You might also like

- Objectives and Principles of Taxation - GeeksforGeeksDocument5 pagesObjectives and Principles of Taxation - GeeksforGeeksLMRP2 LMRP2No ratings yet

- Tax System: KPMG's Questionable Tax Shelters Ethics CaseDocument15 pagesTax System: KPMG's Questionable Tax Shelters Ethics CaseWriting OnlineNo ratings yet

- The Case For A Progressive Tax: From Basic Research To Policy RecommendationsDocument27 pagesThe Case For A Progressive Tax: From Basic Research To Policy Recommendationsbaapuu5695No ratings yet

- Tax Policy PrimerDocument4 pagesTax Policy PrimerFrancis ChikombolaNo ratings yet

- Taxation, Individual Actions, and Economic Prosperity: A Review by Joshua Rauh and Gregory KearneyDocument12 pagesTaxation, Individual Actions, and Economic Prosperity: A Review by Joshua Rauh and Gregory KearneyHoover InstitutionNo ratings yet

- How America was Tricked on Tax Policy: Secrets and Undisclosed PracticesFrom EverandHow America was Tricked on Tax Policy: Secrets and Undisclosed PracticesNo ratings yet

- Buque - Prelim Exam-Income TaxationDocument3 pagesBuque - Prelim Exam-Income TaxationVillanueva, Jane G.No ratings yet

- Tax Literature ReviewDocument5 pagesTax Literature Reviewc5nr2r46100% (2)

- RITESHDocument94 pagesRITESHRahul RajNo ratings yet

- Who Wins and Who Loses? Debunking 7 Persistent Tax Reform MythsDocument18 pagesWho Wins and Who Loses? Debunking 7 Persistent Tax Reform MythsCenter for American ProgressNo ratings yet

- Tax Policy and the Economy, Volume 36From EverandTax Policy and the Economy, Volume 36Robert A. MoffittNo ratings yet

- Tax Inefficiencies and Alternative SolutionsDocument13 pagesTax Inefficiencies and Alternative SolutionsAbdullahNo ratings yet

- Essay FinalDocument6 pagesEssay FinalHananNo ratings yet

- RITESHDocument94 pagesRITESHrohilla smythNo ratings yet

- Taxes in The United StatesDocument36 pagesTaxes in The United StatesYermekNo ratings yet

- ACT 205 - Tax Theory Practice - Lecture 1Document8 pagesACT 205 - Tax Theory Practice - Lecture 1Kaycia HyltonNo ratings yet

- Escaping True Tax Liability of The Government Amidst PandemicsDocument7 pagesEscaping True Tax Liability of The Government Amidst PandemicsMaria Carla Roan AbelindeNo ratings yet

- Critical Review Paper On TaxDocument4 pagesCritical Review Paper On TaxShannia LouieNo ratings yet

- Taxation SystemDocument16 pagesTaxation SystemShadman ShoumikNo ratings yet

- Govt PoliciesDocument8 pagesGovt PoliciesDanyal TahirNo ratings yet

- Tax Inefficiencies and Alternative SolutionsDocument13 pagesTax Inefficiencies and Alternative SolutionsAbdullahNo ratings yet

- ReadingDocument12 pagesReadinglaraghorbani12No ratings yet

- Taxation Is The ProcessDocument7 pagesTaxation Is The ProcessJaneil FrancisNo ratings yet

- Importance of Tax in EconomyDocument7 pagesImportance of Tax in EconomyAbdul WahabNo ratings yet

- BACC3 - Antiniolos, FaieDocument21 pagesBACC3 - Antiniolos, Faiemochi antiniolosNo ratings yet

- Determinant Factors of Exist Gaps Between The Tax Payers and Tax Authority in Ethiopia, Amhara Region The Case of North Gondar ZoneDocument6 pagesDeterminant Factors of Exist Gaps Between The Tax Payers and Tax Authority in Ethiopia, Amhara Region The Case of North Gondar ZonearcherselevatorsNo ratings yet

- CH 1Document20 pagesCH 1tomas PenuelaNo ratings yet

- Freer Markets Within the Usa: Tax Changes That Make Trade Freer Within the Usa. Phasing-Out Supply-Side Subsidies and Leveling the Playing Field for the Working Person.From EverandFreer Markets Within the Usa: Tax Changes That Make Trade Freer Within the Usa. Phasing-Out Supply-Side Subsidies and Leveling the Playing Field for the Working Person.No ratings yet

