You might also like

- About The MS Regress PackageDocument28 pagesAbout The MS Regress PackagegliptakNo ratings yet

- Applications of Variational Inequalities in Stochastic ControlFrom EverandApplications of Variational Inequalities in Stochastic ControlRating: 2 out of 5 stars2/5 (1)

- Vasicek Model, SimpleDocument28 pagesVasicek Model, SimpleAdela TomaNo ratings yet

- Threshold SlidesDocument6 pagesThreshold SlidesoptoergoNo ratings yet

- About The MS Regression ModelsDocument17 pagesAbout The MS Regression ModelsLars LarsonNo ratings yet

- Panel Data For LearingDocument34 pagesPanel Data For Learingarmailgm100% (1)

- Guided Tour On VAR Innovation Response AnalysisDocument45 pagesGuided Tour On VAR Innovation Response AnalysisrunawayyyNo ratings yet

- Martin Forde - The Real P&LDocument13 pagesMartin Forde - The Real P&LfrancescomaterdonaNo ratings yet

- SVAR Notes: Learn in PersonDocument19 pagesSVAR Notes: Learn in PersonEconometrics FreelancerNo ratings yet

- Uygulama Dersý Soru Ve Cevaplari - 29.11.2011Document6 pagesUygulama Dersý Soru Ve Cevaplari - 29.11.2011Orn PhatthayaphanNo ratings yet

- Structural VAR and Applications: Jean-Paul RenneDocument55 pagesStructural VAR and Applications: Jean-Paul RennerunawayyyNo ratings yet

- Lecture Series 1 Linear Random and Fixed Effect Models and Their (Less) Recent ExtensionsDocument62 pagesLecture Series 1 Linear Random and Fixed Effect Models and Their (Less) Recent ExtensionsDaniel Bogiatzis GibbonsNo ratings yet

- ps8 +fall2013Document6 pagesps8 +fall2013Patrick BensonNo ratings yet

- Wooldridge Session 4Document64 pagesWooldridge Session 4Henry KaweesaNo ratings yet

- An Introduction To Bayesian VAR (BVAR) Models R-EconometricsDocument16 pagesAn Introduction To Bayesian VAR (BVAR) Models R-EconometricseruygurNo ratings yet

- Scholes and Williams (1977)Document19 pagesScholes and Williams (1977)DewiRatihYunusNo ratings yet

- 07 - Lent - Topic 2 - Generalized Method of Moments, Part II - The Linear Model - mw217Document16 pages07 - Lent - Topic 2 - Generalized Method of Moments, Part II - The Linear Model - mw217Daniel Bogiatzis GibbonsNo ratings yet

- Vector Autoregressive Models: T T 1 T 1 P T P T TDocument4 pagesVector Autoregressive Models: T T 1 T 1 P T P T Tmpc.9315970No ratings yet

- Eigenvalues and EigenvectorsDocument12 pagesEigenvalues and EigenvectorsGalih Nugraha100% (1)

- 2 Growth Neoclassical GrowthDocument71 pages2 Growth Neoclassical GrowthPAOLA NELLY ROJAS VALERONo ratings yet

- EUI Working Papers: Department of EconomicsDocument33 pagesEUI Working Papers: Department of Economicsmpc.9315970No ratings yet

- Application of Smooth Transition Autoregressive (STAR) Models For Exchange RateDocument10 pagesApplication of Smooth Transition Autoregressive (STAR) Models For Exchange Ratedecker4449No ratings yet

- Calvo - Staggered Prices in A Utility-Maximizing FrameworkDocument16 pagesCalvo - Staggered Prices in A Utility-Maximizing Frameworkanon_78278064No ratings yet

- MIT14 01SCF11 Final Soln f07Document8 pagesMIT14 01SCF11 Final Soln f07Saad MalikNo ratings yet

- SSRN Id1404905 PDFDocument20 pagesSSRN Id1404905 PDFalexa_sherpyNo ratings yet

- Financial Econometrics 2010-2011Document483 pagesFinancial Econometrics 2010-2011axelkokocur100% (1)

