

1

0

-1

-2

13:

Q4

2011 12

Advanced economies

World

Emerging market and

developing economies

Figure 1. Global GDP Growth

(Percent; quaeter over quarter, annualized

28

aamra technologies limited I ANNUAL REPORT 2013

Growth in China will average 7.75% in 2013/2014, 0.25% lower in 2013 and 0.5% lower in 2014, contrary

to the forecast originally made in April 2013. Forecast for the remaining BRICS have been revised down by

0.25% to 0.75% as well. The outlook has also deteriorated to lower commodity prices for many commodity

exporters, including those among BRICS.

In Sub-Saharan Africa, growth will be weaker due to Nigeria and South Africa (some of their largest

economies) struggling with weaker external demand and domestic problems.

Some economies in North Africa and the Middle East still remains weak in their growth because of dif cult

economic transitions and political situations.

All in all, global growth, though about 0.25% weaker than estimated projections in April 2013, is estimated

to recover from slightly above 3% in 2013 to 3.75% in 2014,

The outlook is still dominated by disadvantageous risks. Despite diminished tail risks in advanced

economies, to keep it at bay additional measures are required which include timely increase in the U.S.

debt ceiling and further action by authorities in the euro area to do whatever is required to avoid a sharp

deterioration in fnancial conditions.

In contrast, risk for a longer growth slowdown in emerging market economies have now increased due to

the prolonged efects of domestic capacity constraints, slowing credit growth and weak external conditions.

The forecasts assumes that the recent rise in fnancial market volatility and the associated yield increases

will partly reverse, as they largely refect a one-of reprising of risk due to the changing growth outlook for

emerging market economies and temporary uncertainty about the exit from monetary policy stimulus in

the United States. However, if underlying vulnerabilities lead to additional portfolio shifts, further yield

increases, and continued higher volatility, the result could be sustained capital fow reversals and lower

growth in emerging economies.

Policies to Generate Strong Growth

New challengers are brought to the table to global growth, global rebalancing and employment due to

weaker growth prospect and new risks, therefore policy makers around the globe have to increase eforts

to ensure robust growth.

Key advanced economies urgently need to pursue a mixed strategy that will support a short-term growth,

secured by credible plans for medium-term public debt sustainability. This will allow for a steadier near-

term fscal adjustment that will lead to low infation and sizable economic slack, and monetary policy

stimulus which will continue until the recovery is well established.

Additionally, potential adverse side-efects should be contained with regulatory and macroprudential

policies. Clear communication on the eventual exit from monetary stimulus will help reduce volatility in

global fnancial markets. Further progress in fnancial sector restructuring and reform is also required to

recapitalize and restructure bank balance sheets and improve monetary policy transmission.

In the euro area, a bank asset review should identify problem assets and quantify capital needs, supported

by European Stability Mechanism direct recapitalization where appropriate. Building on recent agreements,

policy makers should also make progress to a fuller banking union, including through a strong Single

Resolution Mechanism. Policies to reduce fnancial market fragmentation, support demand, and reform

product and labor markets are also crucial for stronger growth and job creation.

29

Cyclical positions and vulnerabilities vary across emerging market and developing economies, but

prospects of monetary policy normalization in the United States and a potential capital fow reversal have

heightened some policy trade-ofs. Risks of lower-than-expected potential output in some economies

suggest that there may be less fscal policy space than previously estimated.

Monetary easing can be the frst line of defense against downside risks, as infation is generally expected

to moderate in most economies. However, real policy rates are low already, and capital outfows and price

efects from exchange rate depreciation may also constrain further easing. With weaker growth prospects

and potential legacy problems from a prolonged period of rapid credit growth, the policy framework must

be ready to handle possible increases in fnancial stability risks. While macroeconomic policies can support

these eforts, the main instruments should be regulatory oversight and macro prudential policies.

Finally, the above measures need to be supported by structural reforms across all major economies to

lift global growth and support global rebalancing. As before, this implies measures to sustainably raise

consumption (China) and investment (Germany) in surplus economies, as well as measures that improve

competitiveness in defcit economies.

Bangladesh Economy

Bangladesh economy experienced fuctuating fortunes in FY 2013 with the economy moving towards a

lower level equilibrium in the course of the ongoing fscal year. On the one hand, the macroeconomic

stability was partially restored and rising infationary trends somewhat tamed, while on the other, economic

growth slowed down for a second consecutive year to remain below the target set out in Sixth Five Year

Plan (SFYP).

The prevailing stagnation in private investment was further aggravated by uncertainties emanating from

the ongoing violence and confrontational politics. Although both remittances and exports have posted

robust performance inspite of adverse global scenario, it was the domestic factors which had impacted

in an overriding manner on the macroeconomic performance in FY 2013. A number of weaknesses with

regard to macroeconomic management including governance of the banking sector and the debate

surrounding fnancing options for the Padma Multipurpose Bridge Project (PMBP) were on the policy radar

screen throughout the year.

The economic governance of the countrys power sector was also under the spotlight as the incumbent

government approached towards the fnishing line of its tenure. The external sector of the country also

faces formidable challenges in the backdrop of global uncertainty and faltering image of countrys ready-

made garments (RMG) sector. In the backdrop of these challenges, it appears that confrontational and

uncertain political environment had direct and indirect implications for economic performance in FY 2013,

particularly true for the second half of the fscal year.

One is apprehensive that the ongoing political impasse and the resultant adverse implications will leave an

unfavorable footprint for economic performance also over the upcoming fscal year. Overall, Bangladesh

economy is likely to remain in a dif cult terrain in FY 2014. As it is, the forthcoming budget will be the last

one to be presented by the present government. In the run up to the forthcoming national elections, the

government may like to revisit its pledges in the manifesto and in the SFYP, but in view of the past record,

the continuing fragility of the institutions and the looming political uncertainties, many of the objectives

and the indicators will likely remain unattained.

