You might also like

- Cooperative Management Divina Pastora Multi-Purpose Cooperative 1. Organizational ChartDocument5 pagesCooperative Management Divina Pastora Multi-Purpose Cooperative 1. Organizational ChartMa Elaine Christine SantosNo ratings yet

- Lijjat PapadDocument6 pagesLijjat PapadNeeraj SoniNo ratings yet

- Empowering Women in Urban India: Shri Mahila Griha Udyog Lijjat PapadDocument26 pagesEmpowering Women in Urban India: Shri Mahila Griha Udyog Lijjat PapadRohit Kumar Singh100% (1)

- Lijjat-Web PDFDocument8 pagesLijjat-Web PDFAarti CkNo ratings yet

- Women Empowerment by Investment Groups: Nitin Laxman NayseDocument2 pagesWomen Empowerment by Investment Groups: Nitin Laxman Naysedr_kbsinghNo ratings yet

- Kutumb Sakhi Small Scale IndustryDocument13 pagesKutumb Sakhi Small Scale Industryjyotz777No ratings yet

- SHG Research PaperDocument7 pagesSHG Research PaperYerrolla MadhuravaniNo ratings yet

- Animesh Das P40007 Sec-A Cac Assignment: Shri Mahila Griha Udyog Lijjat Papad FormationDocument9 pagesAnimesh Das P40007 Sec-A Cac Assignment: Shri Mahila Griha Udyog Lijjat Papad FormationAnimeshDasNo ratings yet

- Fundraising 7.0 - The Complete Guide To Making Money For Your Organization . . .Starting Right NowFrom EverandFundraising 7.0 - The Complete Guide To Making Money For Your Organization . . .Starting Right NowRating: 4 out of 5 stars4/5 (1)

- SHG Profiles and Study AreaDocument29 pagesSHG Profiles and Study AreaRavi ShankarNo ratings yet

- Case Study EntrepreneurDocument7 pagesCase Study EntrepreneurLICrmdaNo ratings yet

- Transcribed Swayam DR AjitDocument5 pagesTranscribed Swayam DR AjitBonnie FordNo ratings yet

- 18bf0 - Studying Labour Cooperatives With Lijjat PapadDocument8 pages18bf0 - Studying Labour Cooperatives With Lijjat PapadNaresh KumarNo ratings yet

- Janakalyan 2 Annual Report 1998-99Document21 pagesJanakalyan 2 Annual Report 1998-99prasenrNo ratings yet

- 09 Chapter1 PDFDocument34 pages09 Chapter1 PDFAshwini UikeyNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works by Ramit Sethi: Conversation StartersFrom EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works by Ramit Sethi: Conversation StartersRating: 2 out of 5 stars2/5 (7)

- Zingerman's Delicatessen, Ann Arbor, MichiganDocument5 pagesZingerman's Delicatessen, Ann Arbor, MichiganNishtha RahejaNo ratings yet

- SHG & JLGDocument5 pagesSHG & JLGManasi PatilNo ratings yet

- Raising Funds: The Fundraisers Handbook: a Step-By-Step Guide to Maximizing Corporate Giving to NonprofitsFrom EverandRaising Funds: The Fundraisers Handbook: a Step-By-Step Guide to Maximizing Corporate Giving to NonprofitsNo ratings yet

- Class 10 It Unit 4 - Entrepreneurial SkillsDocument6 pagesClass 10 It Unit 4 - Entrepreneurial SkillsTecho omNo ratings yet

- Sri Mahila Griha Udyog Lijjat Papad: Strategic Management CourseDocument23 pagesSri Mahila Griha Udyog Lijjat Papad: Strategic Management CoursePrachit ChaturvediNo ratings yet

- Micro Finance SHG PPT 120928142952 Phpapp01Document30 pagesMicro Finance SHG PPT 120928142952 Phpapp01Aaryan Singh100% (2)

- Chapter 11 Telhana Innasa FileDocument24 pagesChapter 11 Telhana Innasa FilesalasumayyaNo ratings yet

- Addis Ababa Science and Technology University: Assignment 1: Enterpreneurship Individual AssignmentDocument11 pagesAddis Ababa Science and Technology University: Assignment 1: Enterpreneurship Individual AssignmentYabsra kasahun75% (4)

