You might also like

- 15Document74 pages15physicsdocs60% (25)

- Rhodes Solutions Ch4Document19 pagesRhodes Solutions Ch4Joson Chai100% (4)

- TrustDocument7 pagesTrustRAVI KABRANo ratings yet

- Form No.10bDocument4 pagesForm No.10bKeith RobbinsNo ratings yet

- Form 10BDocument4 pagesForm 10BCA Vishal ThakkarNo ratings yet

- Form No. 10BDocument3 pagesForm No. 10BLalit PardasaniNo ratings yet

- India Sudar TaxFile 2006-07Document9 pagesIndia Sudar TaxFile 2006-07India Sudar Educational and Charitable TrustNo ratings yet

- Charitable Trust Audit ReportDocument8 pagesCharitable Trust Audit ReportKumar UditNo ratings yet

- Form 15G/15H detailsDocument7 pagesForm 15G/15H detailsKartikey RanaNo ratings yet

- 9 B. S. F.Y. 2014 15Document14 pages9 B. S. F.Y. 2014 15prescongoa.ikigaiNo ratings yet

- Form No. 10Bc: Income-Tax Rules, 1962Document3 pagesForm No. 10Bc: Income-Tax Rules, 1962busuuuNo ratings yet

- SSE Checklist - For - Registration - 02.05.2023Document3 pagesSSE Checklist - For - Registration - 02.05.2023Anuj Kumar SinghNo ratings yet

- Form No. 3aaa (Now Redundant) Audit Report Under Section 32ABDocument4 pagesForm No. 3aaa (Now Redundant) Audit Report Under Section 32ABAnonymous 2evaoXKKdNo ratings yet

- Income Tax Provision For Charitable Trust-1Document106 pagesIncome Tax Provision For Charitable Trust-1Gargi BasuNo ratings yet

- Form 3ad: Audit Report Under Section 33ABADocument3 pagesForm 3ad: Audit Report Under Section 33ABARajshree GuptaNo ratings yet

- 15G FormDocument2 pages15G Formsurendar147No ratings yet

- ITR's and AssessmentDocument11 pagesITR's and Assessmentashutosh4iipmNo ratings yet

- Caro 2003Document10 pagesCaro 2003Aftab KhanNo ratings yet

- Form 3ad: Audit Report Under Section 33ABADocument3 pagesForm 3ad: Audit Report Under Section 33ABAAnonymous 2evaoXKKdNo ratings yet

- India Sudar TaxFile 2009-10Document11 pagesIndia Sudar TaxFile 2009-10India Sudar Educational and Charitable TrustNo ratings yet

- Checklist for Revised Schedule III of Companies ActDocument6 pagesChecklist for Revised Schedule III of Companies ActTony VargheseNo ratings yet

- Priyanka Rajbhar Date 26 02 2024Document6 pagesPriyanka Rajbhar Date 26 02 2024Anshul GuptaNo ratings yet

- Form of Application For DgrantDocument7 pagesForm of Application For DgrantboobhotNo ratings yet

- Annual Return - 2008Document9 pagesAnnual Return - 2008Yashwant KakadeNo ratings yet

- Principle of TaxationDocument7 pagesPrinciple of TaxationAnas YawarNo ratings yet

- Form 10B - Filed FormDocument4 pagesForm 10B - Filed FormcakhaleelassociateshydNo ratings yet

- Trusts- Be eligible to receive CSRDocument6 pagesTrusts- Be eligible to receive CSRCA Amresh VashishtNo ratings yet

- Income Tax Officer Vs Bhojraj Charitable Trust On 13 July 1988Document8 pagesIncome Tax Officer Vs Bhojraj Charitable Trust On 13 July 1988Nithyananda N LNo ratings yet

- India Income Tax Act 1961 11Document8 pagesIndia Income Tax Act 1961 11Dinesh KhandelwalNo ratings yet

- SCHEDULE V - PART II - Annual Return: Form of Annual Return of A Company Having A Share CapitalDocument6 pagesSCHEDULE V - PART II - Annual Return: Form of Annual Return of A Company Having A Share CapitalaaptamilnaduNo ratings yet

- 15 G Form (Blank)Document2 pages15 G Form (Blank)nst27No ratings yet

- Registration Requirements for Valuers in IndiaDocument15 pagesRegistration Requirements for Valuers in Indiagsm.nkl6049No ratings yet

- Taxguru - In-Taxation of CharitableReligious Trust 4Document6 pagesTaxguru - In-Taxation of CharitableReligious Trust 4Ishita FarsaiyaNo ratings yet

- Caro For Chartered AccountantsDocument4 pagesCaro For Chartered AccountantsaakashagarwalNo ratings yet

- Customer Pan Card FormDocument3 pagesCustomer Pan Card FormVishu JoshiNo ratings yet

