You might also like

- Account Statement: Transactions ListDocument2 pagesAccount Statement: Transactions Listtawhide_islamicNo ratings yet

- Vishal Mega Mart Private Limited - Company Reports and Balance Sheets - ToflerDocument4 pagesVishal Mega Mart Private Limited - Company Reports and Balance Sheets - ToflerDebolin DeyNo ratings yet

- Crisil Annual Report 2019 PDFDocument256 pagesCrisil Annual Report 2019 PDFYoYoNo ratings yet

- 6 MNTH STMNTDocument22 pages6 MNTH STMNTVikrant VermaNo ratings yet

- Form PDF 337279780310722Document7 pagesForm PDF 337279780310722hitendraNo ratings yet

- Chetna AdhiyaDocument5 pagesChetna AdhiyaVikash MauryaNo ratings yet

- Practical Solution For Issues in ITC Reporting in GSTR-9Document9 pagesPractical Solution For Issues in ITC Reporting in GSTR-9d s p jianNo ratings yet

- Company: IDFC Project Cost Years 2003 2004 2005 2006 2007 2008 2009 2010 ProjectedDocument68 pagesCompany: IDFC Project Cost Years 2003 2004 2005 2006 2007 2008 2009 2010 Projectedsumit_sagarNo ratings yet

- Msme EnterprisesDocument6 pagesMsme EnterprisesRavi Shonam KumarNo ratings yet

- Capsa UnitedDocument12 pagesCapsa Unitedvenkat rajNo ratings yet

- Consumer Information:: Cibil Transunion ScoreDocument4 pagesConsumer Information:: Cibil Transunion ScoreJyothiKumariNo ratings yet

- Consumer Information:: Cibil Transunion ScoreDocument7 pagesConsumer Information:: Cibil Transunion ScoreSamuel ReddyNo ratings yet

- Finova - PD Format Oct 2019Document8 pagesFinova - PD Format Oct 2019Madhusudan ParwalNo ratings yet

- Account Statement: Transactions ListDocument4 pagesAccount Statement: Transactions Listtawhide_islamicNo ratings yet

- KDXP ZBKKJ 7 Awt 49 yDocument15 pagesKDXP ZBKKJ 7 Awt 49 yBharath ANo ratings yet

- SME Application FormDocument12 pagesSME Application FormSomnath DasGuptaNo ratings yet

- Lovepreet SinghDocument10 pagesLovepreet SinghNikhil Visa Services100% (1)

- Matrukrupa Travells: Bunglow No 4, Janta Society, Jamnagar - 361006Document1 pageMatrukrupa Travells: Bunglow No 4, Janta Society, Jamnagar - 361006JIGNA NAKARNo ratings yet

- Crisil - Corporate Presentation: September, 2011Document8 pagesCrisil - Corporate Presentation: September, 2011Sherlynn D'CostaNo ratings yet

- Consumer Base Report GANGANDHARANDocument4 pagesConsumer Base Report GANGANDHARANgangarajathiNo ratings yet

- Detailed Statement: Transactions List - GENESYS PROJECTS & ASSOCIATES PVT LTD (INR) - 629605015958Document4 pagesDetailed Statement: Transactions List - GENESYS PROJECTS & ASSOCIATES PVT LTD (INR) - 629605015958sanjay sharmaNo ratings yet

- Ad AnalysisDocument6 pagesAd Analysisnani reddyNo ratings yet

- Ubi Process Note of Shourya Virat Trading CompanyDocument11 pagesUbi Process Note of Shourya Virat Trading CompanyTripurari KumarNo ratings yet

- Sub.: Annual Report of CRISIL Limited: An CompanyDocument250 pagesSub.: Annual Report of CRISIL Limited: An Companysunil kumarNo ratings yet

- Account Statement: Transactions ListDocument4 pagesAccount Statement: Transactions Listtawhide_islamicNo ratings yet

- Indian Income Tax Return: (Refer Instructions For Eligibility)Document7 pagesIndian Income Tax Return: (Refer Instructions For Eligibility)Yogesh SharmaNo ratings yet

- Cibil GangaDocument3 pagesCibil GangasapankumarNo ratings yet

- Account StatementDocument12 pagesAccount StatementAli RazaNo ratings yet

- H TNB Ga Oy 2 KL I7 CSSDocument15 pagesH TNB Ga Oy 2 KL I7 CSSEVD18I019 NIMMAKAYALA SUMANTH GOURI MANJUNADHNo ratings yet

- MREDHULADocument5 pagesMREDHULAroshith kpNo ratings yet

- (Development of Insurance Sector in India) : A Dissertation Project Report ONDocument53 pages(Development of Insurance Sector in India) : A Dissertation Project Report ONRajesh Kumar roulNo ratings yet

