You might also like

- Hacking Point of Sale: Payment Application Secrets, Threats, and SolutionsFrom EverandHacking Point of Sale: Payment Application Secrets, Threats, and SolutionsRating: 5 out of 5 stars5/5 (1)

- E-Commerce, E-Banking & EFT: Understanding Digital PaymentsDocument19 pagesE-Commerce, E-Banking & EFT: Understanding Digital Paymentssandhya kumarNo ratings yet

- Evaluation of Some SMS Verification Services and Virtual Credit Cards Services for Online Accounts VerificationsFrom EverandEvaluation of Some SMS Verification Services and Virtual Credit Cards Services for Online Accounts VerificationsRating: 5 out of 5 stars5/5 (1)

- 25-Electronic Fund Peter)Document4 pages25-Electronic Fund Peter)Annonymous963258No ratings yet

- CPC Deposit Account AgreementDocument24 pagesCPC Deposit Account AgreementKassieNo ratings yet

- Electric Funds Transfer PDFDocument93 pagesElectric Funds Transfer PDFlifeisgrand100% (1)

- Deposit Account AgreementDocument23 pagesDeposit Account AgreementarayNo ratings yet

- Money Order Claim Card InstructionsDocument1 pageMoney Order Claim Card InstructionsAddie AyalaNo ratings yet

- Electronic Funds TransferDocument14 pagesElectronic Funds TransferRaj KumarNo ratings yet

- Financial Institution - Borrower: One Thousand One Hundred-Ten Dollars and 10/100Document1 pageFinancial Institution - Borrower: One Thousand One Hundred-Ten Dollars and 10/100MikeDouglas100% (9)

- Check Acceptance Procedure - RevisedDocument4 pagesCheck Acceptance Procedure - RevisedJoe EskenaziNo ratings yet

- US Treasury RegistrationDocument1 pageUS Treasury RegistrationthienvupleikuNo ratings yet

- Lectronic Unds Ransfer: Presented By: Ankit Upadhyay Hina Singh Nisha Singh BhatiDocument21 pagesLectronic Unds Ransfer: Presented By: Ankit Upadhyay Hina Singh Nisha Singh BhatiAnkit UpadhyayNo ratings yet

- Incoming Wire Instructions: Questions?Document2 pagesIncoming Wire Instructions: Questions?Niknjim PoseyNo ratings yet

- Ideposit Merchant ApplicationDocument4 pagesIdeposit Merchant Applicationcris4455No ratings yet

- National Check Fraud Center Lock Box BankingDocument2 pagesNational Check Fraud Center Lock Box Bankingasrinu88881125No ratings yet

- RoutingNumberPolicy PDFDocument8 pagesRoutingNumberPolicy PDFClyde ConeyNo ratings yet

- Checks: Naydud K. Cutipa Roiro Mg. Emerson Angel Espiritu Saenz Interpersonal Communication Accounting Day Iv-ADocument11 pagesChecks: Naydud K. Cutipa Roiro Mg. Emerson Angel Espiritu Saenz Interpersonal Communication Accounting Day Iv-AWilliam Paucar GarciaNo ratings yet

- ACH Quick Guide 0914Document5 pagesACH Quick Guide 0914aplawNo ratings yet

- 24831cashier's Checks: How They Function, Fees, and SecurityDocument2 pages24831cashier's Checks: How They Function, Fees, and Securitygonach7d0e100% (1)

- RemittanceDocument3 pagesRemittanceSalman Abrar100% (2)

- Credit Card NoDocument1 pageCredit Card Noanand4312No ratings yet

- Banking Basics: Types of Bank Accounts, Banker-Customer RelationshipsDocument15 pagesBanking Basics: Types of Bank Accounts, Banker-Customer RelationshipsGurpreet Singh100% (1)

- Consumer Credit Protection Act SummaryDocument203 pagesConsumer Credit Protection Act Summary1stoctop100% (1)

- ACH Wire Request Form From VendorsDocument1 pageACH Wire Request Form From VendorsHarvey BalceNo ratings yet

- Wire Transfer InfoDocument1 pageWire Transfer InfoAleksandr IatsiukNo ratings yet

- Checks ManagementDocument3 pagesChecks ManagementnorthepirNo ratings yet

- EzCheckPrinting Check Writer Allows Customers To Print Checks With Signature and LogoDocument3 pagesEzCheckPrinting Check Writer Allows Customers To Print Checks With Signature and LogoPR.com100% (2)