Monetary easing can be the first line of defense against

downside risks, as inflation is generally expected to moderate in

most economies...

30

aamra technologies limited I ANNUAL REPORT 2013

The macroeconomic performance in FY 2014 will critically hinge on the state of both economic and

political governance. For the second consecutive year, GDP growth rate in FY 2013 has failed to attain the

target. This is certainly a setback for the present governments plan to move the economy towards a higher

growth trajectory which is a necessary factor for attaining the middle income status by 2021. According

to the provisional estimates from Bangladesh Bureau of Statistics (BBS), GDP growth for the current fscal

year is expected to be 6.0 per cent; i.e. 1.2% points lower than the target (7.2%) and 0.2% point lower

from fnal GDP growth estimate for FY 2012.1 One may recall that, early projections by analysts were in

agreement that the growth rate in FY 2013 would remain below 6.0 per cent. 2 The SFYP planned to elevate

the average GDP growth rate during FY 2011-FY 2015 period to 7.2%; thus, GDP growth rate was expected

to be 8.0 per cent by FY 2015.

Indeed, successive failure to meet the target for GDP growth has made it dif cult to attain the objectives of

the medium term plan. For example, GDP growth rate would require to be 8.0 per cent in FY 2013 to meet

SFYP target. To cover the present gap between SFYP target and record of GDP growth performance, it will

be required to attain a 9.6 per cent GDP growth in FY 2014. This is a highly unlikely scenario. Consequently,

the SFYP targets have by now lost their relevance in view of the track record. Setting a high target of 7.2%

for FY 2014 is also not going to align trends with the SFYP targets.

FY 2013 has been one of worst years for private investment. The provisional estimate by BBS for FY 2013

anticipates a distinctive fall in the share of the private investment in GDP. It shows that private investment

is expected to decline as a share of GDP to 19.0 per cent in FY 2013 from 20.0 per cent in FY 2012. This is an

outlier because such a fall in private sectors share has never been experienced in the history of Bangladesh

(since FY 1981). This would mean that level of private investment would now move back to the level of FY

2007. This would also mean that, private investment in FY 2013 will be 3.7% points lower than the SFYP

target. This will surely have a dampening consequence from the perspective of the expected acceleration

of growth rates.

In contrast to the depressed private investment, public investment has increased steadily since FY 2009

and surpassed the SFYP target in FY 2013 (6.9 per cent of GDP) by about 1% point. According to provisional

estimates of BBS, public investment is expected to be about 7.9% of GDP in FY 2013. This implies that public

investment (as a share of GDP) will improve by 1.4% points in a single fscal year such an improvement

had never happened before!

Indeed, public investment as a share of GDP will also be the highest in the history. 7 Public investment in FY

2013 increased by 36.6 per cent compared to the previous fscal year. One may reckon that the provisional

estimate of public investment has considered a fuller utilization of original ADP (to the tune of Tk. 55,000

crore). ADP was later downsized (revised ADP (RADP)) and hence, the fnal expenditure fgure should be

lower. Nevertheless, it appears that public investment beyond ADP has also experienced a considerable

rise. It appears that, the estimate for public investment in FY 2013 is somewhat on the high side.

The banking sector in Bangladesh has come under criticism in the recent past due to increased number

of fnancial scams and the rising size of loan default. Undoubtedly, the size of the industry has expanded

in terms of total banks and their branches, deposits and credits which in turn have contributed to the

economic development of the country. The performance of the banking sector has also improved over

the years according to various indications such as capital to risk weighted asset, rate of non-performing

31

loan (NPL) to total loan, expenditure income ratio, return on asset, return on equity, and liquidity. This

has been possible due to various reform measures and policy support of the consecutive governments.

Unfortunately, the health check fails to conceal the problems sufered by the sector from time to time. The

current situation of large fnancial frauds and high NPL of banks calls for a close scrutiny of the sector and

necessitates taking required measures.

The power sector has undergone signifcant changes over the last four years with a view to raising

generation and supply capacities taking cognizance of the emerging urgency. As is known, the country

sufered from signifcant power defcit when the present government came to power in 2009 - total

generation of electricity was only 3268 MW at the time with a per capita access to electricity being only

183KWh. In this backdrop, the government undertook short, medium and long term programs based on

the national plan for power sector development. The major target of the plan was to ensure a moderate

rise in access to electricity in the shortest possible time. This target has partly been attained over the last

four years.

Bangladeshs export earnings stood at USD 21.78 billion, registering a moderate growth rate of 10.14 per

cent during July-April period of FY 2013 compared to the corresponding months of FY 2012. Indeed, whilst

this growth performance was notable by any measure, exports would need to grow by 37.8 per cent over

the remaining two months of the current fscal to attain the growth target of 15.3 per cent set for FY 2013.

It would thus be justifed to project that targets will remain unattained this year.

While Knit (8.9 per cent), woven (14.0 per cent), leather (19.6 per cent) experienced relatively high growth,

raw jute (-11.4 per cent), home textile (-11.8 per cent) and frozen food (-14.4 per cent) posted negative

growth rates during the July-April period of FY 2013 compared to the corresponding period of FY 2012.

During the same period of FY 2013, non-RMG sector did not exhibit a promising trend for export earnings.

As Table 6.3 shows, as a group export performance of RMG was better compared to that of non-RMG,

although both the groups are likely to fail in attaining the respective growth targets.

Business Performance

The year 2013 is projected to be alike 2012 in that the global growth will remain subdued, slightly above

3%. The prime reason for this is the slow growth and considerably weaker domestic demand in most of the

key emerging market economies as well as a more prolonged recession in the euro area.

Instability in the fnancial market has increased globally in May and June after a dormant period since

last summer. In advanced economies, long-term interest rate and fnancial market volatility have risen.