- Acc STMT 833Document26 pagesAcc STMT 833Aishwarya ManoharNo ratings yet

- GSTR2B 20CHSPM6149M1ZS 032023 10062023Document7 pagesGSTR2B 20CHSPM6149M1ZS 032023 10062023laxmi handloommdpNo ratings yet

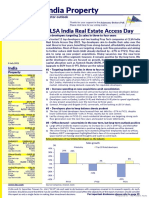

- India Property: CLSA India Real Estate Access DayDocument21 pagesIndia Property: CLSA India Real Estate Access DayManideep KumarNo ratings yet

- Projections - Civil Contractor Material SupplierDocument16 pagesProjections - Civil Contractor Material SupplierRahul LipareNo ratings yet

- Ram Kripal Nishad - PRAT230728CR689051147Document2 pagesRam Kripal Nishad - PRAT230728CR689051147AmanNo ratings yet

- OpMiniStatementUX315 06 2021 PDFDocument1 pageOpMiniStatementUX315 06 2021 PDFsaritaNo ratings yet

- GSTR1 33cfhpd2441a1zb 122022Document4 pagesGSTR1 33cfhpd2441a1zb 122022Prabhu SNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceumesh KumarNo ratings yet

- Account Statement: Transactions ListDocument4 pagesAccount Statement: Transactions Listtawhide_islamicNo ratings yet

- Fixed Deposit AdviceDocument1 pageFixed Deposit Advicemac martinNo ratings yet

- BasixDocument4 pagesBasixcinderella6No ratings yet

- Octa - Financials FY 19-20Document41 pagesOcta - Financials FY 19-20CA Prakash YathamNo ratings yet

- Annexure - 1: Mode of RepaymentDocument2 pagesAnnexure - 1: Mode of RepaymentJaggu NitheshNo ratings yet

- Bureau 90000593499 6071790922Document6 pagesBureau 90000593499 6071790922Pradeep kumar.sNo ratings yet

- Bank Statement1643268941739Document55 pagesBank Statement1643268941739kappilNo ratings yet

- Acct Statement-XX7040-30122022Document93 pagesAcct Statement-XX7040-30122022Gaurav KinholkarNo ratings yet

- Trading & Demat Account Opening Form and Power of Attorney: Application NoDocument52 pagesTrading & Demat Account Opening Form and Power of Attorney: Application Nonirajthacker93620No ratings yet

- Netowrth CertificateDocument3 pagesNetowrth CertificateSai Charan GvNo ratings yet

- Print - Udyam Registration CertificateDocument2 pagesPrint - Udyam Registration CertificateAjit KumarNo ratings yet

- Nykaa - Fundamental Technical AnalysisDocument6 pagesNykaa - Fundamental Technical Analysiskhyati kaulNo ratings yet

- A Study On Correlation Between Indian Stock Indices of BSE and American Stock Indice NASDAQ at Venture Secrurities Ltd.Document68 pagesA Study On Correlation Between Indian Stock Indices of BSE and American Stock Indice NASDAQ at Venture Secrurities Ltd.Mohan kumar K.SNo ratings yet

- Overview of Investment Banking in IndiaDocument8 pagesOverview of Investment Banking in Indiasumit pamechaNo ratings yet

- Acct Statement XX7251 10102022Document14 pagesAcct Statement XX7251 10102022Laba MeherNo ratings yet

- Form 144 CLA-DALALCHI S.A.R.LDocument4 pagesForm 144 CLA-DALALCHI S.A.R.LALOK DHANUKANo ratings yet

- TurnoverDocument7 pagesTurnoverVivek KumarNo ratings yet

- Stocks Investment PortfolioDocument7 pagesStocks Investment PortfolioMaria AleniNo ratings yet

- Itr 1 FormatDocument3 pagesItr 1 FormatPawanNo ratings yet

- Investor Presentation For September 30, 2016 (Company Update)Document64 pagesInvestor Presentation For September 30, 2016 (Company Update)Shyam SunderNo ratings yet

- OLLI ICR 2018 Final - V8Document26 pagesOLLI ICR 2018 Final - V8Ala BasterNo ratings yet

- PK Sinah - Computer FundamentalsDocument536 pagesPK Sinah - Computer FundamentalsAleeza KhanNo ratings yet

- Information Security Guidelines For Insurers-07!04!2017-CleanDocument80 pagesInformation Security Guidelines For Insurers-07!04!2017-CleanabhidadNo ratings yet

- Chain of Custody FormDocument3 pagesChain of Custody FormSanjana Iyer67% (3)

- Project Mutual Fund in IndiaDocument16 pagesProject Mutual Fund in Indiasidhantha94% (31)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsFrom EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsRating: 5 out of 5 stars5/5 (1)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistFrom EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistRating: 4 out of 5 stars4/5 (32)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Other People's Money: The Real Business of FinanceFrom EverandOther People's Money: The Real Business of FinanceRating: 4 out of 5 stars4/5 (34)