You might also like

- Dispersion TradesDocument41 pagesDispersion TradesLameune100% (1)

- 1.1 Homework Solutions PDFDocument4 pages1.1 Homework Solutions PDFhuehuehue123100100% (4)

- Fiitjee AitsDocument23 pagesFiitjee Aitsullasagw100% (6)

- HW 3Document2 pagesHW 3Wikanti Pratiwi0% (1)

- Min-Hsien Chiang: Hsin-Yi Huang Institute of International Business National Cheng Kung UniversityDocument20 pagesMin-Hsien Chiang: Hsin-Yi Huang Institute of International Business National Cheng Kung UniversityJason JawNo ratings yet

- SLV 2010 MerillLynchDocument77 pagesSLV 2010 MerillLynchStone SunNo ratings yet

- Blanchet All MC2QMCDocument17 pagesBlanchet All MC2QMCrokkodscribeNo ratings yet

- The Analysis of Black-Scholes Option Pricing: Wen-Li Tang, Liang-Rong SongDocument5 pagesThe Analysis of Black-Scholes Option Pricing: Wen-Li Tang, Liang-Rong SongDinesh KumarNo ratings yet

- Schwartz97 R TechnicalDocumentDocument7 pagesSchwartz97 R TechnicalDocumentAbhi SuriNo ratings yet

- Equity Smile A Monte-Carlo ApproachDocument2 pagesEquity Smile A Monte-Carlo ApproachSol FernándezNo ratings yet

- Skewed Normal Distribution of Return Assets in Call European Option PricingDocument12 pagesSkewed Normal Distribution of Return Assets in Call European Option PricinghendrikraharjoNo ratings yet

- Entropy Methods For Financial Derivatives: Marco Avellaneda G63.2936.001 Spring Semester 2009Document42 pagesEntropy Methods For Financial Derivatives: Marco Avellaneda G63.2936.001 Spring Semester 2009Arthur DuxNo ratings yet

- Chapter 1 SlidesDocument11 pagesChapter 1 SlidessubpramNo ratings yet

- SOA Exam MFE Flash CardsDocument21 pagesSOA Exam MFE Flash CardsSong Liu100% (2)

- Local Volatility Models - AnkirchnerDocument24 pagesLocal Volatility Models - AnkirchnerjitenparekhNo ratings yet

- Pricing Options Using Monte Carlo Methods: Shariq MohammedDocument14 pagesPricing Options Using Monte Carlo Methods: Shariq MohammedShankar ShankarNo ratings yet

- Calibrate Implied VolDocument37 pagesCalibrate Implied VolALNo ratings yet

- Var PDFDocument40 pagesVar PDFerereredssdfsfdsfNo ratings yet

- Asian Options Under Multiscale Stochastic Volatility: Jean-Pierre Fouque and Chuan-Hsiang HanDocument14 pagesAsian Options Under Multiscale Stochastic Volatility: Jean-Pierre Fouque and Chuan-Hsiang Hanabhishek210585No ratings yet

- Monte Carlo Option Pricing: Victor Podlozhnyuk Mark HarrisDocument15 pagesMonte Carlo Option Pricing: Victor Podlozhnyuk Mark HarrisVishwa ShanikaNo ratings yet

- Statistical Arbitrage With Mean-Reverting Overnight Price Gaps On High-Frequency Data of The S&P 500Document19 pagesStatistical Arbitrage With Mean-Reverting Overnight Price Gaps On High-Frequency Data of The S&P 500James LiuNo ratings yet

- FE - Ch09 Lookback OptionDocument11 pagesFE - Ch09 Lookback OptionIqbal Mochamad AbdurachmanNo ratings yet

- 1 s2.0 S1468121821000857 MainDocument29 pages1 s2.0 S1468121821000857 Maing5v7rm5spmNo ratings yet

- Demand Forecasting InformationDocument66 pagesDemand Forecasting InformationAyush AgarwalNo ratings yet

- Merton's Jump Diffusion Model: Peter Carr (Based On Lecture Notes by Robert Kohn) Bloomberg LP and Courant Institute, NYUDocument13 pagesMerton's Jump Diffusion Model: Peter Carr (Based On Lecture Notes by Robert Kohn) Bloomberg LP and Courant Institute, NYUstehbar9570No ratings yet