- 975 Project ProposalDocument6 pages975 Project Proposalanwesh pradhanNo ratings yet

- Employability - Skills by Epics Unit 2Document28 pagesEmployability - Skills by Epics Unit 2Epics International CollegeNo ratings yet

- Fundraising for Volunteers: Including the One Secret Key to Fundraising SuccessFrom EverandFundraising for Volunteers: Including the One Secret Key to Fundraising SuccessNo ratings yet

- Tumaini University Dar Es Salaam CollegeDocument7 pagesTumaini University Dar Es Salaam CollegeMoud KhalfaniNo ratings yet

- Strategic Management - LIJJAT NE BACHAI IZZAT CASELETDocument6 pagesStrategic Management - LIJJAT NE BACHAI IZZAT CASELETArti KumariNo ratings yet

- 10-Money and Credit NotesDocument6 pages10-Money and Credit NotesNagulan MadhavanNo ratings yet

- Unit 4 Enterprenur Skill Class 10Document4 pagesUnit 4 Enterprenur Skill Class 10Sian SojNo ratings yet

- Class Notes Class: X Topic: Money and Credit NCERT-Extra Question and Answers (Long Type) Subject: EconomicsDocument6 pagesClass Notes Class: X Topic: Money and Credit NCERT-Extra Question and Answers (Long Type) Subject: EconomicsNsbd DbdbNo ratings yet

- The Wise Guide to Winning Grants: How to Find Funders and Write Winning ProposalsFrom EverandThe Wise Guide to Winning Grants: How to Find Funders and Write Winning ProposalsRating: 2 out of 5 stars2/5 (1)

- Jyoti Project ReportDocument54 pagesJyoti Project ReportAbdul Quadir100% (1)

- Report Proposal City University Banglade PDFDocument10 pagesReport Proposal City University Banglade PDFsamit hossainNo ratings yet

- JuhiDocument1 pageJuhiDakshita DubeyNo ratings yet

- Ljunut 4Document6 pagesLjunut 4Hussein HassanNo ratings yet

- Amalsad CaseDocument16 pagesAmalsad CaseShobhan MeherNo ratings yet

- Unit 4 - Entrepreneurial Skills - EditedDocument8 pagesUnit 4 - Entrepreneurial Skills - Editedggghappy586No ratings yet

- Taniyaaa PFDocument5 pagesTaniyaaa PFNeha GaiNo ratings yet

- Micro Finance and RangdeDocument2 pagesMicro Finance and RangderaghavsarathyNo ratings yet

- How To Form A CooperativeDocument56 pagesHow To Form A CooperativeJanssen SarmientoNo ratings yet

- Basic Practices & Philosophy: Basic Thought Three Golden Rules Philosophy That Guides LijjatDocument3 pagesBasic Practices & Philosophy: Basic Thought Three Golden Rules Philosophy That Guides LijjatNikhil JainNo ratings yet

- Final Lijjat PapadDocument22 pagesFinal Lijjat Papadniteshm4u100% (1)

- The ROI Mindset: How to Raise More Money with the Budget You HaveFrom EverandThe ROI Mindset: How to Raise More Money with the Budget You HaveNo ratings yet

- NegOr Q4 UCSP11 Module7 v2Document12 pagesNegOr Q4 UCSP11 Module7 v2Vanessare Viviene MoralesNo ratings yet

- SHG ProjectDocument26 pagesSHG ProjectShreyaaNo ratings yet

- You Are the Next Billionaire: Stand Up, Think More, Think Bigger Than Yourself, and Have the Will to Self-Lift in BusinessFrom EverandYou Are the Next Billionaire: Stand Up, Think More, Think Bigger Than Yourself, and Have the Will to Self-Lift in BusinessNo ratings yet

- The Quick Wise Guide to Fundraising Readiness: How to Prepare Your Nonprofit to Raise FundsFrom EverandThe Quick Wise Guide to Fundraising Readiness: How to Prepare Your Nonprofit to Raise FundsNo ratings yet

- Research Paper On The Topic Microfinance in AgricultureDocument12 pagesResearch Paper On The Topic Microfinance in AgricultureSukhmander SinghNo ratings yet

- Success In Self-Employment: How to Become Your Own Boss Working from HomeFrom EverandSuccess In Self-Employment: How to Become Your Own Boss Working from HomeNo ratings yet

