You might also like

- 2012.08.06 Osn - 1800 - R3 - CWDM & DWDMDocument45 pages2012.08.06 Osn - 1800 - R3 - CWDM & DWDMvictoriovegaNo ratings yet

- 100G Coherent Technologies Oriented To Next Generation of ULH Transmission SystemsDocument2 pages100G Coherent Technologies Oriented To Next Generation of ULH Transmission SystemsvictoriovegaNo ratings yet

- Huawei 100G/40G Solution: WDM & Next Generation Optical Networking 21 23 June 2011 Monte Carlo, MonacoDocument22 pagesHuawei 100G/40G Solution: WDM & Next Generation Optical Networking 21 23 June 2011 Monte Carlo, MonacovictoriovegaNo ratings yet

- Huawei DWDM 100G Field TrialDocument3 pagesHuawei DWDM 100G Field TrialvictoriovegaNo ratings yet

- enDocument10 pagesenlololiliNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Moving Object Tracking in Video Using MATLABDocument5 pagesMoving Object Tracking in Video Using MATLABSumeet SauravNo ratings yet

- List of Book - Computer ScienceDocument3 pagesList of Book - Computer Sciencelibranhitesh7889100% (1)

- NEC Aspila Key Telephone Quick GuideDocument12 pagesNEC Aspila Key Telephone Quick GuideNormel UyNo ratings yet

- SH20-9161-0 Document Composition Facility Users Guide Jul78Document391 pagesSH20-9161-0 Document Composition Facility Users Guide Jul78ccchanNo ratings yet

- SNCP ProtectionDocument6 pagesSNCP Protectionhekri100% (2)

- Lenze Servo DriverDocument186 pagesLenze Servo DriverElyNo ratings yet

- RT-flex82 Flexview-9520 Rev.00Document64 pagesRT-flex82 Flexview-9520 Rev.00Gaby Cris100% (2)

- DIY Coil WinderDocument7 pagesDIY Coil WinderWilson F SobrinhoNo ratings yet

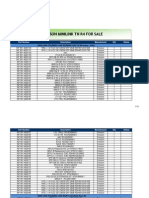

- Ericsson Minilink TN R4Document15 pagesEricsson Minilink TN R4Ebenezer AnnanNo ratings yet

- RK1000 Rockchip PDFDocument57 pagesRK1000 Rockchip PDFsecretobcnNo ratings yet

- Fpga Class 2Document47 pagesFpga Class 2lowtecNo ratings yet

- Narbik NocDocument23 pagesNarbik Nocobee1234No ratings yet

- Acer Aspire 4252/4552/4552G Service GuideDocument178 pagesAcer Aspire 4252/4552/4552G Service GuideKarolMichaelSaavedraContrerasNo ratings yet

- Computer Architecture NoteDocument10 pagesComputer Architecture Notekazi habibaNo ratings yet

- Franklin Electronic Dictionaries 09fdsfDocument6 pagesFranklin Electronic Dictionaries 09fdsfArsalan Arif0% (1)

- Department of Computer Science & Engineering: - + 'KLE Society's KLE Technological University HUBLI-31Document11 pagesDepartment of Computer Science & Engineering: - + 'KLE Society's KLE Technological University HUBLI-31kishorNo ratings yet

- KEYBOARDComputer Keyboard Key ExplanationsDocument9 pagesKEYBOARDComputer Keyboard Key ExplanationsGarg MayankNo ratings yet

- Androidx Class MappingDocument52 pagesAndroidx Class MappingBrittany ZirkleNo ratings yet

- Computer Consumable and Peripherals Prise List: Oxford InfotechDocument4 pagesComputer Consumable and Peripherals Prise List: Oxford Infotechnarendra_bhradiyaNo ratings yet

- Artikel Dan Contoh Soal (Bahasa Inggris)Document15 pagesArtikel Dan Contoh Soal (Bahasa Inggris)BWfool100% (1)

- Capitulo 10 Metodos NumericosDocument42 pagesCapitulo 10 Metodos NumericosMarioAlbertoSimbronNo ratings yet

- lcd 主要参数速查表Document30 pageslcd 主要参数速查表api-3821017100% (1)

- Case Study - (Q & R) - DFC10033 - 1 2021 - 2022Document6 pagesCase Study - (Q & R) - DFC10033 - 1 2021 - 2022lokeshNo ratings yet

- IB Attrition AnalysisDocument121 pagesIB Attrition AnalysisAmeetNo ratings yet

- Assignment of DOSDocument2 pagesAssignment of DOSPravah Shukla100% (1)

- Valeport MIDAS SurveyorDocument1 pageValeport MIDAS SurveyorAndika Yoga RamadanaNo ratings yet

- Sense Point XCD Technical ManualDocument80 pagesSense Point XCD Technical ManualKarina Jimenez VegaNo ratings yet

- Intelligent Block UpconverterDocument196 pagesIntelligent Block UpconverterGeo ThaliathNo ratings yet

- Hitachi Manual - TS5K500.B OEM Specification R18Document176 pagesHitachi Manual - TS5K500.B OEM Specification R18Adrian ScripcaruNo ratings yet

- 10 1 1 26 3120Document18 pages10 1 1 26 3120gonxorNo ratings yet