- Income Tax - Sec 11Document5 pagesIncome Tax - Sec 11Jj018320No ratings yet

- SCHEDULE V - PART II - Annual Return: Form of Annual Return of A Company Having A Share CapitalDocument6 pagesSCHEDULE V - PART II - Annual Return: Form of Annual Return of A Company Having A Share CapitalaaptamilnaduNo ratings yet

- Form No. 3ac: Audit Report Under Section 33ABDocument3 pagesForm No. 3ac: Audit Report Under Section 33ABAnonymous 2evaoXKKdNo ratings yet

- Disclosure No. 2556 2018 Annual Report For Fiscal Year Ended May 31 2018 SEC Form 17 A PDFDocument147 pagesDisclosure No. 2556 2018 Annual Report For Fiscal Year Ended May 31 2018 SEC Form 17 A PDFBeomiNo ratings yet

- 21 Defintions of Income TaxDocument6 pages21 Defintions of Income TaxCA Gourav JashnaniNo ratings yet

- IcplDocument7 pagesIcplDeepak GuptaNo ratings yet

- Approval and Tax Benefits of Non-Profit Organizations in PakistanDocument17 pagesApproval and Tax Benefits of Non-Profit Organizations in PakistanMuhammad HusnainNo ratings yet

- Comtax - Up.nic - in - cSTAct - CST UP Form-1 With AnnexureDocument4 pagesComtax - Up.nic - in - cSTAct - CST UP Form-1 With Annexuresaurabh261050% (2)

- 1 CWF Application FormDocument5 pages1 CWF Application FormShubham Jain ModiNo ratings yet

- Checklist EligibilityDocument2 pagesChecklist EligibilitysmartmumbaiNo ratings yet

- Procedure of Approval of Gratuity Funds Under Income Tax Act, 1961 - Taxguru - inDocument15 pagesProcedure of Approval of Gratuity Funds Under Income Tax Act, 1961 - Taxguru - inJay SharmaNo ratings yet

- TAX - IPCC Amendment For Nov, 2013 Attempt (Carocks - Wordpress.com)Document84 pagesTAX - IPCC Amendment For Nov, 2013 Attempt (Carocks - Wordpress.com)Dushyant SinghaniaNo ratings yet

- Auditors' Report To The Members Of: Sultania Trade PVT - LTDDocument7 pagesAuditors' Report To The Members Of: Sultania Trade PVT - LTDAankit Kumar Jain DugarNo ratings yet

- Annual Return Susruta 2012Document6 pagesAnnual Return Susruta 2012Rajneesh SehgalNo ratings yet

- PAN No.Document5 pagesPAN No.haldharkNo ratings yet

- Form No. 10ccaa: (Now Redundant) Audit Report Under Section 80HHBA of The Income-Tax Act, 1961Document1 pageForm No. 10ccaa: (Now Redundant) Audit Report Under Section 80HHBA of The Income-Tax Act, 1961busuuuNo ratings yet

- CheckList For Application For Managerial RemunerationDocument10 pagesCheckList For Application For Managerial RemunerationspotdealNo ratings yet

- Auditors' Report To The Members of HSCC (India) LTDDocument5 pagesAuditors' Report To The Members of HSCC (India) LTDPraveen KumarNo ratings yet

- format for seeking PSP authorisationDocument20 pagesformat for seeking PSP authorisationHitesh MishraNo ratings yet

- Calculating Net Taxable Salary IncomeDocument6 pagesCalculating Net Taxable Salary IncomeShital PujaraNo ratings yet

- Audit under Fiscal Laws: Key SectionsDocument17 pagesAudit under Fiscal Laws: Key SectionsabhiNo ratings yet

- Planning & EstateDocument5 pagesPlanning & Estatebhaw_shNo ratings yet

- InformationBookletonAIR 11072008Document13 pagesInformationBookletonAIR 11072008Santhosh Kumar BaswaNo ratings yet

- 6 MarksDocument17 pages6 Marksjoy parimalaNo ratings yet

- IncomeTax Short QuestionsDocument7 pagesIncomeTax Short QuestionsWatsun ArmstrongNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- DeedDocument1 pageDeedcachandhiranNo ratings yet

- Serial - No Name - of - Seller Seller - TIN Commodity - Invoice - No Invoice - DateDocument11 pagesSerial - No Name - of - Seller Seller - TIN Commodity - Invoice - No Invoice - DatecachandhiranNo ratings yet

- Murugu and Co: 5 Sakthi Complex Cutcherry Street, Erode, Tamil Nadu 638001 7010641977Document1 pageMurugu and Co: 5 Sakthi Complex Cutcherry Street, Erode, Tamil Nadu 638001 7010641977cachandhiranNo ratings yet

