You might also like

- Inside the Foreign Exchange Universe: (An Essential Guide to Forex)From EverandInside the Foreign Exchange Universe: (An Essential Guide to Forex)Rating: 4 out of 5 stars4/5 (1)

- Global Financial System: International InstitutionsDocument21 pagesGlobal Financial System: International Institutionsapi-265248190% (1)

- 01 Global Financial System: 1.1 International InstitutionsDocument25 pages01 Global Financial System: 1.1 International Institutionsapi-26524819No ratings yet

- IFM UNIT - 1 - CompressedDocument36 pagesIFM UNIT - 1 - CompressedChirurock TrividhiNo ratings yet

- FIN 422 (Chapter 2)Document9 pagesFIN 422 (Chapter 2)Sumaiya AfrinNo ratings yet

- Chapter 4 The Interntional Flow of Funds and Exchange RatesDocument14 pagesChapter 4 The Interntional Flow of Funds and Exchange RatesRAY NICOLE MALINGI100% (1)

- International Monetary and Financial Systems - Chapter-4 MbsDocument62 pagesInternational Monetary and Financial Systems - Chapter-4 MbsArjun MishraNo ratings yet

- Monetory Eco Assignment and PPTDocument8 pagesMonetory Eco Assignment and PPTobayed florianNo ratings yet

- IFM1Document12 pagesIFM1Shaan MahendraNo ratings yet

- International Economic Integration and Institution WRDocument10 pagesInternational Economic Integration and Institution WRYvonne LlamadaNo ratings yet

- Ethical Practice in Correspondent BankingDocument35 pagesEthical Practice in Correspondent Bankingmahesh ojhaNo ratings yet

- BBA607 - Role of International Financial InstitutionsDocument11 pagesBBA607 - Role of International Financial InstitutionsSimanta KalitaNo ratings yet

- Q1) Factors Affecting Exchange Rates: Interest and Inflation RatesDocument7 pagesQ1) Factors Affecting Exchange Rates: Interest and Inflation RatesMandar SangleNo ratings yet

- Main Factors That Influence Exchange Rate.: 1. InflationDocument9 pagesMain Factors That Influence Exchange Rate.: 1. InflationHiren GanganiNo ratings yet

- Winter 2017 BBA Semester 6 BBA603: Role of International Financial InstitutionsDocument10 pagesWinter 2017 BBA Semester 6 BBA603: Role of International Financial InstitutionsSujal SNo ratings yet

- MF0015 - International Financial Management - Set - 2Document10 pagesMF0015 - International Financial Management - Set - 2Shilpa PokharkarNo ratings yet

- Case C8Document6 pagesCase C8Việt Tuấn TrịnhNo ratings yet

- Key Currencies:: Share of National Currencies in Total Identified Official Holdings of Foreign Exchange, 1998Document12 pagesKey Currencies:: Share of National Currencies in Total Identified Official Holdings of Foreign Exchange, 1998KaranPatilNo ratings yet

- DownloadDocument4 pagesDownloadmanirajpoot45No ratings yet

- Module 2 PDFDocument29 pagesModule 2 PDFRAJASAHEB DUTTANo ratings yet

- RizwanDocument9 pagesRizwanRizwan BashirNo ratings yet

- Factors Affecting Exchange RatesDocument9 pagesFactors Affecting Exchange RatesAnoopa NarayanNo ratings yet

- MODULE 8 ReportingDocument7 pagesMODULE 8 Reportingjerome magundinNo ratings yet

- Class Notes All But The Quiz 2 PDFDocument49 pagesClass Notes All But The Quiz 2 PDFAzim HossainNo ratings yet

- Done Motives For Using International Financial MarketsDocument6 pagesDone Motives For Using International Financial Marketskingsley Bill Owusu NinepenceNo ratings yet

- Chapter 4Document24 pagesChapter 4Manjunath BVNo ratings yet

- Tugas Bisnis Internasional Financial ForcesDocument5 pagesTugas Bisnis Internasional Financial ForcesPutry AgustinaaNo ratings yet