Fluctuating fortunes have plagued Bangladesh in the FY 2013 with the economy moving towards a lower

level equipoise in the course of the ongoing fscal year.

Despite both remittances and exports having posted strong performances in spite of adverse global

scenario, the superseding manner on the macroeconomic performance in FY 2013 was completely due to

domestic factors. Throughout the year the policy screen was plagued with a number of weaknesses with

regards to macroeconomic management most of which include governance of the banking sector, and

the debate surrounding fnancing options for the Padma Multipurpose Bridge Project (PMBP). Irrespective

of the political instability and economic recovery, aamra technologies limited (ATL) has posted a strong

operational and fnancial performance.

Bangladeshs export earnings stood at USD 21.78 billion, registering

a moderate growth rate of 10.14 per cent during July-April period of

FY 2013 compared to the corresponding months of FY 2012...

32

aamra technologies limited I ANNUAL REPORT 2013

ATLs performance for FY 2013 remained sound and strong, a remarkable achievement given the market

turbulence. This is due to the proper implementation of our focused and transparent strategy which

realizes predictable business performance over time and in turn, helps create value for our shareholders,

customers, employees and most importantly, the communities in which we operate. During the fnancial

year the company generated gross revenue of approximately BDT 717 million compared to last years

BDT 668 million. Gross proft was approximately BDT 186 million compared to BDT 145 million in last

year. Our prudent and ef cient teams are always a step ahead in adopting to the ever changing business

environment and are ever ready to accommodate the current need of the fnancial and telecom sectors

in Bangladesh. This along with our strong belief in the power of WE, have directly contributed to this

excellent performance. ATL recorded an underlying net proft after tax of BDT 73.3 million, up from BDT

62.5 million last year. Ef cient management and quick adoption of change environment have contributed

to this great achievement.

The highlight of ATLs business performance for the FY 2013 is most defnitely the business expansion in

the bandwidth market for which ATL acquired International Internet Gateway (IIG) license from Bangladesh

Telecommunication Regulatory Commission (BTRC) and has started commercial operation on September

15, 2012. The IIG license has generated proftable business opportunities for the company which clearly

had an impact on the revenue of ATL for the FY ended on June 30, 2013.

Along with being purpose driven, ATL considers itself as a socially responsive, respectful and an abiding

company. Our innovative strategy enables us to invest in high quality assets and to construct disaster

recovery services and other managed services for fnancial institutions and for telecommunication

industry. And we achieve this by implementing our strategy with integrity, strong moral ethics and in an

environmentally sound manner. Through committed leadership and disciplined operations, we see our

self-growing and thriving.

ATLs focused driven business strategy remained constant during the past year and as a leading provider of

high-tech and customized solutions to address a broad range of business IT needs in Bangladesh, we at ATL

are confdent in achieving continued success in the upcoming year.

Election/Re-election of Directors

As per Articles of Association, one third of the Directors shall retire from the of ce every year and they are

eligible for re-election by the shareholders of the company. As per Clause no. 91 of Article of Association of

the Company, Syed Faruque Ahmed and Syeda Farida Ahmed are due to retire. They are however, eligible

for re-election in the Annual General Meeting.

Audit Committee

The Audit Committee of the Company met four (4) times during the year and reviewed the following:

Audit and Inspection Report of the Internal Audit Team and External Auditor.

The Financial Statements of the Company audited by the External Auditors.

Stressing on the importance of the Compliance Culture within the Company.

33

Dividend

aamra technologies limited (ATL) has posted after tax proft of BDT 73.59 million for the year 2013. Basic EPS

stood at BDT 1.46, compared to the last years EPS of BDT 2.46 (reported) where restated EPS is BDT 1.17.

Considering overall market, current fnancial strength of the company and the prospect of further growth,

the Board of ATL has recommended 5% cash and 10% stock dividend for the year 2013.

Auditors

M/s. Masih Muhith Hoque & Co., Chartered Accountants, have carried out the audit of the company for

the fscal year ending on June 30, 2013. As M/s. Masih Muhith Hoque & Co., Chartered Accountants are

not eligible anymore, therefore as per eligible applications the Directors endorse recommendation for the

appointment of Malek Siddiqui Wali & Co., Chartered Accountants, as the auditors of the company for the

fnancial year 2014. The recommendation will be placed in the 24

th

Annual General Meeting for approval.

Acknowledgement

We take this opportunity, on behalf of the Board of Directors, to express my heartfelt gratitude to, all of

our valued clients, shareholders and well-wishers at home and aboard for their wholehearted cooperation

and active support in discharging the responsibilities reposed on me and the Board during the year under

review. We would like to express our sincere gratitude to the Registrar of Joint Stock Companies and Firms,

Bangladesh Securities and Exchange Commission, Dhaka Stock Exchange Limited, Chittagong Stock

Exchange Limited and all the scheduled banks and Leasing Companies for their sincere support and whole

hearted cooperation. We would also put on record my deep appreciation for the services and loyalty of the

executives, of cers and employees of the company at all levels without which we could not have achieved

this result.

We would like to thank and express gratitude on behalf of the Board of Directors to Mr. Syed Farhad Ahmed

Managing Director & CEO for his hard work, commitment and dedication to the welfare of our company.

The Board also acknowledges with thanks, the contribution made by the honorable Directors by guiding

and giving proper directions from time to time which has made ATL a Hallmark in Hi-Tech IT solution

provider in Bangladesh. Last but not the least certainly, we express our sincerest gratitude to all our clients

for their loyalty and patronage over the period. With our very best regards to all our valuable shareholders,

we promise to continue the growth with your support.

Thank you all.

