You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- AFC3240 Topic 03 S1 2011Document36 pagesAFC3240 Topic 03 S1 2011sittmoNo ratings yet

- International Parity Relationship: Topic 4Document32 pagesInternational Parity Relationship: Topic 4sittmoNo ratings yet

- AFC3240 NotesDocument18 pagesAFC3240 NotessittmoNo ratings yet

- AFC3240 Topic 06 S1 2011Document27 pagesAFC3240 Topic 06 S1 2011sittmoNo ratings yet

- AFC3240 Topic 09 S1 2011Document17 pagesAFC3240 Topic 09 S1 2011sittmoNo ratings yet

- AFC3240 Topic 08 S1 2011Document24 pagesAFC3240 Topic 08 S1 2011sittmoNo ratings yet

- AFC3240 Topic 07 S1 2011Document12 pagesAFC3240 Topic 07 S1 2011sittmoNo ratings yet

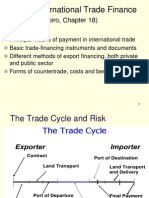

- Topic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)Document15 pagesTopic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)sittmoNo ratings yet

- AFC3240 Topic 01 S2 2010Document18 pagesAFC3240 Topic 01 S2 2010sittmoNo ratings yet

- Determining Exchange Rates Using Balance of Payments and Supply/Demand ModelsDocument27 pagesDetermining Exchange Rates Using Balance of Payments and Supply/Demand ModelssittmoNo ratings yet

- Section 2 Section 2 Intervention in Markets Intervention in MarketsDocument18 pagesSection 2 Section 2 Intervention in Markets Intervention in MarketssittmoNo ratings yet

- Sec 03Document24 pagesSec 03sittmoNo ratings yet

- Sec 04Document32 pagesSec 04sittmoNo ratings yet

- Solving Inhomogenous Recurrence Relations 3Document4 pagesSolving Inhomogenous Recurrence Relations 3sittmoNo ratings yet

- Solving Inhomogenous Recurrence Relations 2Document2 pagesSolving Inhomogenous Recurrence Relations 2sittmoNo ratings yet

- Solving Inhomogenous Recurrence RelationsDocument3 pagesSolving Inhomogenous Recurrence Relationssittmo0% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Victoria Revolutions ManualDocument47 pagesVictoria Revolutions ManualAndrei SoraNo ratings yet

- He Defines Economics As The Science of Choice. It Studies How People Choose To Use Scarce Resources orDocument5 pagesHe Defines Economics As The Science of Choice. It Studies How People Choose To Use Scarce Resources orMarilyn GarciaNo ratings yet

- Novus Customer Service Training AgendaDocument39 pagesNovus Customer Service Training Agendarana1812No ratings yet

- 2021 - Malahayati - An Assessment of The Short-TerDocument23 pages2021 - Malahayati - An Assessment of The Short-TerAnand Yamani YupitrikaNo ratings yet

- Ecs ExampackDocument103 pagesEcs ExampackCharlize RileyNo ratings yet

- ASTROLOGY BASIC SETUP FOR 10 MIN TRADINGDocument6 pagesASTROLOGY BASIC SETUP FOR 10 MIN TRADINGVijay KumarNo ratings yet

- Chapter 6 Economics QuizDocument18 pagesChapter 6 Economics QuizCarmz100% (1)

- Fixed Exchange Rate and Flexible Exchange RateDocument10 pagesFixed Exchange Rate and Flexible Exchange RateAnanya456No ratings yet

- Economics PDFDocument38 pagesEconomics PDFUtkarsh TiwariNo ratings yet

- Demand and Supply AnalysisDocument9 pagesDemand and Supply AnalysisManash JRNo ratings yet

- Business Economics: Dr. Augendra BhukuthDocument120 pagesBusiness Economics: Dr. Augendra Bhukuth31Laura Helena Ayu SunardiNo ratings yet

- CFA Level 1 LOS Changes PDFDocument51 pagesCFA Level 1 LOS Changes PDFMohaiminul Islam ShuvraNo ratings yet

- Understanding Supply and Demand Drives Stock PricesDocument69 pagesUnderstanding Supply and Demand Drives Stock PricesIes BécquerNo ratings yet

- Derivation of Aggregate Supply FunctionDocument23 pagesDerivation of Aggregate Supply FunctionDanish KhanNo ratings yet

- Calculate Available to Promise dates in Oracle InventoryDocument10 pagesCalculate Available to Promise dates in Oracle InventoryyounomeNo ratings yet

- The Behavior Of Interest Rates: Group 9: 1/ Huỳnh Nguyễn Hạ Vy 2/ Đoàn Duy Khánh 3/ Nguyễn Đường Phương NgọcDocument40 pagesThe Behavior Of Interest Rates: Group 9: 1/ Huỳnh Nguyễn Hạ Vy 2/ Đoàn Duy Khánh 3/ Nguyễn Đường Phương NgọcNguyễn Đường Phương NgọcNo ratings yet

- BEF1312 Final Exam 2022 S1Document4 pagesBEF1312 Final Exam 2022 S1bonaventure chipetaNo ratings yet

- Foreign Direct Investment and Export Competitiveness: Smruti Ranjan BeheraDocument31 pagesForeign Direct Investment and Export Competitiveness: Smruti Ranjan BeheraTejal MestryNo ratings yet

- ECO202 Practice Test 3 (Ch.3)Document2 pagesECO202 Practice Test 3 (Ch.3)Aly HoudrojNo ratings yet

- MA Economics Annual SystemDocument25 pagesMA Economics Annual Systemmastermind_asia9389No ratings yet

- Internal Assessment Component-1 Section HDocument3 pagesInternal Assessment Component-1 Section HHarsh KandeleNo ratings yet

- Microeconomics For Managers: Demand and Supply Curve ShiftsDocument48 pagesMicroeconomics For Managers: Demand and Supply Curve ShiftsAnkit PandaNo ratings yet

- Agricultural Licensure Examination ReviewerDocument31 pagesAgricultural Licensure Examination ReviewerRuebenson Acabal100% (13)

- Managerial Economics - PT 2015Document4 pagesManagerial Economics - PT 2015Samvid JhinganNo ratings yet

- Revision For GCSE Economics Section 2 PDFDocument4 pagesRevision For GCSE Economics Section 2 PDFelia khowajaNo ratings yet

- Supply and Demand AnalysisDocument32 pagesSupply and Demand AnalysisAMBWANI NAREN MAHESHNo ratings yet

- Ee Unit 1Document128 pagesEe Unit 1aryanchopra989No ratings yet

- Entrepreneurship: Quarter 1 - Module 7: 1. Branding 2. The Business PlanDocument27 pagesEntrepreneurship: Quarter 1 - Module 7: 1. Branding 2. The Business PlanSheyn RanayNo ratings yet

- DLL Econ Q1WK4 Sy22-23Document11 pagesDLL Econ Q1WK4 Sy22-23AurelynFilomeno-FieldadNo ratings yet