- Chapter 1 Why Study Financial Markets and InstitutionsDocument17 pagesChapter 1 Why Study Financial Markets and InstitutionsJay Ann DomeNo ratings yet

- Factors That Influence Exchange RatesDocument2 pagesFactors That Influence Exchange RatesJoelene ChewNo ratings yet

- Factors Affecting Exchange RatesDocument2 pagesFactors Affecting Exchange Ratesanish-kc-8151No ratings yet

- Research Project ReportDocument55 pagesResearch Project ReportharryNo ratings yet

- Unit - 1Document8 pagesUnit - 1VaghelaNo ratings yet

- Quiz AnswerDocument11 pagesQuiz Answercharlie tunaNo ratings yet

- Big Picture C UlocDocument5 pagesBig Picture C UlocAnvi Rose CuyosNo ratings yet

- Finmark ActivityDocument4 pagesFinmark ActivityKoo KooNo ratings yet

- Fundamentals of International FinanceDocument11 pagesFundamentals of International FinanceChirag KotianNo ratings yet

- Project Report On Currency MarketDocument54 pagesProject Report On Currency MarketSurbhi Aery63% (8)

- Lesson 2Document5 pagesLesson 2Eloysa CarpoNo ratings yet

- JUNE 2015 Q.8: Short Notes: 1. IMF (Repeated) 2. European Union - EUDocument9 pagesJUNE 2015 Q.8: Short Notes: 1. IMF (Repeated) 2. European Union - EUHafsaNo ratings yet

- Background of Foreign Exchange MarketDocument9 pagesBackground of Foreign Exchange MarketLiya Jahan100% (2)

- Leela Mam Ques & AnsDocument30 pagesLeela Mam Ques & AnsBhuvana HariNo ratings yet

- Balance of PaymentsDocument12 pagesBalance of PaymentsRahul DebNo ratings yet

- How Do Central Banks Manage Exchange Rates?: by P. Samarasiri, Assistant Governor, Central Bank of Sri LankaDocument10 pagesHow Do Central Banks Manage Exchange Rates?: by P. Samarasiri, Assistant Governor, Central Bank of Sri LankadewminiNo ratings yet

- Important Interntional FinanceDocument42 pagesImportant Interntional FinanceShivanjali JadhavNo ratings yet

- Trade Barrier: Trade Barriers Are Government-Induced Restrictions OnDocument5 pagesTrade Barrier: Trade Barriers Are Government-Induced Restrictions OnThanasekaran TharumanNo ratings yet

- Prayoga Dwi Nugraha - Summary CH 12 Buku 2Document10 pagesPrayoga Dwi Nugraha - Summary CH 12 Buku 2Prayoga Dwi NugrahaNo ratings yet

- Project Report On Currency MarketDocument54 pagesProject Report On Currency MarketMansi KotakNo ratings yet

- Financial Derivatives and Risk ManagemenDocument9 pagesFinancial Derivatives and Risk ManagemenDwi EriantoNo ratings yet

- ForeignDocument70 pagesForeignadsfdgfhgjhkNo ratings yet

- Module 3 Lesson 3Document15 pagesModule 3 Lesson 3Marivic TolinNo ratings yet

- Foreign Exchange Is Essential To Coordinate Global BusinessDocument7 pagesForeign Exchange Is Essential To Coordinate Global BusinesssaranistudyNo ratings yet

- Exam Assigment of IFMDocument9 pagesExam Assigment of IFMPunita KumariNo ratings yet

- International Financial Management Unit - IDocument15 pagesInternational Financial Management Unit - IBHRAMARBAR SAHANINo ratings yet

- Narrative Report For FINANCIAL MANAGEMENT, PedrosaDocument3 pagesNarrative Report For FINANCIAL MANAGEMENT, PedrosaAlfredJoshuaMirandaNo ratings yet

- Chapter 9-Pricing and FinancingDocument22 pagesChapter 9-Pricing and FinancingcchukeeNo ratings yet

- TFM Session Five FX ManagementDocument64 pagesTFM Session Five FX ManagementmankeraNo ratings yet

- Lecture 4Document33 pagesLecture 4Jelani GreerNo ratings yet

- 1.what Is An Exchange RateDocument15 pages1.what Is An Exchange RateCristina TobingNo ratings yet