- Bayesian Methods in Finance-Nick PolsonDocument38 pagesBayesian Methods in Finance-Nick PolsonIvan CordovaNo ratings yet

- Credit Indices PrimerDocument13 pagesCredit Indices PrimerSanket PatelNo ratings yet

- Measuring Forecast Performance of ARMADocument10 pagesMeasuring Forecast Performance of ARMAAbhaya Kumar SahooNo ratings yet

- Response Spectrum Analysis PDFDocument30 pagesResponse Spectrum Analysis PDFSujay SantraNo ratings yet

- Jacques - On The Hedging Portfolio of Asian OptionsDocument20 pagesJacques - On The Hedging Portfolio of Asian OptionsJustin ChanNo ratings yet

- EE675A Lecture 16Document6 pagesEE675A Lecture 16sachin bhadangNo ratings yet

- FY Lecture2Document15 pagesFY Lecture2mokgokNo ratings yet

- Time Dependent DemandDocument2 pagesTime Dependent DemandIbrahim El SharNo ratings yet

- An Investment Strategy Based On Stochastic Unit Root ModelsDocument8 pagesAn Investment Strategy Based On Stochastic Unit Root ModelsHusain SulemaniNo ratings yet

- Markovian Projection For Equity, Fixed Income, and Credit DynamicsDocument31 pagesMarkovian Projection For Equity, Fixed Income, and Credit DynamicsginovainmonaNo ratings yet

- Discrete Random Variables and Probability DistributionsDocument36 pagesDiscrete Random Variables and Probability DistributionsBeverly PamanNo ratings yet

- Time Series Analysis: Box-Jenkins MethodDocument26 pagesTime Series Analysis: Box-Jenkins Methodपशुपति नाथNo ratings yet

- Lecture 3Document9 pagesLecture 3przemstilNo ratings yet

- Jump Diffusion Models - PrimerDocument3 pagesJump Diffusion Models - PrimerycchiranjeeviNo ratings yet

- Bruno Dupire Slide 1-2Document114 pagesBruno Dupire Slide 1-2Tze ShaoNo ratings yet

- Options Evaluation Using Monte Carlo Simulation Vasile BRĂTIANDocument13 pagesOptions Evaluation Using Monte Carlo Simulation Vasile BRĂTIANISAILA ANAMARIA-CRISTINANo ratings yet

- Econometrics 1 Slide4bDocument26 pagesEconometrics 1 Slide4byingdong liuNo ratings yet

- International Journal of Pure and Applied Mathematics No. 4 2013, 547-555Document10 pagesInternational Journal of Pure and Applied Mathematics No. 4 2013, 547-555jawad HussainNo ratings yet

- Financial Econometrics - Introduction To Realized Variance (PPT 2011)Document19 pagesFinancial Econometrics - Introduction To Realized Variance (PPT 2011)Randomly EmailNo ratings yet

- Comments On ISO 11929:2010Document10 pagesComments On ISO 11929:2010Grant AtoyanNo ratings yet

- DVP MotionDocument42 pagesDVP MotionShabin MuhammedNo ratings yet

- 5-4 Greek LettersDocument30 pages5-4 Greek LettersNainam SeedoyalNo ratings yet

- Valuing Exploration Andproduction ProjectsDocument3 pagesValuing Exploration Andproduction ProjectsSuta VijayaNo ratings yet

- 1705.04780 MatlabDocument49 pages1705.04780 MatlabNoureddineLahouelNo ratings yet

- Convolutional Codes: Cheng-Chi WongDocument25 pagesConvolutional Codes: Cheng-Chi Wongtrungthanhbk01No ratings yet

- VAR Models: Gloria González-RiveraDocument32 pagesVAR Models: Gloria González-RiveraVinko ZaninovićNo ratings yet

- CFP Lecture1Document36 pagesCFP Lecture1Andrei BejenariNo ratings yet

- CourseworkDocument3 pagesCourseworkJohnNo ratings yet

- Fast Narrow Bounds On The Value of Asian OptionsDocument12 pagesFast Narrow Bounds On The Value of Asian OptionsLong TranNo ratings yet