- Xppaut NotesDocument8 pagesXppaut Notescalvk79No ratings yet

- Eco100y5 Tt1 2012f MichaelhoDocument3 pagesEco100y5 Tt1 2012f MichaelhoexamkillerNo ratings yet

- PO310 EWEC2010 PresentationDocument1 pagePO310 EWEC2010 Presentationp2pnow2005100% (1)

- Midterm Question - Time Series Analysis - UpdatedDocument3 pagesMidterm Question - Time Series Analysis - UpdatedAakriti JainNo ratings yet

- Vasicek Model SlidesDocument10 pagesVasicek Model SlidesnikhilkrsinhaNo ratings yet

- Notes Dixit StiglitzDocument9 pagesNotes Dixit StiglitzMasha KovalNo ratings yet

- The Economic Crisis Is A Crisis For Economic Theory ALAN KIRMAN (2010)Document21 pagesThe Economic Crisis Is A Crisis For Economic Theory ALAN KIRMAN (2010)Daniela Cardenas SanchezNo ratings yet

- Threshold Heteroskedastic Models: Jean-Michel ZakoianDocument25 pagesThreshold Heteroskedastic Models: Jean-Michel ZakoianLuis Bautista0% (1)

- FFT CalcDocument21 pagesFFT CalcYusufAdiNNo ratings yet

- Homework 1Document8 pagesHomework 1Andrés García Arce0% (1)

- Using The GRS Test Statistic To Asses Factor Model FitDocument6 pagesUsing The GRS Test Statistic To Asses Factor Model FitAnonymous v9zDTEcgsNo ratings yet

- Game Theory FullDocument65 pagesGame Theory Fullaman jainNo ratings yet

- Generalized Method of Moments (GMM) Estimation: OutlineDocument16 pagesGeneralized Method of Moments (GMM) Estimation: OutlineDione BhaskaraNo ratings yet

- VAR and CointDocument10 pagesVAR and Cointnnnn1234ssssNo ratings yet

- Problem Set 1 Math EconDocument5 pagesProblem Set 1 Math EconEmilio Castillo DintransNo ratings yet

- Lucas - Econometric Policy Evaluation, A CritiqueDocument28 pagesLucas - Econometric Policy Evaluation, A CritiqueFederico Perez CusseNo ratings yet

- Alex Lipton and Artur Sepp - Stochastic Volatility Models and Kelvin WavesDocument27 pagesAlex Lipton and Artur Sepp - Stochastic Volatility Models and Kelvin WavesPlamcfeNo ratings yet

- Vector Auto Regression in Eview IkeDocument37 pagesVector Auto Regression in Eview Ikegbengaode100% (3)

- Homework 5Document5 pagesHomework 5Jean JNo ratings yet

- Dokumen - Tips Cap 3 Bowers 1997 Actuarial Mathematics 2edDocument53 pagesDokumen - Tips Cap 3 Bowers 1997 Actuarial Mathematics 2edSri Jelita PutriNo ratings yet

- State EstimationDocument34 pagesState EstimationFengxing ZhuNo ratings yet

- Regression ChecklistDocument3 pagesRegression ChecklistYixin XiaNo ratings yet

- Econometrics I: TA Session 5: Giovanna UbidaDocument20 pagesEconometrics I: TA Session 5: Giovanna UbidaALAN BUENONo ratings yet

- HJM ModelsDocument9 pagesHJM ModelsGlenden KhewNo ratings yet

- Manual de R StudioDocument6 pagesManual de R StudioendoecaNo ratings yet

- Stability Analysis of Four Bar Mechanism. Part IDocument9 pagesStability Analysis of Four Bar Mechanism. Part IRizkyArmanNo ratings yet

- Pushdown Automata Simulator: Bachelor ThesisDocument29 pagesPushdown Automata Simulator: Bachelor ThesisTaqi ShahNo ratings yet

- Dynamic Programming MethodDocument3 pagesDynamic Programming Methodbobo411No ratings yet