On behalf of the Board

Syed Faruque Ahmed

Chairman

We would like to express our sincere gratitude to the Registrar of Joint

Stock Companies and Firms, Bangladesh Securities and Exchange

Commission, Dhaka Stock Exchange Ltd., Chittagong Stock Exchange Ltd...

34

aamra technologies limited I ANNUAL REPORT 2013

wcq kqvinvvie`,

Avmmvjvgy AvjvBKzg,

|<| +|| || (=|=)-=< |<|+<-< -- <||<+ |<|< | ||-< |

||| =< |<|| ||+ |<-- :, -::- < -| <<< <||<+ |<- | +<|<

| - +<|

ewkK A_bxwZ

-:- | |< || | |, | -| <|+ <|< -|< -::- +<| : |< ||

< |+ |+< <| -| |< ||--|< |+| +| =< < ++| <| <| <||<

|| <|< |< <|, | <| + -||| -| =< +|<

|| <|+ <|< < = |<| | || |+-, <| |+| |<<|| <|

<+|<|, -| <|<| |+|<| =< < +|< ||+ - |+| | =| |

|- +|| ||+ <| ||+ |-|< || |, |<<|| < <|-+ ||-+ || +<

|<+< ||| <|+ <|< ||< || <<| -< | < <| ||<

<||< =|+ |- +<|< =+| | - |< |+| || +<, |-|<<

=< -|< | <|<< |<|| |<+r|< | =+| + ||+ |+ ||<

| || ||+|< =| -<+|< =+|< , < |+ + <| <||< | ||+

-< |+ +||<|+ +<|< ||+ |+ |||| =< << <|-| <|-+ |+

-|< ||< | --<< | |+|<| +< - <|+ -<-|| =< +|||

=<<< |<|< +|| +| |<

|' + |<<|| =+| | <|< <, | |<<|| |+ <||< || <| <|

< ||| |+ <||<< |||| =< -||-| - <| |<<||

-|< =+| |< -|< <, ||+ <| + |< |$ $ <| |< |< -

|-|+, <| <||< ||| +| || , |-< +|< + |, ||

|| <$, -|< < =< |+ < <|-| - -<< -| +||<|, < |||

-< -|< =< < ||||< +|<

<|+ <| || <$ -:-'< <|< |< <||<+ -|< | -.c, -::'< | - -.-c

(-< | :) < = |||| <| || +|< |

1. AMmigvb evRvijvZ cew nvm:

| <|<|

<|<|< <|- <|< ||--|

<+||| |<<|

|<|| <-<

|<-

35

|< -| + |+|

|+ |||| + ||

-< ||

2. BDiv Aji MfxiZi g`v:

-< <|*|

'|<|' ||< <|

'|<|' ||< +| ||+ =< -|

| ||--|

3. gvwKb A_bxwZi axi mcmviY

|<| <<+|<| ||--|< < ||| |+ +| <

=< |+< * |<<| || =+|

| <| | +<|, | ||+|< ||

-| | <||, | =< <<| -:-

< +<| - < |<| |<< <||

+< , ||+ <| <| <<| -|

| -:-- <| |< +<| : + <<

+< :.-c + -.-c =| | +<

<||+< <| |+ |<<| +<< -:- ,

||+ = | |+|

|| $ <| -::- -< | -, |

<|+|< < ||+ |+ ||<

|<|+ |<< +|<, || =< <| ||--|

| < || <|+ < +< |-| | -|+, <|+ -< |<<< +|< |+| +| <|| -:-'<

= =|+| <| - ||| | :.-c <| =|+| -||< |<<|| |+< -::'< +|

+|< .c =< < |||+ +| |<<|| |<< +|< <|<||< =< || <|<|< ||

|<< +|< <| | =< -::'< |<| << |<||+ +|< -:-- <| <|$< | +||

= =|+|< < | | +<| -| |< + -<

-::- c =< -:-- | c.c <| <||< =< ||| <| = || +<|

- <$ |< |<+< -|, | .-c <|<| =| -::- | | |< (|==-=<

|<< <|| +< , ||+ <| <| <<| -| | -:--

<| |< +<| : + << +< :.-c + -.-c =| | +<

<||+< <| |+ |<<| +<< -:-...

8

7

6

5

4

3

2

1

0

-1

-2

13:

Q4

2011 12

Advanced economies

World

Emerging market and

developing economies

Figure 1. Global GDP Growth

(Percent; quaeter over quarter, annualized

36

aamra technologies limited I ANNUAL REPORT 2013

| +||+ |+ ||) +|< =|+|| -< ||< |||< +< -::-:--

| <| -< -.-c, | -:: + .-c +, -:- + .c + | + =| -::- +<|

<||< * *|-| <| |<+-=< <|| ||< +< | .-c + =+ |< .-c

+|| -

|+ < + <||+|<+< < | + |<| |<| ||- +<|, |<+< <

|- |<-|-|<| ||+| ||<| =< | ||+| -<< <|- ||--| || |<

+|< <| -<< -< < ||+| =< <|< < |+ || =| -< < |-< <|,

+|< +| |+ ||< =< <||+ |<||< -< <|+ <|+ <| |- | .-c -<,

-::'< =|< <|| + | < +< |-|< +<| - || : =< < -::'< + -:--

:.-c |+ =| |<| | |<<|+ |+< +|< < ||< ||+ |+

=|+ + |$| < <<| -< | | -< ||+ < | ||<|< =< <|

+ +< |<| <<| - | =+| |+ |<|< -| |<| - | =|$ || |

|<<| |-+ -||-| <| < - ||< |+ = <| <||< ||| <| ||

|< <|<|< | |<< +|<, <| < -|< +|< =< -< <|-t |<|< +|<

<|| | +<| - ||+ <||<< |<| =< ||+ | =< | | <|< +|< | ||+

< -|$|< - | <|+|< | | |+< t| =+ | <T +< |<<| <| ||

<| <||< ||| =< ||+ || ||+ <|< ||+ |+| | -|+, |- -

| <-|| ||< ||| |<<< |-+ <||< -, | |< <| | =< |<| ||

<-| |+ |- |< | -< |<<|| < <|-< |<<| || =< ||| <| + ||

kwkvjx cew ARbi bxwZ

<|+ <|< ||+ |||< |< | || - | - <|+ |<| =< +|

-< <| || =< |+< +|< , +|< |<<|| |||<|<+-< |+ ||< <|

<|$||< |<<|+ ||+ +< -, <| < |||+ <<| || =+| | + <<

| - $ | =+| r |-| <| +<<, | | -< |<|| |<+r| =< < |-|

<+|<| < |+ |+|< < |- =| =+| |+ |-| ||+ |+<< ||||+ |- -< |

| -||| || |+ |<<|< |-+ || +<< =< ||+ || <|- |+< |||<

|< |

|<|+ =< -<-| <||+ ||< |<| |< ||< ||||| |+ <|| |< |+ |-|

+, |<| =< + <|$ || + |<|< ||| <|+ ||+ <||<< |<| +| |-|

+<< |+ ||+ || |< | <|+< =< <|+< ||< +|||

|<| <| t+||| |<|< -<+|< <| +, =+| <|+ - |||, -

=< << |<| |<|<< ||+ ||- +<<, | <|| |||| + |<| |

| <||< <|+< | ||+ || | - |||<|<+-< =+| ||| =++

|<| ++ +<|< |< |<+< t<||+ | +< -|<||< |+< -| +<

||||, ||--|+ =< <||< < ||| <| =< +| ||+ +<

< - -< <| <||< =< | |||+ |+|< <| =< *<| |+ |<|

37

-, |+ -|||< |||<+|+< ||+ <|< || =< =+| |< < <|-< | || |+

|| |<<< | <| +< || |-< |< + ||< |+ |+ || <|

- , ||+||< | + |<, < | |-|< +<| -| | + ||< |+< |<< ||+

-|+< - |< |< |<<| <<|, - |<|< || +<| - |+ , <|< | ||

-||| -< | | -|+, + || -|< |< < + =< << <|-t<|- =< -|<

|<| -|< + < < |+ |- |< |<+< -|+<+ -< <|< || =< |<

|< <||<+|< =+| | < - <|- + || +|||+ < - -<

|+ ||||< |+ <|+ |+|<| +< <||+ |+ ||- =< |+

+< |<, <| <+<|+ < |<+||| =< <||+ -<-| |||< < | |+|<|

- -< $||<, <| <<||< <<-|< +||| , <|+ |<| || <

<$ || | +<| <|+ <|+ < <<< |< |, =| |* +<, + |<

<| <<| (|) =< |<|| (|||) < |||, | = <<||- | || |||<

||||+ <| +<<

evsjv`k A_bxwZ

<||- || || | +< -:: <<< |< | | || | <<< ||

=+| || |<|< |-+ || - |-+, <||+ |+ ||||+ ||+ <||< +<|

-| =< +||< -|||< |+ || -| -| |-+ |+ <| -| <<

|| <<< | < | | | :^ | << |-| |<+r| |< +<| -|

<<+|<| |<|| |<<|| |<<| |<| <| <$| | | =< <||+ <| |+|<

+|< |- <|* =< <||, -|< -| - +< <|+ |<< |<| <| , =|

| |<| |-|- | -:: <<< <|+ || |< < =+| |+|<| <|

| <|+ |+ <<||< |<<| |++ -<| <||+ < |- =< -| |<+r|

||<||+ |<+r <| <:| +r< | | <<<|| || < +|

-< |<- < <| |+ <<|| <| <+|< < - =< |-< < -< <|-

< |+ ||+ |+|<| +< <|+ |+| =< -< <| ||+ |r< <|<

|<| =< |< |<| = - ||<+ =< ||+ <||+ |<< <||< <|

<| |< -:: << |+ < <, =| |<< +< <| <<< |||<

=+| |<< | +<| | , | <||+ |<| =< |< |<|+ +|< < | -:- <<<

<||-< ||+ ||+ =+| |<-+ |<|| < - | <| - <| <+|<

|| << <|, <<| || |<|< | <+|< < |< || =< :^ +-

<||<+| |<+r| |< |||+ < +<< |+ | ||< ||+ |^||< <| *<|

=< <||+ |+| | -| =< |-+|< < +| < | -< |

-:-'< <|+ |+ -| |<|+|< <|<| +<< = |+ <|< << <|+|

, | <||-+ --: | ||- =+| < |< - <||< -<|< <|<| +<< <|<|<||-+|<

- |||< |||<+|+< ||+ <| < || =< =+| |< <

<|-< | || |+ || |<< < < | +< ||...

