You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Administrative Agencies - The Fourth Branch of GovernmentDocument10 pagesAdministrative Agencies - The Fourth Branch of Governmentsleepysalsa100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- False Flag OperationsDocument3 pagesFalse Flag OperationssleepysalsaNo ratings yet

- Al Hikam DetailsDocument11 pagesAl Hikam DetailsArif Hussain ShaikhNo ratings yet

- INS 22 Chapter 07Document10 pagesINS 22 Chapter 07dona007100% (1)

- Pas 10 - Events After The Reporting PeriodDocument11 pagesPas 10 - Events After The Reporting PeriodBritnys Nim100% (1)

- Self-Liquidating Inventory Loan: Rose - Chapter 17 #1Document37 pagesSelf-Liquidating Inventory Loan: Rose - Chapter 17 #1Lê Chấn PhongNo ratings yet

- Problem-Reaction-Solution (The Hegalian Dialectic)Document2 pagesProblem-Reaction-Solution (The Hegalian Dialectic)sleepysalsaNo ratings yet

- Business Finance ABM StrandDocument107 pagesBusiness Finance ABM StrandMiss Anonymous23No ratings yet

- Warfare StateDocument4 pagesWarfare StatesleepysalsaNo ratings yet

- Incrementalization: July 8, 2012Document2 pagesIncrementalization: July 8, 2012sleepysalsaNo ratings yet

- Controlled OppositionDocument2 pagesControlled OppositionsleepysalsaNo ratings yet

- Short Questions-Central BankDocument6 pagesShort Questions-Central BanksadNo ratings yet

- GAURAVDocument2 pagesGAURAVGaurav MishraNo ratings yet

- Audit Entry Sheet 2Document43 pagesAudit Entry Sheet 2Charles MarkeyNo ratings yet

- Dissolution of PartnershipsDocument12 pagesDissolution of PartnershipshasithlakashanNo ratings yet

- Americas Voucher Order FormDocument1 pageAmericas Voucher Order FormilirisaiNo ratings yet

- Yap - ACP312 - ULOb - Let's CheckDocument4 pagesYap - ACP312 - ULOb - Let's CheckJunzen Ralph YapNo ratings yet

- NabardDocument9 pagesNabardAbi ElixirNo ratings yet

- Truth in Lending Act-PDIC-FRIADocument14 pagesTruth in Lending Act-PDIC-FRIAKyla DabalmatNo ratings yet

- Trinity College Copy of New Supplier Form Sphera Solutions UK LimitedDocument1 pageTrinity College Copy of New Supplier Form Sphera Solutions UK Limitedsarath6142No ratings yet

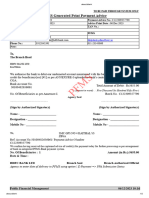

- PFMS Generated Print Payment Advice: To, The Branch HeadDocument2 pagesPFMS Generated Print Payment Advice: To, The Branch HeadAnurag gargNo ratings yet

- Engineering Economics NotesDocument84 pagesEngineering Economics NotesJay Mark CayonteNo ratings yet

- Chapter 3 - Understanding The Income StatementDocument68 pagesChapter 3 - Understanding The Income StatementNguyễn Yến NhiNo ratings yet

- Presentation On Ratio Analysis:: A Case Study On RS Education Solutions PVT - LTDDocument12 pagesPresentation On Ratio Analysis:: A Case Study On RS Education Solutions PVT - LTDEra ChaudharyNo ratings yet

- Loans and Advances of The Sutex Co-Opertive Bank Ltd.Document62 pagesLoans and Advances of The Sutex Co-Opertive Bank Ltd.sumesh8940% (1)

- Banks and The False Dichotomy in The Comparative Political Economy of Finance (Hardie Et Al 2013)Document39 pagesBanks and The False Dichotomy in The Comparative Political Economy of Finance (Hardie Et Al 2013)MarcoKreNo ratings yet

- Notice To The Unit-Holders of The FCP Fund Lyxor Euro Stoxx 50 (DR) UCITS ETFDocument6 pagesNotice To The Unit-Holders of The FCP Fund Lyxor Euro Stoxx 50 (DR) UCITS ETFGeorgio RomaniNo ratings yet

- What Are Commercial BanksDocument3 pagesWhat Are Commercial BanksShyam BahlNo ratings yet

- Fee Statement: Private & ConfidentialDocument256 pagesFee Statement: Private & Confidentialshin kwee farNo ratings yet

- Technical Interview Questions Prepared by Fahad Irfan - PDF Version 1Document4 pagesTechnical Interview Questions Prepared by Fahad Irfan - PDF Version 1Muhammad Khizzar KhanNo ratings yet

- Fee Voucher Fee Voucher Fee Voucher Voucher # 499276 Voucher # 499276 Voucher # 499276Document1 pageFee Voucher Fee Voucher Fee Voucher Voucher # 499276 Voucher # 499276 Voucher # 499276M Irfan IqbalNo ratings yet

- HDFC AMC Case StudyDocument34 pagesHDFC AMC Case StudyGrim ReaperNo ratings yet

- Salisid Berdel John Alexie P Kostka B Module 1 ActivitiesDocument15 pagesSalisid Berdel John Alexie P Kostka B Module 1 ActivitiesBerdel PascoNo ratings yet

- Internship Report of TuhinDocument75 pagesInternship Report of Tuhinratul JiaNo ratings yet

- Goodwill QuestionsDocument7 pagesGoodwill QuestionsTanisha JainNo ratings yet

- D4 - Richard Bulmer and Peter EnglandDocument32 pagesD4 - Richard Bulmer and Peter EnglandmarhadiNo ratings yet