- Electronic Fund Transfer (EFT)Document27 pagesElectronic Fund Transfer (EFT)Ranjeet Ramaswamy IyerNo ratings yet

- Certified Cheque and Cashier ChequeDocument2 pagesCertified Cheque and Cashier ChequeS K MahapatraNo ratings yet

- Vehicle Loans: List of Documents Required To Be Submitted For Hire Purchase LoanDocument17 pagesVehicle Loans: List of Documents Required To Be Submitted For Hire Purchase LoanDr.K.PadmanabhanNo ratings yet

- Step 1:: Payment Process ProfilesDocument4 pagesStep 1:: Payment Process ProfilesckanadiaNo ratings yet

- Assignment On Payment Methods: Submitted byDocument6 pagesAssignment On Payment Methods: Submitted bySanam ChouhanNo ratings yet

- Promissory Notes - Legal Issues - Foreclosure DefenseDocument21 pagesPromissory Notes - Legal Issues - Foreclosure Defense83jjmack100% (2)

- Instruments of PaymentDocument13 pagesInstruments of Paymentnovelonash100% (4)

- Usps Money OrderDocument4 pagesUsps Money Ordermulibunso67% (3)

- AmexDocument12 pagesAmexMohammad BilalNo ratings yet

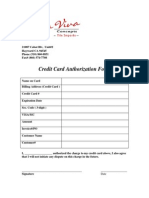

- Auth Form ACH or CC Recurring PaymentDocument2 pagesAuth Form ACH or CC Recurring PaymentAurora BorealissNo ratings yet

- Credit Card RefundsDocument8 pagesCredit Card RefundsthulaseeNo ratings yet

- Cash Transfer MethodsDocument20 pagesCash Transfer MethodsPUNEET MAKHANINo ratings yet

- How Do (Bank) Wire Transfers WorkDocument4 pagesHow Do (Bank) Wire Transfers WorkFaisal KhanNo ratings yet

- Remittance Processing System (RPS)Document7 pagesRemittance Processing System (RPS)Noman DxNo ratings yet

- Telegraphic Transfer GuideDocument12 pagesTelegraphic Transfer GuideBenedict Wong Cheng WaiNo ratings yet

- Credit CardsDocument21 pagesCredit Cardsdixita_chotalia3829100% (1)

- Legitimate Online Payday LoansDocument2 pagesLegitimate Online Payday LoansAnonymous W8y1haNo ratings yet

- CitiDirect Online Banking Bank Handlowy W Warszawie S.A.Document31 pagesCitiDirect Online Banking Bank Handlowy W Warszawie S.A.César OrellanaNo ratings yet

- Bill of Sale and Promissory Note InstructionsDocument10 pagesBill of Sale and Promissory Note InstructionsAngela PattersonNo ratings yet

- Acting As Agent Under A Financial Durable Power of Attorney - An UDocument48 pagesActing As Agent Under A Financial Durable Power of Attorney - An UWayne Ogden100% (1)

- Wire Transfer Procedure PDFDocument7 pagesWire Transfer Procedure PDFombonoNo ratings yet

- Ch10depository Transfer ChecksDocument21 pagesCh10depository Transfer ChecksEfad HafizullahNo ratings yet

- Payment ACH Best GuideDocument66 pagesPayment ACH Best Guidepandian0020% (1)

- Cosigner Addendum ExplainedDocument7 pagesCosigner Addendum ExplainedLinda SmithNo ratings yet

- E ChequeDocument5 pagesE ChequeKaustubh ShilkarNo ratings yet

- Adverse Action NoticeDocument2 pagesAdverse Action NoticeNiko RomeroNo ratings yet

- Lose weight with slimming toe ring voucherDocument3 pagesLose weight with slimming toe ring voucherGlenn GonzagaNo ratings yet

- Checking AccountDocument7 pagesChecking Accountapi-312903607No ratings yet

- 17-Banking Services ProceduresDocument37 pages17-Banking Services ProceduresjayNo ratings yet

- SBI ATM Card To Card Money Transfer Through ATM - Latest InfoDocument8 pagesSBI ATM Card To Card Money Transfer Through ATM - Latest InfoviketjhaNo ratings yet

