You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Code of Professional ResponsibilityDocument9 pagesCode of Professional ResponsibilitybbysheNo ratings yet

- Ja Matthew KangDocument3 pagesJa Matthew KangSannie RemotinNo ratings yet

- RULE 130 Rules of CourtDocument141 pagesRULE 130 Rules of CourtalotcepilloNo ratings yet

- CRUZ (2014) Philippine Political LawDocument1,047 pagesCRUZ (2014) Philippine Political LawSannie RemotinNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument96 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledSannie RemotinNo ratings yet

- Corporation LawDocument181 pagesCorporation LawRodil FlanciaNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument96 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledSannie RemotinNo ratings yet

- PALS Civil ProcedureDocument150 pagesPALS Civil ProcedureLou Corina Lacambra100% (2)

- RULE 130 ReviewerDocument2 pagesRULE 130 ReviewerSannie RemotinNo ratings yet

- 100 Manuel Labor NotesDocument19 pages100 Manuel Labor NotesTricia Aguila-Mudlong100% (1)

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument96 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledSannie RemotinNo ratings yet

- Bar TechniquesDocument11 pagesBar TechniquesolpotNo ratings yet

- RULE 132 Rules of Court - Presentation of EvidenceDocument26 pagesRULE 132 Rules of Court - Presentation of EvidenceSannie RemotinNo ratings yet

- 100 Manuel Labor NotesDocument19 pages100 Manuel Labor NotesTricia Aguila-Mudlong100% (1)

- Excerpts From Effective Bar Review MethodsDocument26 pagesExcerpts From Effective Bar Review MethodsSannie RemotinNo ratings yet

- Books Used by TopnotchersDocument2 pagesBooks Used by TopnotchersSannie RemotinNo ratings yet

- Complete Legal Ethics Case Digests (Canons 7-22)Document119 pagesComplete Legal Ethics Case Digests (Canons 7-22)Franch Galanza89% (27)

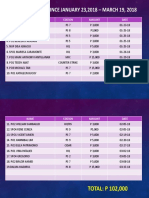

- Assistance Given Since January 23,2018 - March 19, 2018: Name Station Amount DateDocument2 pagesAssistance Given Since January 23,2018 - March 19, 2018: Name Station Amount DateSannie RemotinNo ratings yet

- Vic Mamalateo (Tax Remedies) PDFDocument51 pagesVic Mamalateo (Tax Remedies) PDFMV FadsNo ratings yet

- Endorsement LetterDocument1 pageEndorsement LetterSannie RemotinNo ratings yet

- Vic Mamalateo (Tax Remedies) PDFDocument51 pagesVic Mamalateo (Tax Remedies) PDFMV FadsNo ratings yet

- ReflectionDocument1 pageReflectionSannie RemotinNo ratings yet

- Torts and Damages-ReviewerDocument33 pagesTorts and Damages-Reviewerjhoanna mariekar victoriano84% (37)

- Vic Mamalateo (Tax Remedies) PDFDocument51 pagesVic Mamalateo (Tax Remedies) PDFMV FadsNo ratings yet

- Books Used by TopnotchersDocument2 pagesBooks Used by TopnotchersSannie RemotinNo ratings yet

- Endorsement LetterDocument1 pageEndorsement LetterSannie RemotinNo ratings yet

- Andrew S. Enriquez 0997-663-1077 Sales Representative: Down PaymentDocument1 pageAndrew S. Enriquez 0997-663-1077 Sales Representative: Down PaymentSannie RemotinNo ratings yet

- Zamboanga Adventist CenterDocument3 pagesZamboanga Adventist CenterSannie RemotinNo ratings yet

- Auto Loan RequirementsDocument1 pageAuto Loan RequirementsSannie RemotinNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)