38

aamra technologies limited I ANNUAL REPORT 2013

|| <<< ||| <|< -|< -:: << +< < - =| < <| <+|<<

|<+r| <|<|| -<|< || |-| <||- |<| <<|'< (|<|<=) ||+ |-|< ||

<| <<< |||< <|< -|< || - :-=, | - || (-.-)-=< :.--

=< + =< $| ||| <|< -:--=< |-|< + .- + + '< +< |< , |<

<||| = |< < <| =+ -| , -::-=< <|< -|< :-=< | |+< :^ + <||<+|

|<+r| $ ||| <|< -|< -:: + -:c << -.--= | +< |<+r| |

-

+|< -:c << ||| <| || | - |, ||| <| =< <|<|<||-+

<| < |-| |<+r|< - ++< +< -|-< < +<||<+| |<+r|<

-:: << ||- ||| <|< -|< - | -|< -<+|< | ==|| || =<

||| <| < |<<<|< < |<<|| <| |+ -< +< -:- << ||- >.: -|< |||

<| | =| =+| < <+< -+r | == | | ||| | <

|<<| || -||< -:- =< -.- =< =+| || |<|< ==|| ||< *

=+ | <|

-:: << | <<+|<| |<||< |+ <<|< < =+|, |<|<= =< |-|< -:: <<<

<|| ||< =+| <<+|<| |<||< ||| | +<| -| =| -|

<<+|<| |<|| |||< -| |< - -:: <<< |||=< =+| |-< -:- =< -

+ + -::-= :> -< =| =+| |<< | +|< <||-< |-| (:>-: << +) <<+|<|

= || +| +<| =| |< <| |< <<+|<| |<|| -- <<<

| |< |< =| |< <| -:: << |<|| -< ==|| ||< :.-

+ =|< < =+| -|-|+|<| | |+<, || -|<< <|< << |<| <<+|<|

|<||< -|< |<| <+|<| |<|| ||< <| -> << + =< | -::

<< :^ + <||<+| |<+r|< || ||$ (|||-=< :.>) | : -|< |<|<=< |

|-< || -:: << || +|<| |<|| -< |||-=< -.> | |* +< , <+|<| |<||

(|||< =+| |-<) :.- -|< =+| =++ << <| |<- = =< | +| |

| |||-=< |-< -:: << <+|<| |<|| -< |-| <| -| <+|<| |<||

::.: -|< <| |< <<< | <+|<| |<||< | |-|< =+| <<-|< |

<||<+ |<+r| (+| -||< +|| |+|< ||) |<<| +<| -| <||<+ |<+r| (=||)

+| | - (|<=||) =< +|< $| << + + |< | -| | <+|<| |<||

=||'< =| =< || | +< =+| |<<|| | = - , -:: <<

|-|<+ <+|<| |<|| |+| |||<|

<||-< <||+ ||+ | ||| - <| + ||+ -||< +|< =< |<|<<

<|< |+|< <$ || --|||< <| | |r|< |+|< | <|+ =< ||< |, |-|

=< < |<| |<<| ||< - | | -< |+ <-| < <||+

< -| ++ << << | -, -< |+< || |<<| <, | < | |

< -|<, |-<< |, - + |, < + |, - + | =< |<| || |<<|

=| < - << <+|<|< |<| + <<||- =< || < -|<,

39

= |< <| |+<| || + <| < - <$ ||< |+ -|| =< ||<

<|+< | -||< || = |<| || =< || <<| - +<| -<+|<

|< |< << |<- | ||< -, |- <| =< <<<|- | |<<| = <<|

<| |+|<|< | |<<| < =- <$ <<< |<- || | <| <+|< ->-=

| | | |<- |- | | :-:- || ||| |<- <<-|<< | | <<| :-:

|+|| | = <|< |<| <+|< r < <, -| |-| +| - +< |<- |

|| |<+r|< < || +< = |<+r|< <| | |< r < < |<- <<-|<< |

| ||||< ||+ +<| = c << +| | -

<||-< <|| | -||$ -:.-- |<| ||+ |< | -| , -:- <<< =+ ||<

| -:: <<< =+| < <|< -|< :.:- + , = <|< | |

+| | <||< | | :-.- <| || <| << <| -|< < |< +<

=| +< -::- =| |<|< +<| -| :c.: | =| <|| +<| |+ -< , = <<

| || + |<

| (-.>), (:-.), |$| (:>.>) || | +< | +|< <|, +|| |

(-::.-), -| +| (-::.-) =< |-|| |<|< (-:-.-) |+ <| +< -:--=< |

+ =| -:: <<< =+ < | -:: <<< =+ <| |<|+ |r <|

| | <|| |< ||| << - +< |<| | :.: < + -| |, <||

< =+| - <| |<|+ | +< <| |<|+ <| | |< | |- -

<t | | <|< || < - |

eemv ARb

-::'< <|| +<| - , <|+ <| -:-'< | |+< : =< |+| < =< <| +|<

- |<< <| =< |<<|| -<< -| ||--| <|< | <| <| ||| |

| <| + =+| |<+< | -|

|<<|| ||+ <||< =< | |||| <| =+| ||| |< |'< < +

<| ||| -||-| -< -|< =< ||+ <||< |<| <| |-< |

<||- -:: << |$ $ || || <+<||- |||< - |<| << $

<|* =< <|| ||| -| | <|+ |<| <|< || -:: <<<

<|+ |+ |<|+ <| | < || +|< |+ + -<| <|+ |+

<<|| |< <||+ < | =< | |<+r| | ||<||+ |<+ <| <:|

+r |< <| <||+ |||| =< |+ |< ||<< |<| +|| |. (=|=)

=+| |||, +| =< ||+ - +<

-:: << =|='< < | =< ||| =+| -| <||< < |$| |< =|

- ||-< ||< | <|<| =< ++ | || <|||+ + |< <|<|

+< =< | ||-< |<-||<, | =< +| | ||^< | -|| +<

<||-< <|| | -||$ -:.-- |<| ||+ |< | -| , -:-

||+ <<< =+ ||< | -::'< ||+ << =+| < <|< -|<

:.:- + , = <|< | | +| |

<||< | | :-.- <| ||...