- Achieve Instant Approval and Issuance of Credit Cards Using Bizagi - NividousDocument1 pageAchieve Instant Approval and Issuance of Credit Cards Using Bizagi - NividousNividousNo ratings yet

- Stealth TechnologyDocument6 pagesStealth TechnologyGaurav KumarNo ratings yet

- Impact of Credit Rating On MsmeDocument11 pagesImpact of Credit Rating On MsmeGaurav KumarNo ratings yet

- GIODocument1 pageGIOGaurav KumarNo ratings yet

- Mahindra Xylo vs Toyota Innova: A Comparison of Key Specs and FeaturesDocument5 pagesMahindra Xylo vs Toyota Innova: A Comparison of Key Specs and FeaturesGaurav KumarNo ratings yet

- Micro Borrowing: Smes - Role of MfisDocument16 pagesMicro Borrowing: Smes - Role of MfisGaurav KumarNo ratings yet

- CREDIT RATING OF MSMEsDocument16 pagesCREDIT RATING OF MSMEsGaurav KumarNo ratings yet

- Zero Ink PrintingDocument3 pagesZero Ink PrintingGaurav KumarNo ratings yet

- Genepax - Water Powered CarDocument2 pagesGenepax - Water Powered CarGaurav Kumar100% (1)

- Future Transport & Green TechnologyDocument17 pagesFuture Transport & Green TechnologyGaurav KumarNo ratings yet

- CASE STUDY - MSMEs Likely To Get 6% of Net Bank CreditDocument15 pagesCASE STUDY - MSMEs Likely To Get 6% of Net Bank CreditGaurav KumarNo ratings yet

- Financial Derivatives & Risk ManagementDocument24 pagesFinancial Derivatives & Risk ManagementGaurav Kumar0% (1)

- Success Story PDFDocument56 pagesSuccess Story PDFhemantmNo ratings yet

- GDP Vs Sensex & NiftyDocument14 pagesGDP Vs Sensex & NiftyGaurav KumarNo ratings yet

- Management of Financial DerivativesDocument35 pagesManagement of Financial DerivativesGaurav Kumar100% (1)

- MFIs & Financial InclusionDocument13 pagesMFIs & Financial InclusionGaurav KumarNo ratings yet

- Micro Financing & Micro BorrowersDocument22 pagesMicro Financing & Micro BorrowersGaurav KumarNo ratings yet

- Credit Gap For Small Scale IndustriesDocument52 pagesCredit Gap For Small Scale IndustriesGaurav KumarNo ratings yet

- Credit Gap For Small Scale IndustriesDocument12 pagesCredit Gap For Small Scale IndustriesGaurav KumarNo ratings yet

- Case Study: The Power of IdeasDocument12 pagesCase Study: The Power of IdeasGaurav KumarNo ratings yet

- Technocrat - EntrepreneurDocument4 pagesTechnocrat - EntrepreneurGaurav Kumar100% (1)

- SME FinancingDocument9 pagesSME FinancingGaurav KumarNo ratings yet

- Micro Small and Medium EnterprisesDocument12 pagesMicro Small and Medium EnterprisesGaurav KumarNo ratings yet

- Small and Medium EnterprisesDocument9 pagesSmall and Medium EnterprisesGaurav KumarNo ratings yet

- Indian EntrepreneurshipDocument10 pagesIndian EntrepreneurshipGaurav KumarNo ratings yet

- Special Provisions Regarding Assessment of FirmDocument5 pagesSpecial Provisions Regarding Assessment of FirmGaurav KumarNo ratings yet

- Blessed Entrepreneur, Do You Hear The Angel's Whisper?Document9 pagesBlessed Entrepreneur, Do You Hear The Angel's Whisper?Gaurav KumarNo ratings yet

- Financial Planning & Tax Management - Section - 115-O of The Indian Income Tax Act, 1961Document8 pagesFinancial Planning & Tax Management - Section - 115-O of The Indian Income Tax Act, 1961Gaurav KumarNo ratings yet

- E Commerce and e BusinessDocument64 pagesE Commerce and e BusinessGaurav Kumar100% (2)

- A Customer - Centric Organization As ADocument30 pagesA Customer - Centric Organization As AGaurav KumarNo ratings yet

