You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

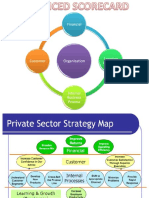

- Balanced Scorecard - Wells Fargo (BUSI0027D) PDFDocument12 pagesBalanced Scorecard - Wells Fargo (BUSI0027D) PDFRafaelKwong50% (4)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Article 41-PFR Case DigestDocument3 pagesArticle 41-PFR Case DigestMary NoveNo ratings yet

- Policy Alternative AssignmentDocument11 pagesPolicy Alternative Assignmentapi-246825887No ratings yet

- Competitor AnalysisDocument4 pagesCompetitor AnalysisRafaelKwong100% (1)

- Management Accounting - Project 1Document7 pagesManagement Accounting - Project 1RafaelKwongNo ratings yet

- McDonald's Advertising and Pricing IIDocument2 pagesMcDonald's Advertising and Pricing IIRafaelKwongNo ratings yet

- Inventory Management of McDonald'sDocument2 pagesInventory Management of McDonald'sRafaelKwongNo ratings yet

- MA Project 2 - McDonaldsDocument11 pagesMA Project 2 - McDonaldsRafaelKwongNo ratings yet

- Budgeted Balance SheetDocument2 pagesBudgeted Balance SheetRafaelKwongNo ratings yet

- Chapter 16 LeadershipDocument18 pagesChapter 16 LeadershipRafaelKwongNo ratings yet

- Mini Interview Instruction SheetDocument2 pagesMini Interview Instruction SheetRafaelKwongNo ratings yet

- Management Accounting Project 2 - D6 (Finalized) PDFDocument20 pagesManagement Accounting Project 2 - D6 (Finalized) PDFRafaelKwongNo ratings yet

- Task Necessity Effectiveness 1. 2. 3Document1 pageTask Necessity Effectiveness 1. 2. 3RafaelKwongNo ratings yet

- Kinky Boots WrittenDocument12 pagesKinky Boots WrittenRafaelKwongNo ratings yet

- New Leaflet Inside ContentDocument1 pageNew Leaflet Inside ContentRafaelKwongNo ratings yet

- PUT UP PetitionDocument2 pagesPUT UP PetitionPartha Sarkar100% (1)

- Introduction To Internal Reconstruction of CompaniesDocument5 pagesIntroduction To Internal Reconstruction of CompaniesIrfan Aijaz100% (1)

- Cambodias Family Trees MedDocument96 pagesCambodias Family Trees MedModelice100% (2)

- Chapter 2 MEC600Document50 pagesChapter 2 MEC600Aziful AiemanNo ratings yet

- Laptop Invoice - GujaratDocument2 pagesLaptop Invoice - GujaratTuShAr DaVENo ratings yet

- 311970536Document1 page311970536Codrut RadantaNo ratings yet

- Declaration in Support of Petition For Rehearing en BancDocument121 pagesDeclaration in Support of Petition For Rehearing en BancNational Organization for MarriageNo ratings yet

- AffidavitDocument2 pagesAffidavitanurag yadavNo ratings yet

- Filipino Society of Composers v. TanDocument6 pagesFilipino Society of Composers v. Tand-fbuser-49417072No ratings yet

- 163 Florentino V FlorentinoDocument2 pages163 Florentino V FlorentinoLouis TanNo ratings yet

- HSRADocument2 pagesHSRAercorsNo ratings yet

- Family Code QDocument14 pagesFamily Code QpapaTAYNo ratings yet

- New Format Rids 1Document4 pagesNew Format Rids 1Aly VNo ratings yet

- Accountability Right Highest Attainable Standard HealthDocument40 pagesAccountability Right Highest Attainable Standard Healthmelicruz14No ratings yet

- DiscoveryDocument11 pagesDiscoveryforam chauhanNo ratings yet

- NAC IACGR 01sep2020 CompressedDocument249 pagesNAC IACGR 01sep2020 CompressedIan Rey BitayNo ratings yet

- Settlement, OAG v. RattnerDocument35 pagesSettlement, OAG v. RattnerLaura NahmiasNo ratings yet

- Modes of DiscoveryDocument7 pagesModes of DiscoveryGlenice JornalesNo ratings yet

- Election Law - Group 1Document36 pagesElection Law - Group 1Abegail Fronteras Buñao100% (1)

- Get List of Lahore Zip CodesDocument3 pagesGet List of Lahore Zip CodesKhu SipNo ratings yet

- Candida Virata vs. Victorio OchoaDocument3 pagesCandida Virata vs. Victorio OchoaKristine KristineeeNo ratings yet

- MB110715 OptDocument54 pagesMB110715 OptVince Bagsit PolicarpioNo ratings yet

- 01 Banda Vs ErmitaDocument38 pages01 Banda Vs ErmitaHerzl Hali V. HermosaNo ratings yet

- Petition 7 of 2018 2Document32 pagesPetition 7 of 2018 2Salimah Nadiah GunneretteNo ratings yet

- PCIB Vs BalmacedaDocument11 pagesPCIB Vs BalmacedaBeverlyn JamisonNo ratings yet

- SMT. - JANKI - DEVI - OTHERS - VS - SHRI - HARISH - CHANDER - CHAWLA Javeed and ShahidDocument20 pagesSMT. - JANKI - DEVI - OTHERS - VS - SHRI - HARISH - CHANDER - CHAWLA Javeed and ShahidsimmionNo ratings yet

- Gaso Transport Services V Obene Ealr 1990-1994 Ea 88Document12 pagesGaso Transport Services V Obene Ealr 1990-1994 Ea 88Tumuhaise Anthony Ferdinand100% (1)

- Planning Commission and NITI AayogDocument5 pagesPlanning Commission and NITI AayogsuprithNo ratings yet