40

aamra technologies limited I ANNUAL REPORT 2013

<<<|| +||| <||-| |+| | -:- || | | +< | |< << <||-| |+|

::- ||< || =<< | | - <||-| |+| | :-: || | << | <||-|

|+| :-c || ||-< -<-| =< - < <-| | |<<| |<<+ - +< =+ <|

=| |+ =< <-| |+ <| ||+ |^|< | =< <||-< |+ || +<

| = +|< < - ||< "- ||-< |<| <||< <-| < =|= |

+< | | | | <||-| |+| -:.: || +< -|< <, | | |< << c-.-c ||

|+| = < <-| < - <<|| =< |<< |<<< | - || | -::

<< =|='< <|||+ < < | - , <| <||< <<| |< |< =|=

| +< <||- |+||+ | +| (|<||<|)-=< |||+ |< |* |

<|||+ |<|| << +< -:-'< :c < + |*| |< < <<|< <| +< <

| +|||< |< < : -::- |< <

+ |<| |<|| -|< * * = =|= |+ |||+|< -|||, || =< +|||

|-< |<<| +< ||-< |<| + - |<|| +< - =< -|<

|+|<|- ||+ |^| =< |||| |r< | <| -|< -| +< |-|, |||

|+ |< =< |<<|< =+| -< <|- ||-< + <|<|< < |- |*+|<|<

=< | |<||< |< |<| ||-< |-|- =< | <||

|<| +|| ||-=< - =+<< << <|||+ + ||| < =< =+|

-|+|<| ||< =< |<|| |<| <<|<-+|<| < <||- |< <<|< |

|, =|= <<| << <|<|<|-+ | ||<||

cwiPvjK`i wbevPb/cybtwbevPb

||< ||+ =||" || |<|+<-< =+ || |-< - + + << <<

|< =< |<| |< -||<-< |<| t|<|< | -< >: - || - |<+ |--

=< -| |<-| |-- <<< | <

AwWU KwgwU

=+| |<|| +|| |<<|< = << << || - |<| ||<|- |< |<<| || +<

<|- |< =< |<| |<< |<|| |<- |<-

<|- |<|+< |<| |<|| +|||< ||+ |<-

+|||< |<| | + ||* =< << < |< -|

wWwfW

|<| +|| || (=|=) -:: | -:.c> || |+| +< <|- | | +< |

|<< |+ | -||$ :.-: |+| | |< << | -.-: |+| (-|) | |< |= -

:.:- |+| ||<+ <||< =< |^|< <| ||+ | =< <<| || <| |<<| =|='<

|<|+| -:: |< +<| c | - =< : | <|| |< ||-=< <||<

+<

41

wbixK e`

| |- |- -+ = +|, || =|+| -:: =< : < -| <<< |<||

+< - | |- |- -+ = +|, || =|+| |^|| |< |<| +|| ||

-=< || | -|< | - |<-< |<| |<|+ <- |+ ||++| || = +|,

|| =|+|+ -:- | <<< |<|+ || +< ||< +< ||<| -- <||<+

|<|< | |-< +<| -<

abev` vcb

|<|+<-< < + ||-< + |-+, |<-||< =< <|+||-< | ||<+ +| |

+<| |<| +| | +<| |<| |< <<<|| - =< |<- + ||-< | |-< <|+

-|||| =< | || |<| ||<+ | ||| + +||| =< |-<

|<T+, <||- ||+|<| = =+ +|, |+| + =+ ||, 1| + =+ ||

=< < || <|+ =< || +||||+ ||-< | |-< |< < |<| | |

+<| ||-< |<|-| ++| =< +|-< | |-< <| =< |^|< | < | |< | |$|

|<| = | +< |<| |

|<| |<|+<-< + <<|- =< +| || | <<|| |<|+ =< <| |<|-| ++|

|< - <-|- |--+ +|||< +| |< +| |< |*+|<< |<|| <- |<|

<<|- || || |<|+<-< || |-+|-| -< | |<| +||

||+ =+| + ||< |^| < <||- =+| -|-< |-< $

<<, |-< +| | < , ||<+ +| || ||-< + |-+-< = -| ||-< |

|-< < |<| || |-| ||-< ||-< <| <|- <||<

<|+ <<|-

- |<+ |--

|<|

|<| ||<+ | ||| + +||| =< |-< |<T+,

<||- ||+|<| = =+ +|, |+| + =+ ||, 1| +

=+ || =< < || <|+ =< || +||||+ ||-< |

|-< |< < ...

42

aamra technologies limited I ANNUAL REPORT 2013

Fairness, Transparency, Accountability and Responsibility are the minimum standards of acceptable

corporate behavior today. At aamra technologies limited, corporate governance means increasing the

shareholders value by being ef cient, transparent, professional and accountable to the organization,

society and to the environment.

Board of Directors

There are 5 members in the Board of Directors. Out of the 5 members, one member is an Independent Director.

All our board members include persons of high caliber, with academic and professional qualifcation in the

feld of business and professionals. This gives strength for efective discharge of duties and responsibilities

by the Board. The Board approves the companys budget and business plan and reviews those on a regular

basis so as to give directions as per changing economic and market environment. The Board reviews the

policies and manuals of the various segments of businesses in order to establish efective risk management

in credit and other key areas of operations. The management operates within the policies, guidelines and

limits approved by the Board.

COMPLIANCE REPORT ON CORPORATE GOVERNANCE

Status of compliance of the conditions described in SECs Notifcation No. SEC/CMRRCD/2006-158/

Admin/02-08 dated February 20, 2006 issued under Section 2CC of the Securities and Exchange Ordinance,

1969 (XVII of 1969) regarding Corporate Governance is given below in pursuance of condition No. 5.00 of

the said notifcation:

Condition

no.

Title

Compliance Status

Explanation Non

compliance with

the condition

Compiled

Not

Compiled

1.00 BOARD OF DIRECTORS

1.1 Board Size

1.2 Appointment of Independent Director

1.3

Chairman of the Board and Chief

Executive

1.4

The Directors' Report to the

Shareholders

1.4 (a) Fair presentation of the state of afairs

1.4 (b)

Proper maintenance of books of

accounts

1.4 ( c)

Application of proper accounting

policies in preparation of fnancial

statements

1.4 (d)

Adherence to International Accounting

Standards

CORPORTE

GOVERNANCE

43

Condition

no.