- E - BusinessDocument29 pagesE - BusinessGaurav KumarNo ratings yet

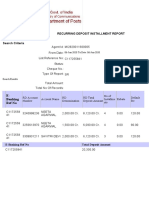

- E-Banking Ref No: Recurring Deposit Installment ReportDocument2 pagesE-Banking Ref No: Recurring Deposit Installment ReportSaurabh JainNo ratings yet

- Untitled DocumentDocument7 pagesUntitled Documentlilieth shayNo ratings yet

- IAB Brand Disruption Report 2023Document59 pagesIAB Brand Disruption Report 2023Carolina GarciaNo ratings yet

- Fintech Wave in IndiaDocument7 pagesFintech Wave in IndiaT ForsythNo ratings yet

- Blue Coat Systems PEPPM Price TemplateDocument152 pagesBlue Coat Systems PEPPM Price TemplateNovian Nur CahyaNo ratings yet

- Bank StatementDocument8 pagesBank Statementvineet kumar4No ratings yet

- Operating Bank AccountsDocument2 pagesOperating Bank AccountsWira KafryawanNo ratings yet

- Icici Bank Makemytrip Platinum Credit CardDocument8 pagesIcici Bank Makemytrip Platinum Credit CardGaurish BandekarNo ratings yet

- Bob Neft RtgsDocument3 pagesBob Neft RtgsTarak M ShahNo ratings yet

- Acct Statement - XX6735 - 18112023Document28 pagesAcct Statement - XX6735 - 18112023Mr קΐメelNo ratings yet

- HDFC Rtgs Neft Form PDF DownloadDocument1 pageHDFC Rtgs Neft Form PDF DownloadJJ JJ0% (1)

- Fintech Regulations in the Philippines: Applying Traditional Laws to Emerging TechnologiesDocument37 pagesFintech Regulations in the Philippines: Applying Traditional Laws to Emerging TechnologiesMike E DmNo ratings yet

- CCBCDocument7 pagesCCBCapi-325149905No ratings yet

- Transaction History: Name: Account Number: Address: Card Number: Reporting Period: EmailDocument2 pagesTransaction History: Name: Account Number: Address: Card Number: Reporting Period: EmailCarybel DiazNo ratings yet

- HDFC Card Dispute FormDocument2 pagesHDFC Card Dispute FormKamini GautamNo ratings yet

- Payment Centers That Authorized To Received University CollectionDocument4 pagesPayment Centers That Authorized To Received University CollectionWilliam Rice100% (2)

- Transaction Report Summary 18.04.21-18.05.21Document4 pagesTransaction Report Summary 18.04.21-18.05.21antonella giulianottiNo ratings yet

- YES Premia Credit Card - User GuideDocument17 pagesYES Premia Credit Card - User Guidesanjay mehtaNo ratings yet

- MICRO ATM TransactionsDocument69 pagesMICRO ATM Transactionsraja choudhuryNo ratings yet

- Account Statement From 18 Feb 2021 To 18 Aug 2021Document3 pagesAccount Statement From 18 Feb 2021 To 18 Aug 2021Abhi PujaraNo ratings yet

- NAIT Program Application Receipt for Digital Media and ITDocument1 pageNAIT Program Application Receipt for Digital Media and ITTasmim Kamal AnaNo ratings yet

- NUR NAHAR'S BANK STATEMENTDocument2 pagesNUR NAHAR'S BANK STATEMENTshahid2opu100% (2)

- Casaviva Credit Card FormDocument1 pageCasaviva Credit Card Formapi-276066920No ratings yet

- Ug Fee VoucherDocument1 pageUg Fee VoucherMALAIKA ALINo ratings yet

- Cardholder service info and account statementDocument6 pagesCardholder service info and account statementbombie bomboxNo ratings yet

- 375 Bob StatementDocument3 pages375 Bob Statementdhaval panchalNo ratings yet

- OpTransactionHistory21 01 2016Document3 pagesOpTransactionHistory21 01 2016venkatesanjsNo ratings yet

- Blockchain and Retail BankingDocument9 pagesBlockchain and Retail BankingMilinbhadeNo ratings yet

- Unified Merchants Api Test Specifications: A Better Way To PayDocument13 pagesUnified Merchants Api Test Specifications: A Better Way To PayAidene EricNo ratings yet

- August Month Current Affairs CapsuleDocument72 pagesAugust Month Current Affairs CapsulevikramadhityaNo ratings yet