- Background On The Solution of DSGE ModelsDocument7 pagesBackground On The Solution of DSGE ModelsTheBlueBalloonNo ratings yet

- GMM Resume PDFDocument60 pagesGMM Resume PDFdamian camargoNo ratings yet

- Chapter 8Document29 pagesChapter 8jgau0017No ratings yet

- CMSspreads Several MethodDocument9 pagesCMSspreads Several MethodYuan LiNo ratings yet

- Volatility Surface InterpolationDocument24 pagesVolatility Surface InterpolationMickehugoNo ratings yet

- Consistent Pricing of FX Options: Antonio Castagna Fabio Mercurio Banca IMI, MilanDocument18 pagesConsistent Pricing of FX Options: Antonio Castagna Fabio Mercurio Banca IMI, MilanbnsqtradingNo ratings yet

- Dispersion TradesDocument41 pagesDispersion TradesLameune100% (1)

- Commodity Hybrids Trading: James Groves, Barclays CapitalDocument21 pagesCommodity Hybrids Trading: James Groves, Barclays CapitalLameuneNo ratings yet

- Brief Therapy - A Problem Solving Model of ChangeDocument4 pagesBrief Therapy - A Problem Solving Model of ChangeLameuneNo ratings yet

- A Course On Asymptotic Methods, Choice of Model in Regression and CausalityDocument1 pageA Course On Asymptotic Methods, Choice of Model in Regression and CausalityLameuneNo ratings yet

- Butterfly EconomicsDocument5 pagesButterfly EconomicsLameuneNo ratings yet

- Andrea RoncoroniDocument27 pagesAndrea RoncoroniLameuneNo ratings yet

- Tristam ScottDocument24 pagesTristam ScottLameuneNo ratings yet

- Eyde LandDocument54 pagesEyde LandLameuneNo ratings yet

- Network of Options For International Coal & Freight BusinessesDocument20 pagesNetwork of Options For International Coal & Freight BusinessesLameuneNo ratings yet

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDocument44 pagesReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneNo ratings yet

- Day3 Session2B StoneDocument11 pagesDay3 Session2B StoneLameuneNo ratings yet

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDocument44 pagesReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneNo ratings yet

- Pricing Storable Commodities and Associated Derivatives: Dorje C. BrodyDocument32 pagesPricing Storable Commodities and Associated Derivatives: Dorje C. BrodyLameuneNo ratings yet

- Jacob BeharallDocument19 pagesJacob BeharallLameuneNo ratings yet

- Tristam ScottDocument24 pagesTristam ScottLameuneNo ratings yet

- Marcel ProkopczukDocument28 pagesMarcel ProkopczukLameuneNo ratings yet

- Valuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingDocument25 pagesValuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingLameuneNo ratings yet

- Prmia 20111103 NyholmDocument24 pagesPrmia 20111103 NyholmLameuneNo ratings yet

- Day3 Session 2APaulDocument11 pagesDay3 Session 2APaulLameuneNo ratings yet

- Day3 Session 1BSternberg PresentationforWebDocument11 pagesDay3 Session 1BSternberg PresentationforWebLameuneNo ratings yet

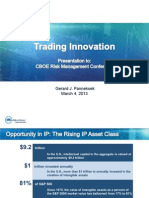

- Gerard J. Pannekoek March 4, 2013Document12 pagesGerard J. Pannekoek March 4, 2013LameuneNo ratings yet

- Day1 Session3 ColeDocument36 pagesDay1 Session3 ColeLameuneNo ratings yet

- Commodities and ETRM PDFDocument4 pagesCommodities and ETRM PDFhquaoNo ratings yet

- TD Ameritrade Free Etf List PDFDocument6 pagesTD Ameritrade Free Etf List PDFjjy1234No ratings yet

- Infostream Q1 23Document26 pagesInfostream Q1 23Ally Bin AssadNo ratings yet

- Back Ground To The Budget 2013-14Document197 pagesBack Ground To The Budget 2013-14The New VisionNo ratings yet