Title

Compliance Status

Explanation Non

compliance with

the condition

Compiled

Not

Compiled

1.4 (e) Sound Internal Control

1.4 (f ) Ability to continue as a going concern

1.4 (g)

Deviations from operation of the

previous year

1.4 (h)

Presentation of key operating and

fnancial data of the last three years

1.4 (i) Declaration of Dividend

1.4 (j) Number of Board Meetings Held

1.4 (k) Pattern of shareholding

2.00

CHIEF FINANCIAL OFFICER (CFO), HEAD OF INTERNAL AUDIT AND COMPANY

SECRETARY

2.1

Appointment of CFO, Head of Internal

Audit and Company Secretary

2.2

Requirement of CFO and Company

Secretary to attend Board Meeting

3.00 AUDIT COMMITTEE

3.1 (i) Constitution of Audit Committee

3.1 (ii)

Appointment of independent director in

Audit Committee

3.1 (iii) Vacancy in the Audit Committee

3.2 (i)

Selection of Chairman of the Audit

Committee

3.2 (ii)

Qualifcation of the Chairman of the

Audit Committee

3.3 Reporting of the Audit Committee

3.3.1 (i)

Reporting of the Audit Committee to the

Board of Directors

3.3.1 (ii) (a) Report on confict of interest No such case arose

3.3.1 (ii) (b) Suspected fraud or irregularities

3.3.1 (ii) ( c) Suspected infringement of laws

44

aamra technologies limited I ANNUAL REPORT 2013

Condition

no.

Title

Compliance Status

Explanation Non

compliance with

the condition

Compiled

Not

Compiled

3.3.1 (ii) (d) Any other matter No such case arose

3.3.2

Reporting to the SEC by the Audit

Committee

No such case arose

3.4

Reporting to the shareholders and

general investors

4.00 EXTERNAL / STATUTORY AUDITORS

4.00 (i)

Appraisal or valuation services of fairness

opinions

4.00 (ii)

Financial information systems design

and implementation

4.00 (iii)

Book keeping or other services related to

the accounting records

4.00 (iv) Broker-Dealer services N/A

4.00 (v) Actuarial services N/A

4.00 (vi) Internal audit services

4.00 (vii)

Any other services that the Audit

Committee determines

The Audit Committee [3.00]

Sl Name Designation

1 Mr. K.M.Hasan, FCA Chairman

2 Syeda Munia Ahmed Member

3 Fahmida Ahmed Member

45

The audit committee makes recommendation on

the reporting, control and compliance aspects of

the Directors and the Companys responsibilities,

providing independent monitoring, guidance and

challenge to executive management in these areas.

The audit committee on behalf of the board strives

to ensure efective implementation of the processes

and procedures set out in the business plans and

policies. Its aim is to ensure that high standards of

corporate reporting, control and compliance are

achieved, in the belief that excellence in these areas

enhances the efectiveness and reduces the risks of

the business.

The composition of the committee

In accordance with the currently accepted best

practices and corporate governance guidelines,

the board appointed audit committee comprises

of the following non-executive and independent

directors of the company:

Name of Members

Position in the

Committee

Position in the

Board

Mr. K.M. Hasan, FCA Chairman

Independent

Director

Syeda Munia Ahmed Member Director

Fahmida Ahmed Member Director

Meetings of the Audit Committee

The Committee held four meetings during the

year under review. The terms of reference of the

audit committee clearly defnes the roles and

responsibilities of the audit committee. The terms

of reference is periodically reviewed and revised

with the concurrence of the board of directors.

The roles and functions of the committee are

further regulated by the rules governing the

audit committee as specifed by the conditions/

guidelines on corporate governance issued by the

Bangladesh Securities and Exchange Commission.

Activities of the Audit Committee

The audit committee carried out the following

activities during the year:

Reviewed the systems and procedures to

ensure that all transactions are completely and

accurately recorded in the books of account;

Reviewed the accounting policies and to

determine the most appropriate accounting

policies after consideration of all choices

available;

Reviewed the efectiveness of the fnancial

reporting system in place to ensure reliability of

the information provided to the stakeholders;

Reviewed and approved the Annual Financial

Statements prepared for publication, prior to

submission to the Board;

Reviewed the efectiveness and independence

of the statutory auditors;

Recommended the re-appointment,

remuneration and engagement letter of the

statutory auditors;

Reviewed management reports together with

the managements response thereto and the

audited fnancial statements with the external

auditors.

Acknowledgement

The Audit Committee expressed its sincere thanks

to the members of the Board, management and the

Auditors for their support in carrying out its duties

and responsibilities efectively.

K.M. Hasan, FCA

Chairman

Audit Committee

REPORT OF THE

AUDIT COMMITEE

46

aamra technologies limited I ANNUAL REPORT 2013

Board of Directors at the

23

th

Annual General

Meeting (AGM) of aamra

technologies limited

PICTURE

GALLERY

Board of Directors &

Shareholders at the

23

th

Annual General

Meeting (AGM) of aamra

technologies limited

Shareholders at the

23

th

Annual General

Meeting (AGM) of aamra

technologies limited

47

Board of Directors

9

th

Extra Ordinary General

Meeting (EGM) 2013

aamra technologies limited

A shareholder speaks at the

9

th

Extra Ordinary General

Meeting (EGM) 2013

aamra technologies limited

Shareholders at the

9

th

Extra Ordinary General

Meeting (EGM) 2013

aamra technologies limited

48

aamra technologies limited I ANNUAL REPORT 2013

aamra becomes a Gold

Member of Bangladesh

German Chamber of

Commerce & Industry

PICTURE GALLERY

Mr. Syed Farhad Ahmed,

Managing Director of

aamra technologies limited

speaks at the Bangladesh

Investment Summit, Europe