- Exchange Rates Foreign-Exchange Rate, Forex Rate or FX Rate)Document5 pagesExchange Rates Foreign-Exchange Rate, Forex Rate or FX Rate)SaadRasheedNo ratings yet

- Week 6 IMS, BoPDocument18 pagesWeek 6 IMS, BoPMustafa KhanNo ratings yet

- Planning ProcessDocument70 pagesPlanning ProcesskishenavNo ratings yet

- "Coming Together Is A: BeginningDocument28 pages"Coming Together Is A: Beginningapi-26524819No ratings yet

- Leadership Final Presentation : Free DownloadsDocument41 pagesLeadership Final Presentation : Free DownloadsNishantha100% (7)

- International Business Management: TH STDocument4 pagesInternational Business Management: TH STapi-26524819No ratings yet

- What Is Management?: Management Is A Art of Getting Things Done Through PeopleDocument15 pagesWhat Is Management?: Management Is A Art of Getting Things Done Through Peopleapi-26524819No ratings yet

- Management Process: Lecturer: H.P. Rasika Priyankara Unit Title: BM 311 Year I Semester IDocument58 pagesManagement Process: Lecturer: H.P. Rasika Priyankara Unit Title: BM 311 Year I Semester Iapi-26524819No ratings yet

- IntroductionDocument18 pagesIntroductionapi-26524819No ratings yet

- Year 2007 2006 2005 2004 2003 Touchwood Investment Limited East West Property Colombo Land CT Land Ceylinco Seylan DevelopmentDocument216 pagesYear 2007 2006 2005 2004 2003 Touchwood Investment Limited East West Property Colombo Land CT Land Ceylinco Seylan Developmentapi-26524819No ratings yet

- Performance Management System 360 Degree FeedbackDocument14 pagesPerformance Management System 360 Degree Feedbackapi-26524819No ratings yet

- What Is Management?: Management Is A Art of Getting Things Done Through PeopleDocument15 pagesWhat Is Management?: Management Is A Art of Getting Things Done Through Peopleapi-26524819No ratings yet

- Term Paper IB002Document5 pagesTerm Paper IB002api-26524819No ratings yet

- JayalalDocument1 pageJayalalapi-26524819No ratings yet

- K.K.J.R.Samarasekera Kumbalmulla, Morahela, Balangoda, Tel: Home - 0455780358 Mobil - 0719492488 ObjectivesDocument3 pagesK.K.J.R.Samarasekera Kumbalmulla, Morahela, Balangoda, Tel: Home - 0455780358 Mobil - 0719492488 Objectivesapi-26524819No ratings yet

- A Credit Risk ModelDocument39 pagesA Credit Risk ModelAnonymous 4gOYyVfdfNo ratings yet

- Financial Crisis 2008Document18 pagesFinancial Crisis 2008Doniyor KarimovNo ratings yet

- 01 Enrollment Agreement - EncryptedDocument7 pages01 Enrollment Agreement - EncryptedCamilla SerpaNo ratings yet

- Analysis of Loans and Advances Provided by IDBI Bank: Vishnu Theerdhan M.S Register Number - 3511210265Document97 pagesAnalysis of Loans and Advances Provided by IDBI Bank: Vishnu Theerdhan M.S Register Number - 3511210265Ramya RNo ratings yet

- Grameen Bank: Bank For The PoorDocument14 pagesGrameen Bank: Bank For The PoorDivyaa R RajaghanthamNo ratings yet

- Draft of Simple Mortgage DeedDocument3 pagesDraft of Simple Mortgage DeedDaniyal Siraj100% (1)

- CP Chapter 2 - 201819 1Document8 pagesCP Chapter 2 - 201819 1Jerome JoseNo ratings yet

- Commercial Banking System and Role of RBI - Assignment June 2021Document6 pagesCommercial Banking System and Role of RBI - Assignment June 2021sadiaNo ratings yet

- Chapter 2 RiskDocument31 pagesChapter 2 Risksolid9283No ratings yet

- The Relationship Between Risks and Company Performance Digi BerhadDocument24 pagesThe Relationship Between Risks and Company Performance Digi BerhadPutri FakhiraNo ratings yet

