You might also like

- Mabeza vs. NLRC labor case rulingDocument12 pagesMabeza vs. NLRC labor case rulingJasmin AlapagNo ratings yet

- Transpo Day 2 CasesDocument7 pagesTranspo Day 2 CasesJasmin AlapagNo ratings yet

- Transpo Day 2 CasesDocument7 pagesTranspo Day 2 CasesJasmin AlapagNo ratings yet

- Chapter VIII Ordinary Asset and Capital AssetsDocument3 pagesChapter VIII Ordinary Asset and Capital AssetsJasmin Alapag100% (2)

- Chapter VIII Ordinary Asset and Capital AssetsDocument3 pagesChapter VIII Ordinary Asset and Capital AssetsJasmin AlapagNo ratings yet

- Transpo Day 1 CasesDocument10 pagesTranspo Day 1 CasesJasmin AlapagNo ratings yet

- NIRC Sections Related To Gross IncomeDocument11 pagesNIRC Sections Related To Gross IncomeJasmin AlapagNo ratings yet

- PERSONS Complete DigestsDocument233 pagesPERSONS Complete DigestsJamie Del CastilloNo ratings yet

- Chapter V1 Cost and Deductions PART IDocument7 pagesChapter V1 Cost and Deductions PART IJasmin AlapagNo ratings yet

- Chapter VIII Ordinary Asset and Capital AssetsDocument3 pagesChapter VIII Ordinary Asset and Capital AssetsJasmin Alapag100% (2)

- Transpo Day 1 CasesDocument10 pagesTranspo Day 1 CasesJasmin AlapagNo ratings yet

- Chapter V1 Cost and Deductions PART IDocument8 pagesChapter V1 Cost and Deductions PART IJasmin AlapagNo ratings yet

- Chapter IX Accounting Method, Periods and Filing of ITRDocument4 pagesChapter IX Accounting Method, Periods and Filing of ITRJasmin AlapagNo ratings yet

- Chapter VIII Ordinary Asset and Capital AssetsDocument3 pagesChapter VIII Ordinary Asset and Capital AssetsJasmin AlapagNo ratings yet

- Chapter IX Accounting Method, Periods and Filing of ITRDocument4 pagesChapter IX Accounting Method, Periods and Filing of ITRJasmin AlapagNo ratings yet

- Tax Chapter 7Document5 pagesTax Chapter 7Jasmin AlapagNo ratings yet

- Chapter V1 Cost and Deductions PART IDocument7 pagesChapter V1 Cost and Deductions PART IJasmin AlapagNo ratings yet

- Chapter IX Accounting Method, Periods and Filing of ITRDocument4 pagesChapter IX Accounting Method, Periods and Filing of ITRJasmin AlapagNo ratings yet

- Cover SheetDocument1 pageCover SheetJasmin AlapagNo ratings yet

- Chapter IX Accounting Method, Periods and Filing of ITRDocument4 pagesChapter IX Accounting Method, Periods and Filing of ITRJasmin AlapagNo ratings yet

- Chapter IV Gross Income NotesDocument5 pagesChapter IV Gross Income NotesJasmin AlapagNo ratings yet

- Tax Rates Effective January 1, 1998 Up To PresentDocument8 pagesTax Rates Effective January 1, 1998 Up To PresentJasmin AlapagNo ratings yet

- Getz 1Document1 pageGetz 1Jasmin AlapagNo ratings yet

- A. What Is A "Common Carrier"?Document26 pagesA. What Is A "Common Carrier"?Jasmin AlapagNo ratings yet

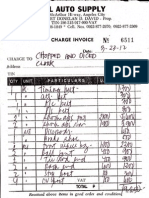

- Chopped and Diced Hot Rod Shop, Inc. Clark Freeport ZoneDocument6 pagesChopped and Diced Hot Rod Shop, Inc. Clark Freeport ZoneJasmin AlapagNo ratings yet

- Legal Brief For Assignment 2.docx Rev3Document5 pagesLegal Brief For Assignment 2.docx Rev3Jasmin AlapagNo ratings yet