- FI - Reading 44 - Fundamentals of Credit AnalysisDocument42 pagesFI - Reading 44 - Fundamentals of Credit Analysisshaili shahNo ratings yet

- 2.1. Finance & Financial Statement Analysis by CA Pramod JainDocument69 pages2.1. Finance & Financial Statement Analysis by CA Pramod JainAnjaneyulu SadhuNo ratings yet

- Blockchain AdoptionDocument46 pagesBlockchain AdoptionChima UzombaNo ratings yet

- Accounting For Derivatives and Hedging Activities-Sent2020 PDFDocument38 pagesAccounting For Derivatives and Hedging Activities-Sent2020 PDFTiara Eva TresnaNo ratings yet

- N7Document13 pagesN7Hứa Trí TínNo ratings yet

- GR+XII +Chapter++Test +National+IncomeDocument7 pagesGR+XII +Chapter++Test +National+IncomeAkshatNo ratings yet

- Cuomo Mining Corporation A Public Company Whose Stock Trades On PDFDocument2 pagesCuomo Mining Corporation A Public Company Whose Stock Trades On PDFTaimur TechnologistNo ratings yet

- 2012 Kcse Business Paper 2Document2 pages2012 Kcse Business Paper 2Lubanga JuliusNo ratings yet

- Business Tax - Applicable Business Tax PracticeDocument3 pagesBusiness Tax - Applicable Business Tax PracticeDrew BanlutaNo ratings yet

- Risk Management Solution Chapters Seven-EightDocument9 pagesRisk Management Solution Chapters Seven-EightBombitaNo ratings yet

- Sinclair Company Group Case StudyDocument20 pagesSinclair Company Group Case StudyNida Amri50% (4)

- MBL922N 2013 6 E 1 - TestDocument16 pagesMBL922N 2013 6 E 1 - Testeugene123100% (1)

- Op Transaction History 29!03!2018Document2 pagesOp Transaction History 29!03!2018Avinash GuptaNo ratings yet

- Impacts of Liquidity Ratios On ProfitabilityDocument4 pagesImpacts of Liquidity Ratios On ProfitabilityChaterina ManurungNo ratings yet

- Partnership: Useful LinksDocument15 pagesPartnership: Useful LinkskittuNo ratings yet

- No. 2010-20 July 2010: Receivables (Topic 310)Document92 pagesNo. 2010-20 July 2010: Receivables (Topic 310)LexuzDyNo ratings yet

- Commercial Transportation Working Analysis HDFC Bank - 2011Document72 pagesCommercial Transportation Working Analysis HDFC Bank - 2011rohitkh28No ratings yet

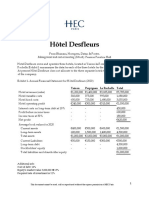

- S07 Desfelurs V3Document2 pagesS07 Desfelurs V3Khushi singhalNo ratings yet

- Banking Allied ServicesDocument11 pagesBanking Allied ServicesSrinivasula Reddy P100% (5)

- WaerDocument13 pagesWaerdasmaguero4lgNo ratings yet

- National Stock ExchangeDocument1 pageNational Stock ExchangeSachin YadavNo ratings yet

- Monno Ceramic ValuationDocument47 pagesMonno Ceramic ValuationMahmudul HassanNo ratings yet

- White PaperDocument11 pagesWhite PaperDavos SavosNo ratings yet

- CMA DataDocument36 pagesCMA DataPramod GuptaNo ratings yet

- FN1584 1622Document445 pagesFN1584 16224207west59thNo ratings yet

- British Council Online Refund Form.Document1 pageBritish Council Online Refund Form.Irene PinedaNo ratings yet

- Beauty Without Cruelty - India: Be Part of Our Movement and Donate NowDocument2 pagesBeauty Without Cruelty - India: Be Part of Our Movement and Donate NowdpfsopfopsfhopNo ratings yet

- Perpetual Help: Calculate Future Value and Present Value of Money andDocument8 pagesPerpetual Help: Calculate Future Value and Present Value of Money andDennis AlbisoNo ratings yet

- CC Auth Form-CompletedDocument1 pageCC Auth Form-CompletedakshayNo ratings yet