- Local Vol RepDocument16 pagesLocal Vol RepALNo ratings yet

- Rough Volatility 2023 Part 1 HandoutDocument43 pagesRough Volatility 2023 Part 1 HandoutSlakeNo ratings yet

- Ec2 4Document40 pagesEc2 4masudul9islamNo ratings yet

- Chapter 8Document29 pagesChapter 8jgau0017No ratings yet

- Introduction To (Demand) ForecastingDocument39 pagesIntroduction To (Demand) Forecastinggeeths207No ratings yet

- Wystup Fxpricingformulae EqfDocument20 pagesWystup Fxpricingformulae EqfPrac_23No ratings yet

- ARMA ProcessesDocument29 pagesARMA ProcessesVidaup40No ratings yet

- Bs and Montecarlo GenerationDocument5 pagesBs and Montecarlo GenerationFanny NardellaNo ratings yet

- Nonlinear Analysis: Alireza Rahrooh, Scott ShepardDocument5 pagesNonlinear Analysis: Alireza Rahrooh, Scott ShepardAntonio MartinezNo ratings yet

- Mathematical Formulas for Economics and Business: A Simple IntroductionFrom EverandMathematical Formulas for Economics and Business: A Simple IntroductionRating: 4 out of 5 stars4/5 (4)

- Commodity Hybrids Trading: James Groves, Barclays CapitalDocument21 pagesCommodity Hybrids Trading: James Groves, Barclays CapitalLameuneNo ratings yet

- Brief Therapy - A Problem Solving Model of ChangeDocument4 pagesBrief Therapy - A Problem Solving Model of ChangeLameuneNo ratings yet

- A Course On Asymptotic Methods, Choice of Model in Regression and CausalityDocument1 pageA Course On Asymptotic Methods, Choice of Model in Regression and CausalityLameuneNo ratings yet

- Butterfly EconomicsDocument5 pagesButterfly EconomicsLameuneNo ratings yet

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDocument44 pagesReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneNo ratings yet

- Tristam ScottDocument24 pagesTristam ScottLameuneNo ratings yet

- Eyde LandDocument54 pagesEyde LandLameuneNo ratings yet

- Network of Options For International Coal & Freight BusinessesDocument20 pagesNetwork of Options For International Coal & Freight BusinessesLameuneNo ratings yet

- Pricing Storable Commodities and Associated Derivatives: Dorje C. BrodyDocument32 pagesPricing Storable Commodities and Associated Derivatives: Dorje C. BrodyLameuneNo ratings yet

- Day3 Session2B StoneDocument11 pagesDay3 Session2B StoneLameuneNo ratings yet

- Tristam ScottDocument24 pagesTristam ScottLameuneNo ratings yet

- Jacob BeharallDocument19 pagesJacob BeharallLameuneNo ratings yet

- Valuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingDocument25 pagesValuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingLameuneNo ratings yet

- Emmanuel GincbergDocument37 pagesEmmanuel GincbergLameuneNo ratings yet

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDocument44 pagesReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneNo ratings yet

- Marcel ProkopczukDocument28 pagesMarcel ProkopczukLameuneNo ratings yet

- Prmia 20111103 NyholmDocument24 pagesPrmia 20111103 NyholmLameuneNo ratings yet

- Day3 Session 2APaulDocument11 pagesDay3 Session 2APaulLameuneNo ratings yet

- Day3 Session 1BSternberg PresentationforWebDocument11 pagesDay3 Session 1BSternberg PresentationforWebLameuneNo ratings yet

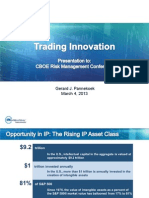

- Gerard J. Pannekoek March 4, 2013Document12 pagesGerard J. Pannekoek March 4, 2013LameuneNo ratings yet

- Day1 Session3 ColeDocument36 pagesDay1 Session3 ColeLameuneNo ratings yet

- Gas Chromatography/Mass Spectrometry Analysis (GC/MS) : Fundamentals and Special TopicsDocument155 pagesGas Chromatography/Mass Spectrometry Analysis (GC/MS) : Fundamentals and Special TopicsDangLuuHaiNo ratings yet