- Tax Policy Research Paper TopicsDocument4 pagesTax Policy Research Paper Topicsfzmgp96k100% (1)

- Taxation IssuesDocument23 pagesTaxation IssuesBianca Jane GaayonNo ratings yet

- TaxationDocument34 pagesTaxationShyamKumarKCNo ratings yet

- Demooji Tax in PracticeDocument2 pagesDemooji Tax in PracticePao AbuyogNo ratings yet

- Fiscal Policy - Taxation in PakistanDocument21 pagesFiscal Policy - Taxation in Pakistanali mughalNo ratings yet

- This Content Downloaded From 196.191.248.6 On Fri, 06 May 2022 17:05:39 UTCDocument33 pagesThis Content Downloaded From 196.191.248.6 On Fri, 06 May 2022 17:05:39 UTCTahir DestaNo ratings yet

- Theoretical FrameworkDocument14 pagesTheoretical Frameworkfadi786No ratings yet

- Research Paper TaxesDocument6 pagesResearch Paper Taxesyqxvxpwhf100% (1)

- Tax ReformsDocument9 pagesTax ReformsAmreen kousarNo ratings yet

- Tax Policy and the Economy, Volume 35From EverandTax Policy and the Economy, Volume 35Robert A. MoffittNo ratings yet

- Thesis TaxationDocument8 pagesThesis Taxationgjgm36vk100% (2)

- Ch. 14 - Taxes and Government SpendingDocument25 pagesCh. 14 - Taxes and Government SpendingMr RamNo ratings yet

- Developing Consistent Tax Bases For Broad-Based Reform: Fiscal Associates, IncDocument10 pagesDeveloping Consistent Tax Bases For Broad-Based Reform: Fiscal Associates, IncThe Washington PostNo ratings yet

- Federal Tax RevenuesDocument12 pagesFederal Tax RevenuesJOijiewjfNo ratings yet

- Taxation JunaDocument551 pagesTaxation JunaJuna DafaNo ratings yet

- Tax Policies and Its Economic FluctuationsDocument14 pagesTax Policies and Its Economic FluctuationsZubairNo ratings yet

- Day 3 SlidesDocument25 pagesDay 3 SlidesEyob MogesNo ratings yet

- Taxation DiazDocument3 pagesTaxation DiazRyan DiazNo ratings yet

- The Impact of Taxation On The Economic DevelopmentDocument3 pagesThe Impact of Taxation On The Economic DevelopmentppppNo ratings yet

- Ans Taxation 1Document23 pagesAns Taxation 1Priscilla AdebolaNo ratings yet

- University of Rwanda Huye Campus Principle of Taxation Cat Marketing Departiment MPIRANYA Jean Marie Vianney REG NUMBER: 220009329Document5 pagesUniversity of Rwanda Huye Campus Principle of Taxation Cat Marketing Departiment MPIRANYA Jean Marie Vianney REG NUMBER: 220009329gatete samNo ratings yet

- University of Rwanda Huye Campus Principle of Taxation Cat Marketing Departiment MPIRANYA Jean Marie Vianney REG NUMBER: 220009329Document5 pagesUniversity of Rwanda Huye Campus Principle of Taxation Cat Marketing Departiment MPIRANYA Jean Marie Vianney REG NUMBER: 220009329gatete samNo ratings yet

- Tax Evasion and Financial Instability: Peterson K OziliDocument10 pagesTax Evasion and Financial Instability: Peterson K OziliMihaela ApostolNo ratings yet

- Presentation of Taxation - ScribdDocument17 pagesPresentation of Taxation - ScribdAbdellah BelhouariNo ratings yet

- Tax AssignmentDocument6 pagesTax AssignmentCarlos Takudzwa MudzengerereNo ratings yet

- M222994Document5 pagesM222994Carlos Takudzwa MudzengerereNo ratings yet

- Learning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxFrom EverandLearning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxNo ratings yet

- Tax Working Group Briefing PaperDocument20 pagesTax Working Group Briefing PaperbernardchickeyNo ratings yet

- Taxation and Fiscal PoliciesDocument279 pagesTaxation and Fiscal PoliciesFun DietNo ratings yet

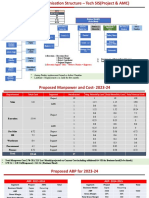

- Proposed Org Chart - Tech SIS.Document5 pagesProposed Org Chart - Tech SIS.Santosh KumarNo ratings yet

- My Record of Group ContributionDocument16 pagesMy Record of Group ContributionMemey C.No ratings yet