- Credit Risk Management Practice in Private Banks Case Study Bank of AbyssiniaDocument85 pagesCredit Risk Management Practice in Private Banks Case Study Bank of AbyssiniaamogneNo ratings yet

- BPI Direct Savings Bank A Case StudyDocument30 pagesBPI Direct Savings Bank A Case Study김서연No ratings yet

- An Exploratory Data Analysis For Loan Prediction Based On Nature of The ClientsDocument4 pagesAn Exploratory Data Analysis For Loan Prediction Based On Nature of The ClientsKanavNo ratings yet

- Bondholders' Letter To BofA Over Countrywide Loans (Inc. NY Fed)Document14 pagesBondholders' Letter To BofA Over Countrywide Loans (Inc. NY Fed)DealBook50% (2)

- Wri ResearchDocument7 pagesWri ResearchTú Anh NguyễnNo ratings yet

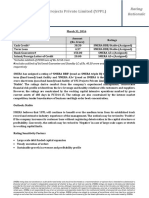

- YFC Projects Private Limited (YPPL) : Rating RationaleDocument2 pagesYFC Projects Private Limited (YPPL) : Rating Rationalelalit rawatNo ratings yet

- The Effect of Credit Card UsageDocument21 pagesThe Effect of Credit Card UsageNoor OsamaNo ratings yet

- Debt Recovery Agency in IndiaDocument22 pagesDebt Recovery Agency in Indiarecreatecredit CollectionsNo ratings yet

- Affin Home Flexi Plus: Product Disclosure SheetDocument6 pagesAffin Home Flexi Plus: Product Disclosure SheetPoi 3647No ratings yet

- Mortgage Key Facts SheetDocument2 pagesMortgage Key Facts Sheetpeter_martin9335No ratings yet

- Abdisalan Duale ProjectDocument65 pagesAbdisalan Duale ProjectLevi Kipkosgei WNo ratings yet

- Moodys - Sample Questions 1Document12 pagesMoodys - Sample Questions 1iva100% (2)

- Chap 3 Co-Ops in The Community RevisedDocument10 pagesChap 3 Co-Ops in The Community RevisediherrmanNo ratings yet

- How To Create A New Order in Agrigenome LIMS 2.1.28july2020Document7 pagesHow To Create A New Order in Agrigenome LIMS 2.1.28july2020raj kumarNo ratings yet

- The Role of Microfinance Bank On Small Scale EnterpriseDocument5 pagesThe Role of Microfinance Bank On Small Scale EnterpriseKingsley OpeyemiNo ratings yet

- 2 - Practice Assignment (ER - Diagram)Document3 pages2 - Practice Assignment (ER - Diagram)Zain Baig100% (1)

- Notice For Full Redemption of Home Loan: Section I - Mode of PaymentDocument2 pagesNotice For Full Redemption of Home Loan: Section I - Mode of Paymentconnect2rahul4204No ratings yet

- Maybank Credit Cardmembers Are Advised To Completely Understand The Product Term & Conditions Before EnrolmentDocument6 pagesMaybank Credit Cardmembers Are Advised To Completely Understand The Product Term & Conditions Before EnrolmentMr DummyNo ratings yet

- Faya PDF 2 PDFDocument43 pagesFaya PDF 2 PDFRameNo ratings yet

- WelcomeLetter C022100601030822 18 09 23Document3 pagesWelcomeLetter C022100601030822 18 09 23The Cool Telly UpdateNo ratings yet

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Mind over Money: The Psychology of Money and How to Use It BetterFrom EverandMind over Money: The Psychology of Money and How to Use It BetterRating: 4 out of 5 stars4/5 (24)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyFrom EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyRating: 3 out of 5 stars3/5 (1)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsFrom EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsRating: 4.5 out of 5 stars4.5/5 (21)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Buffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsFrom EverandBuffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsRating: 5 out of 5 stars5/5 (1)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistFrom EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistRating: 4 out of 5 stars4/5 (32)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)From EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Rating: 4 out of 5 stars4/5 (5)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)