- RPT Add Math Form 5Document9 pagesRPT Add Math Form 5Suziana MohamadNo ratings yet

- Liquid Paint Driers: Standard Specification ForDocument3 pagesLiquid Paint Driers: Standard Specification ForAlvaro Iparraguirre NavarroNo ratings yet

- Validation of Process Gas SystemsDocument6 pagesValidation of Process Gas SystemsJuan Manuel Valdez Von FürthNo ratings yet

- BQUA - Hydranautics CPA5-LD MembraneDocument1 pageBQUA - Hydranautics CPA5-LD MembraneBassemNo ratings yet

- P.A.Hilton LTD Product Data Sheet: HST7 - Deflection of FramesDocument3 pagesP.A.Hilton LTD Product Data Sheet: HST7 - Deflection of FramesramNo ratings yet

- A Guide To Understanding Color CommunicationDocument28 pagesA Guide To Understanding Color CommunicationSeafar YachtingNo ratings yet

- Mid1 Review Solutions PDFDocument4 pagesMid1 Review Solutions PDFRiza AriyaniNo ratings yet

- Modeling of Annular Prediffuser For Marine Gas Turbine Combustor Using CFD - A Study On The Effect of Strut ConfigurationDocument12 pagesModeling of Annular Prediffuser For Marine Gas Turbine Combustor Using CFD - A Study On The Effect of Strut Configurationrajarathnam.kNo ratings yet

- Data Sheet Tr-26 Iecex GBDocument2 pagesData Sheet Tr-26 Iecex GBmkfe2005No ratings yet

- Method 8015dDocument37 pagesMethod 8015dplayerboy111No ratings yet

- Division 3&4 Concrete&MasonryDocument9 pagesDivision 3&4 Concrete&MasonryAceron Torres MalicdanNo ratings yet

- Mechanics of SolidsDocument15 pagesMechanics of Solidsselva1975No ratings yet

- RefrigerationDocument52 pagesRefrigerationRajesh Kumar ChaubeyNo ratings yet

- F23R-A Cili Padi Gas Development Project: Lifting Lugs CalculationDocument4 pagesF23R-A Cili Padi Gas Development Project: Lifting Lugs CalculationCambridge Chin Chian QiaoNo ratings yet

- Unit I MCQ Ii-2Document7 pagesUnit I MCQ Ii-2Kavitha Pasumalaithevan0% (1)

- Course Material For GCFFDocument235 pagesCourse Material For GCFFBeena BNo ratings yet

- D. A. KnowlesDocument7 pagesD. A. Knowlesbiochemist591360No ratings yet

- Revised Affinity LawsDocument13 pagesRevised Affinity Lawsscribdhas2006No ratings yet

- Estimation of Wave Making Resistance by Wave Analysis Ship Wave at SeaDocument11 pagesEstimation of Wave Making Resistance by Wave Analysis Ship Wave at SeaPosei DonNo ratings yet

- Engineering Fracture Mechanics Prof. K. Ramesh Department of Applied Mechanics Indian Institute of Technology, MadrasDocument27 pagesEngineering Fracture Mechanics Prof. K. Ramesh Department of Applied Mechanics Indian Institute of Technology, Madrasferi muhammadNo ratings yet

- Dynamic Matrix Control: Presented by Chinta Manohar D Surya SuvidhaDocument35 pagesDynamic Matrix Control: Presented by Chinta Manohar D Surya SuvidhaManoharChintaNo ratings yet

- ChecalDocument8 pagesChecalmigabraelNo ratings yet

- Differential Equations - MTH401 Special 2006 Assignment 02 SolutionDocument5 pagesDifferential Equations - MTH401 Special 2006 Assignment 02 SolutionDarlene AlforqueNo ratings yet

- Bojan Petkovic-Modeling and Simulation of A Double Pendulum With Pad PDFDocument12 pagesBojan Petkovic-Modeling and Simulation of A Double Pendulum With Pad PDFVeljko MilkovicNo ratings yet