You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Name:: Read The PassageDocument1 pageName:: Read The PassageamalNo ratings yet

- Patiala Ki RaoDocument24 pagesPatiala Ki RaoMahavirSinghNo ratings yet

- 2018 ASHRAE® Handbook - Refrigeration (SI Edition) Table: Table 10. Change in Respiration Rates With TimeDocument2 pages2018 ASHRAE® Handbook - Refrigeration (SI Edition) Table: Table 10. Change in Respiration Rates With TimeAlexis AlvarezNo ratings yet

- Detailed Lesson Plan in ScienceDocument4 pagesDetailed Lesson Plan in ScienceJether Marc Palmerola GardoseNo ratings yet

- Afforestation, Reforestation and Forest Restoration in Arid and Semi-Arid TropicsDocument260 pagesAfforestation, Reforestation and Forest Restoration in Arid and Semi-Arid TropicsSergio Serch Alberto LagunesNo ratings yet

- Watershed ManagementDocument9 pagesWatershed ManagementShweta ShrivastavaNo ratings yet

- Design Engineering Workshop - Computer - EngineeringDocument15 pagesDesign Engineering Workshop - Computer - EngineeringsugneshhirparaNo ratings yet

- Laportea Aestuans NPADocument1 pageLaportea Aestuans NPAcandide GbaguidiNo ratings yet

- Export Products and AgricultureDocument31 pagesExport Products and AgricultureTariq Hasan60% (5)

- Analysis of Maize Value Addition Among Entrepreneurs in Taraba State, NigeriaDocument9 pagesAnalysis of Maize Value Addition Among Entrepreneurs in Taraba State, NigeriaIJEAB JournalNo ratings yet

- Snap Hydroponics BrochureDocument2 pagesSnap Hydroponics BrochureEduardson Justo100% (1)

- DAO96-40 (IRR of RA 7940) Pursuant to PD No. 705, as amended, and E.O. No. 192 dated 10 June 1987, and in consonance with the sustainable development thrust of the Government, a Log Control and Monitoring System in the DENR is hereby adopted and the following guidelines are hereby issued for the information of all concerned.Document726 pagesDAO96-40 (IRR of RA 7940) Pursuant to PD No. 705, as amended, and E.O. No. 192 dated 10 June 1987, and in consonance with the sustainable development thrust of the Government, a Log Control and Monitoring System in the DENR is hereby adopted and the following guidelines are hereby issued for the information of all concerned.Mditsa1991100% (4)

- Alwyn H. Gentry, USA - Research - 002 PDFDocument2 pagesAlwyn H. Gentry, USA - Research - 002 PDFKarlos RamirezNo ratings yet

- E5 01A ThemeContentsDocument24 pagesE5 01A ThemeContentsmohammadNo ratings yet

- Groundwork 4 TranslationDocument285 pagesGroundwork 4 TranslationMohamed AzabNo ratings yet

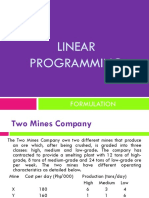

- LINEAR PROGRAMMING Formulation ExampleDocument40 pagesLINEAR PROGRAMMING Formulation ExampleAlyssa Audrey JamonNo ratings yet

- Biotechnology in AquacultureDocument2 pagesBiotechnology in AquacultureNehaNo ratings yet

- Schemes OdishaDocument296 pagesSchemes Odishamahima patraNo ratings yet

- Soil RajeshDocument15 pagesSoil RajeshMir'atun Nissa QuinalendraNo ratings yet

- Hydroponic GardeningDocument12 pagesHydroponic GardeningDilip Sankar Parippay Neelamana100% (1)

- Unit 7: Change and DevelopmentDocument4 pagesUnit 7: Change and DevelopmentIulian ComanNo ratings yet

- Case StudyDocument15 pagesCase StudyJaimell LimNo ratings yet

- San Isidro Farmer's AssociationDocument6 pagesSan Isidro Farmer's Associationauhsoj raluigaNo ratings yet

- Sina Elusakin: (Industrial and General Insurance PLC Nigeria)Document30 pagesSina Elusakin: (Industrial and General Insurance PLC Nigeria)selusakinNo ratings yet

- Presentation 2Document16 pagesPresentation 2Tarun Bhasker ChaniyalNo ratings yet

- B.SC - II Sem IV SyllabusDocument174 pagesB.SC - II Sem IV SyllabusSumit WaghmareNo ratings yet

- Deforestation ReportDocument10 pagesDeforestation ReportElina KarshanovaNo ratings yet

- Activity Sheets in Science Week 8 Quarter 2Document7 pagesActivity Sheets in Science Week 8 Quarter 2Vivian PesadoNo ratings yet

- Strawberry IrrigationDocument5 pagesStrawberry IrrigationrafaelNo ratings yet

- Agam Eco.Document16 pagesAgam Eco.priya19990No ratings yet