You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Tax Invoice: Gati Kintetsu Express Private LimitedDocument1 pageTax Invoice: Gati Kintetsu Express Private Limitedsibesh nandiNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Print Money ReceiptDocument1 pagePrint Money ReceiptBorshon Bayzid100% (5)

- Acct11 1hwDocument3 pagesAcct11 1hwRonald James Siruno MonisNo ratings yet

- Student Instructions and Worksheets 1Document13 pagesStudent Instructions and Worksheets 1api-4583202030% (1)

- Procurement ProgressDocument1 pageProcurement ProgressPradeep KumarNo ratings yet

- Finished Steel Products Imports - Nov14Document3 pagesFinished Steel Products Imports - Nov14Pradeep KumarNo ratings yet

- NEC Contract For ECC Option ADocument1 pageNEC Contract For ECC Option APradeep KumarNo ratings yet

- Plus TwoDocument1 pagePlus TwoPradeep KumarNo ratings yet

- Start Up Costs CalculatorDocument5 pagesStart Up Costs CalculatorMainul HossainNo ratings yet

- Finished Steel Apparent Consumption - Nov14Document3 pagesFinished Steel Apparent Consumption - Nov14Pradeep KumarNo ratings yet

- Toyota 0.128 General Motors 0.089 Daimler 0.081 Ford 0.078 Others 0.624Document2 pagesToyota 0.128 General Motors 0.089 Daimler 0.081 Ford 0.078 Others 0.624Pradeep KumarNo ratings yet

- Smart City Corporate Price ListDocument2 pagesSmart City Corporate Price ListPradeep KumarNo ratings yet

- Ports in WorldDocument4 pagesPorts in Worldra_mechNo ratings yet

- Ports in WorldDocument4 pagesPorts in Worldra_mechNo ratings yet

- Ports in WorldDocument4 pagesPorts in Worldra_mechNo ratings yet

- Bangalore Urban AgglomerationDocument4 pagesBangalore Urban AgglomerationPradeep KumarNo ratings yet

- Alp Ha 0.6 8 RSFE - Running Sum of Forecast ErrorsDocument3 pagesAlp Ha 0.6 8 RSFE - Running Sum of Forecast ErrorsPradeep KumarNo ratings yet

- Man Power - TenderDocument3 pagesMan Power - TenderPradeep KumarNo ratings yet

- 9 Form HDocument2 pages9 Form HBhaskara RaoNo ratings yet

- Incoterms ChartDocument2 pagesIncoterms ChartPradeep KumarNo ratings yet

- Alpha 0.68 RSFE - Running Sum of Forecast ErrorsDocument3 pagesAlpha 0.68 RSFE - Running Sum of Forecast ErrorsPradeep KumarNo ratings yet

- Alpha 0.68 RSFE - Running Sum of Forecast ErrorsDocument3 pagesAlpha 0.68 RSFE - Running Sum of Forecast ErrorsPradeep KumarNo ratings yet

- Conf Ident IAL: Averages, AlligationDocument2 pagesConf Ident IAL: Averages, AlligationPradeep KumarNo ratings yet

- Form D AbolishedDocument1 pageForm D AbolishedPradeep KumarNo ratings yet

- Subject: - Purchasing of Fire &safety ItemsDocument2 pagesSubject: - Purchasing of Fire &safety ItemsPradeep KumarNo ratings yet

- Custom Duty Calculator - Last YearDocument5 pagesCustom Duty Calculator - Last YearPradeep KumarNo ratings yet

- Custom Duty Calculator - Last YearDocument5 pagesCustom Duty Calculator - Last YearPradeep KumarNo ratings yet

- Swot AnalysisDocument1 pageSwot AnalysisPradeep KumarNo ratings yet

- Custom Duty Calculator - LatestDocument3 pagesCustom Duty Calculator - LatestPradeep KumarNo ratings yet

- Tool Box TalkDocument2 pagesTool Box TalkPradeep KumarNo ratings yet

- How To Conduct Industry AnalysisDocument4 pagesHow To Conduct Industry AnalysisvinaytyNo ratings yet

- Industry AnalysisDocument4 pagesIndustry AnalysisPradeep KumarNo ratings yet

- Sl. No Description Duty % Amount Total DutyDocument2 pagesSl. No Description Duty % Amount Total DutyPradeep KumarNo ratings yet

- Tender For Car DisposalDocument3 pagesTender For Car DisposalPradeep KumarNo ratings yet

- Indicative Taxnet Profile: Personal InformationDocument4 pagesIndicative Taxnet Profile: Personal InformationAbdul WadoodNo ratings yet