- HK Tour PackageDocument1 pageHK Tour PackageJasmin AlapagNo ratings yet

- UntitledDocument1 pageUntitledJasmin AlapagNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Alternative Investment Funds: Meaning, Taxation, Regulations & ListDocument7 pagesAlternative Investment Funds: Meaning, Taxation, Regulations & Listsanket karwaNo ratings yet

- BONDSDocument5 pagesBONDSKyrbe Krystel AbalaNo ratings yet

- Micro Small Medium Enterprises PolicyDocument22 pagesMicro Small Medium Enterprises PolicySai PragnaNo ratings yet

- PC Square2307Document3 pagesPC Square2307SirManny ReyesNo ratings yet

- VCICPlayer HandbookDocument17 pagesVCICPlayer HandbookKarma TsheringNo ratings yet

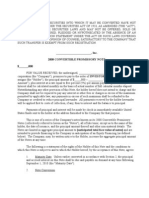

- Generic Convertible NoteDocument8 pagesGeneric Convertible Noteg4nz0100% (1)

- José Rizal's Declaration and Proclamation of The Gift of Love Twitter11.18.18.1Document8 pagesJosé Rizal's Declaration and Proclamation of The Gift of Love Twitter11.18.18.1karen hudes100% (1)

- Ras Gas ProjectDocument12 pagesRas Gas ProjectAritra MandalNo ratings yet

- Pakistan Derivative MarketDocument13 pagesPakistan Derivative MarketPratik ChourasiaNo ratings yet

- The Baby Boomer BustDocument13 pagesThe Baby Boomer BustPeter MaverNo ratings yet

- User Manual For Dealer TerminalDocument64 pagesUser Manual For Dealer TerminalBirender Pal SikandNo ratings yet

- SEBI's Disclosures and Investor Protection Guidelines Explained! Do You FeelDocument2 pagesSEBI's Disclosures and Investor Protection Guidelines Explained! Do You Feelabhisheksh100% (2)

- Financial Services Competency ModelDocument10 pagesFinancial Services Competency ModelDon CamNo ratings yet

- Global Water Intelligence: Volume 5 Issue 4 April 2004Document32 pagesGlobal Water Intelligence: Volume 5 Issue 4 April 2004Aravind NatarajanNo ratings yet

- Barai and Longueuil Arrest PRDocument5 pagesBarai and Longueuil Arrest PRAbsolute ReturnNo ratings yet

- AF301 Final Exam Semester 2, 2014Document8 pagesAF301 Final Exam Semester 2, 2014Anonymous 9dEMgo0No ratings yet

- Ashok Resume NewDocument3 pagesAshok Resume NewVishvajeet DasNo ratings yet

- Maggie Crisis ManagementDocument21 pagesMaggie Crisis ManagementAshif Khan100% (1)

- Tennis Trading The Ultimate GuideDocument32 pagesTennis Trading The Ultimate GuideGabi Luka100% (3)

- Balance Sheet of Shakti PumpsDocument2 pagesBalance Sheet of Shakti PumpsAnonymous 3OudFL5xNo ratings yet

- Financial Management and Financial ObjectivesDocument78 pagesFinancial Management and Financial Objectivesnico_777No ratings yet

- Alternate Investment FundsDocument5 pagesAlternate Investment FundsJhansi DevarasettyNo ratings yet

- Ratio AnalysisDocument51 pagesRatio AnalysisSeema RahulNo ratings yet

- Zerify Answer To ComplaintDocument27 pagesZerify Answer To ComplaintYTOLeaderNo ratings yet

- Question Paper Code:: Reg. No.Document12 pagesQuestion Paper Code:: Reg. No.Saravana KumarNo ratings yet

- NPAs and SecuritizationDocument18 pagesNPAs and SecuritizationVikku AgarwalNo ratings yet

- Green Shoe OptionDocument15 pagesGreen Shoe OptionNadeem Ahmad100% (1)

- Wortham LabsDocument2 pagesWortham LabsDan LehrNo ratings yet

- Basic Financial StatementsDocument14 pagesBasic Financial StatementssajjadNo ratings yet

- Advanced Battery Technologies, Inc.: Here HereDocument35 pagesAdvanced Battery Technologies, Inc.: Here HerePrescienceIGNo ratings yet