- Analysis of Annual Report:: AbstractDocument6 pagesAnalysis of Annual Report:: Abstractapi-301617324No ratings yet

- Cost AccountingDocument47 pagesCost AccountingCarlos John Talania 1923No ratings yet

- Management Theory and PracticesDocument15 pagesManagement Theory and Practicessajidsfa100% (2)

- 11 NIQ Soil Testing PatharkandiDocument2 pages11 NIQ Soil Testing Patharkandiexecutive engineer1No ratings yet

- Bhaichung BhutiyaDocument8 pagesBhaichung BhutiyaPriyankaSinghNo ratings yet

- Islamic Capital Market Malaysia PDFDocument35 pagesIslamic Capital Market Malaysia PDFSyahrul EffendeeNo ratings yet

- Furnmart Furniture Stor1Document5 pagesFurnmart Furniture Stor1Bame SereboloNo ratings yet

- Chapter 9 Accounting Cycle of A Service BusinessDocument59 pagesChapter 9 Accounting Cycle of A Service BusinessArlyn Ragudos BSA1No ratings yet

- Broker Course Syllabus: Florida Real Estate CommissionDocument59 pagesBroker Course Syllabus: Florida Real Estate Commissioni_ara01No ratings yet

- SAN Notification2021Document1 pageSAN Notification2021Ndumiso MagaganeNo ratings yet

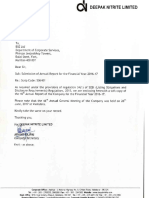

- Deepak NitriteDocument169 pagesDeepak NitriteTejendra PatelNo ratings yet

- A Great Volatility TradeDocument3 pagesA Great Volatility TradeBaljeet SinghNo ratings yet

- Goods & Services Tax (GST) Supply - Time, Place and Value: Concurrent Session 1DDocument23 pagesGoods & Services Tax (GST) Supply - Time, Place and Value: Concurrent Session 1Damighul_saharNo ratings yet

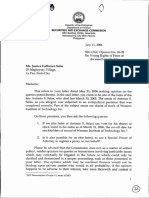

- Republic of The Philippines Department of Finance SEC Building, EDSA, Greenhills Mandaluyong City Metro Manila PhilippinesDocument4 pagesRepublic of The Philippines Department of Finance SEC Building, EDSA, Greenhills Mandaluyong City Metro Manila PhilippinesPaul GeorgeNo ratings yet

- Community and Management Skills TrainingDocument42 pagesCommunity and Management Skills TrainingAdnan AkramNo ratings yet

- GAAP: Understanding It and The 10 Key Principles: U.S. Public Companies Must Follow GAAP For Their Financial StatementsDocument1 pageGAAP: Understanding It and The 10 Key Principles: U.S. Public Companies Must Follow GAAP For Their Financial StatementsThuraNo ratings yet

- Brynn Grey Financial Impact StudyDocument239 pagesBrynn Grey Financial Impact StudyScott FranzNo ratings yet

- Ar 20 Nissan GandharaDocument152 pagesAr 20 Nissan GandharaGravel coNo ratings yet

- Invoice DMXDocument1 pageInvoice DMXNurhadi HadinataNo ratings yet

- Ppe 2016Document40 pagesPpe 2016Benny Wee0% (1)

- Exeter Delinquent Property Tax ListDocument3 pagesExeter Delinquent Property Tax ListseacoastonlineNo ratings yet

- RFP Supply Implementation Maintenance Loan Lifecycle Management System Including Document Management System Early Warning Signals Tender Document PDFDocument220 pagesRFP Supply Implementation Maintenance Loan Lifecycle Management System Including Document Management System Early Warning Signals Tender Document PDFRajatNo ratings yet

- Consolidated Financial Statements - Intercompany Asset TransactionsDocument15 pagesConsolidated Financial Statements - Intercompany Asset TransactionsImran Abdul HamidNo ratings yet

- InvestmentDocument106 pagesInvestmentSujal BedekarNo ratings yet

- 8fe8c95c08fa432b6352Document14 pages8fe8c95c08fa432b6352Harry keenNo ratings yet

- Varanasi - Sugam Darshan - 1121232Document1 pageVaranasi - Sugam Darshan - 1121232raj1602No ratings yet

- Demat Account OpeningDocument8 pagesDemat Account OpeningNivas NowellNo ratings yet

- Testing Your Trading PlanDocument10 pagesTesting Your Trading PlanTyler K. Moore100% (3)