- SG Arrival Card - 11sep23Document2 pagesSG Arrival Card - 11sep23maximus_2000No ratings yet

- FullStmt 1678965714873 4220102828520 Arsala04Document43 pagesFullStmt 1678965714873 4220102828520 Arsala04Arsala QasimNo ratings yet

- ThirdPartyRetrieveDocument - Asp 5Document4 pagesThirdPartyRetrieveDocument - Asp 5Elizabeth HilsonNo ratings yet

- COLLECTOR of Internal Revenue vs. Pedro BAUTISTA and David TanDocument1 pageCOLLECTOR of Internal Revenue vs. Pedro BAUTISTA and David TanPouǝllǝ ɐlʎssɐNo ratings yet

- Income-Tax Rules, 1962Document2 pagesIncome-Tax Rules, 1962Abdul SattarNo ratings yet

- Form 510Document6 pagesForm 510Cor LeonisNo ratings yet

- Megahertz Internet Network Pvt. LTD.: Retail InvoiceDocument1 pageMegahertz Internet Network Pvt. LTD.: Retail InvoiceAyush ThapliyalNo ratings yet

- INVOICE Jco PassDocument3 pagesINVOICE Jco PasseldaNo ratings yet

- Jio Fiber InvoiceDocument10 pagesJio Fiber InvoicePiyush Kumar PandeyNo ratings yet

- Tax Receipt Transport Department, Government of West Bengal Registration Authority UTTAR DINAJPUR RTO, West BengalDocument1 pageTax Receipt Transport Department, Government of West Bengal Registration Authority UTTAR DINAJPUR RTO, West BengalSiwam ChoudharyNo ratings yet

- Taxation Bar Examination 2013 Q&ADocument11 pagesTaxation Bar Examination 2013 Q&ADianne Esidera RosalesNo ratings yet

- MyobDocument1 pageMyobAgnes WeaNo ratings yet

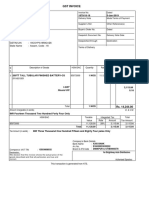

- GST Invoice: Circular Road, Dimapur Nagaland GSTIN/UIN: 13CHIPM1831L1ZC State Name: Nagaland, Code: 13Document1 pageGST Invoice: Circular Road, Dimapur Nagaland GSTIN/UIN: 13CHIPM1831L1ZC State Name: Nagaland, Code: 13Yogesh GuptaNo ratings yet

- Position PaperDocument1 pagePosition PaperAlvy Faith Pel-eyNo ratings yet

- Gmail - Booking Confirmation On IRCTC, Train - 09314, 10-Sep-2021, 2S, LKO - UJNDocument1 pageGmail - Booking Confirmation On IRCTC, Train - 09314, 10-Sep-2021, 2S, LKO - UJNSumitNo ratings yet

- Compost 58000002480Document13 pagesCompost 58000002480prasadNo ratings yet

- Safe Deposit LockerDocument3 pagesSafe Deposit LockerPaul BlessonNo ratings yet

- GROUP 10 (Corporation Income Taxation - Regular Corporation)Document16 pagesGROUP 10 (Corporation Income Taxation - Regular Corporation)Denmark David Gaspar NatanNo ratings yet

- Settlement Payment in Lazada: 1.1 CompanyDocument15 pagesSettlement Payment in Lazada: 1.1 CompanyMinhHuy LêNo ratings yet

- 23 UgsthbDocument84 pages23 UgsthbChawla DimpleNo ratings yet

- 2012 Banking Services RFP - Exhibit Items - Supplement To Exhibit SAP PDFDocument155 pages2012 Banking Services RFP - Exhibit Items - Supplement To Exhibit SAP PDFRajendra PilludaNo ratings yet

- Ministry of Corporate Affairs: Only For Pay Later Payment. Not For Payment at Branch Counter E-Challan For Paying LaterDocument2 pagesMinistry of Corporate Affairs: Only For Pay Later Payment. Not For Payment at Branch Counter E-Challan For Paying LaterPrakashNo ratings yet

- FlexiDocument4 pagesFlexiManish Mani100% (1)

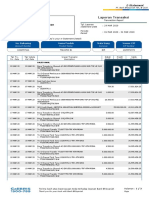

- Laporan Transaksi: No. Rekening Nama Produk Mata Uang Nomor CIFDocument3 pagesLaporan Transaksi: No. Rekening Nama Produk Mata Uang Nomor CIFAlfiIchaNo ratings yet

- Nothing Phone (1) (Black, 128 GB) : Grand Total 27009.00Document1 pageNothing Phone (1) (Black, 128 GB) : Grand Total 27009.00Rehan KahnNo ratings yet