- Alankit Assignments LTD.: Project Report ONDocument84 pagesAlankit Assignments LTD.: Project Report ONmannuNo ratings yet

- The Commodities Futures Modernization Act Pub134Document12 pagesThe Commodities Futures Modernization Act Pub134falungongboy6587No ratings yet

- Finance Project Report On Commodity MarketDocument67 pagesFinance Project Report On Commodity MarketSaket VermaNo ratings yet

- Financial Derivatives Assignment IDocument12 pagesFinancial Derivatives Assignment Iamit_harry100% (3)

- House Hearing, 110TH Congress - Hearing To Review Reauthorization of The Commodity Exchange ActDocument106 pagesHouse Hearing, 110TH Congress - Hearing To Review Reauthorization of The Commodity Exchange ActScribd Government DocsNo ratings yet

- Lecture 025 SBB Super Breaker Block BullishDocument22 pagesLecture 025 SBB Super Breaker Block BullishkaitongjiangNo ratings yet

- 4 - Microsoft PowerPoint - JDC Company ProfileDocument12 pages4 - Microsoft PowerPoint - JDC Company ProfileBill LiNo ratings yet

- 3-Strategies Spreads Guy BowerDocument15 pages3-Strategies Spreads Guy BowerNicoLazaNo ratings yet

- Facts and Fantasies About Commodity Futures Ten Years LaterDocument31 pagesFacts and Fantasies About Commodity Futures Ten Years LaterSoren K. GroupNo ratings yet

- Commodity Derivatives A Guide For Future Practitioners (Paul E Peterson) PDFDocument281 pagesCommodity Derivatives A Guide For Future Practitioners (Paul E Peterson) PDFFabricio SilvaNo ratings yet

- OilAndGasFinancialJournalOctober2008 EnergyTradingRiskManagementDocument24 pagesOilAndGasFinancialJournalOctober2008 EnergyTradingRiskManagementjohnsm2010No ratings yet

- Definition of Silver Etf:: Silver Etfs Which Hold Physical SilverDocument11 pagesDefinition of Silver Etf:: Silver Etfs Which Hold Physical SilverMayur Bhanushali-MangeNo ratings yet

- Master of Science in Commodity TradingDocument2 pagesMaster of Science in Commodity Tradinganwar187No ratings yet

- WP44 FinancialisationDocument60 pagesWP44 FinancialisationBecca SNo ratings yet

- Gold ProjectDocument66 pagesGold Projectmupparaju_975% (4)

- 07 Chapter 2Document30 pages07 Chapter 2anithaivaturi100% (1)

- Introduction To DerivativesDocument9 pagesIntroduction To DerivativesParam ShahNo ratings yet

- Post Harvest Marketing-Commodity Exchanges of The FutureDocument13 pagesPost Harvest Marketing-Commodity Exchanges of The FutureDvaraNo ratings yet

- DerivativesDocument130 pagesDerivativesPavithran ChandarNo ratings yet

- "Employee Motivation": Summer Training Project Report OnDocument33 pages"Employee Motivation": Summer Training Project Report OnAkarshika PandeyNo ratings yet

- Derivatives in India Blackbook Project TYBFM 2015-2016: Download NowDocument20 pagesDerivatives in India Blackbook Project TYBFM 2015-2016: Download NowSanjay KadamNo ratings yet

- Market Liquidity ExplainedDocument5 pagesMarket Liquidity ExplainedAlberto BonuccelliNo ratings yet

- Analysis of Movement of Gold, Silver and Crude Oil PricesDocument70 pagesAnalysis of Movement of Gold, Silver and Crude Oil PricesAbhishek RanaNo ratings yet

- Abhi Final AsbmDocument78 pagesAbhi Final AsbmRaja DubeyNo ratings yet

- SAP Punch & Bend Raw Material PricingDocument14 pagesSAP Punch & Bend Raw Material PricingSatyanarayana MurthyNo ratings yet

- Financial Market & InstrumentDocument73 pagesFinancial Market & InstrumentSoumya ShettyNo ratings yet