- Sample BillDocument1 pageSample BillcachandhiranNo ratings yet

- Nila Purchases GSTDocument11 pagesNila Purchases GSTcachandhiranNo ratings yet

- Authorisation Letter Ilovepdf CompressedDocument2 pagesAuthorisation Letter Ilovepdf CompressedcachandhiranNo ratings yet

- E WAY BILL 11Document1 pageE WAY BILL 11cachandhiranNo ratings yet

- Deed CompressPdfDocument1 pageDeed CompressPdfcachandhiranNo ratings yet

- APPLICATIONDocument3 pagesAPPLICATIONcachandhiranNo ratings yet

- Form GST REG-06: Government of IndiaDocument3 pagesForm GST REG-06: Government of IndiacachandhiranNo ratings yet

- 2EWBDocument1 page2EWBcachandhiranNo ratings yet

- Bank StatementDocument1 pageBank StatementcachandhiranNo ratings yet

- Challan 1Document1 pageChallan 1cachandhiranNo ratings yet

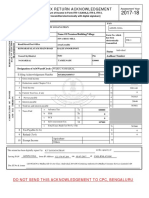

- Indian Income Tax Return Acknowledgement: Name of Premises/Building/VillageDocument1 pageIndian Income Tax Return Acknowledgement: Name of Premises/Building/VillagecachandhiranNo ratings yet

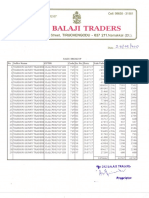

- Balaji Traders Sales July PDFDocument1 pageBalaji Traders Sales July PDFcachandhiranNo ratings yet

- Aadhar 1Document1 pageAadhar 1cachandhiranNo ratings yet

- ComDocument2 pagesComcachandhiranNo ratings yet

- Nila TextilesDocument1 pageNila TextilescachandhiranNo ratings yet

- Star positions for boy and girl horoscopesDocument9 pagesStar positions for boy and girl horoscopescachandhiranNo ratings yet

- Rental AgreementDocument2 pagesRental AgreementcachandhiranNo ratings yet

- Letter From DepartmentDocument1 pageLetter From DepartmentcachandhiranNo ratings yet

- Balaji Traders Sales JulyDocument1 pageBalaji Traders Sales JulycachandhiranNo ratings yet

- Samayasangili Road, Avathipalayam, Pallipalayam Erode 638008. GSTIN: 33FAMPS4712L1Z9Document1 pageSamayasangili Road, Avathipalayam, Pallipalayam Erode 638008. GSTIN: 33FAMPS4712L1Z9cachandhiranNo ratings yet

- Itr VDocument1 pageItr VcachandhiranNo ratings yet

- Bank ChallanDocument1 pageBank ChallancachandhiranNo ratings yet

- Reck NorDocument5 pagesReck NorcachandhiranNo ratings yet

- Tamil Nadu VAT Registration Certificate for Sri Kumaravel TextilesDocument2 pagesTamil Nadu VAT Registration Certificate for Sri Kumaravel TextilescachandhiranNo ratings yet

- Tamil Nadu VAT registration receiptDocument1 pageTamil Nadu VAT registration receiptcachandhiranNo ratings yet

- Registration AknowDocument1 pageRegistration AknowcachandhiranNo ratings yet

- A: !B 6m D6Of !b6ofirn 8) RR B: RR RR L I TDocument1 pageA: !B 6m D6Of !b6ofirn 8) RR B: RR RR L I Tcachandhiran100% (1)

- Vitamin B12: Essential for RBC Formation and CNS MaintenanceDocument19 pagesVitamin B12: Essential for RBC Formation and CNS MaintenanceHari PrasathNo ratings yet

- Edu 510 Final ProjectDocument13 pagesEdu 510 Final Projectapi-324235159No ratings yet

- Olimpiada Engleza 2017 CL A 7 A PDFDocument4 pagesOlimpiada Engleza 2017 CL A 7 A PDFAnthony Adams100% (3)

- People v. De Joya dying declaration incompleteDocument1 pagePeople v. De Joya dying declaration incompletelividNo ratings yet

- Med 07Document5 pagesMed 07ainee dazaNo ratings yet

- The Bachelor of ArtsDocument6 pagesThe Bachelor of ArtsShubhajit Nayak100% (2)

- Simon Baumberg - Prokaryotic Gene ExpressionDocument348 pagesSimon Baumberg - Prokaryotic Gene ExpressionBodhi Dharma0% (1)

- Dynamics of Bases F 00 BarkDocument476 pagesDynamics of Bases F 00 BarkMoaz MoazNo ratings yet

- Personal Branding dan Positioning Mempengaruhi Perilaku Pemilih di Kabupaten Bone BolangoDocument17 pagesPersonal Branding dan Positioning Mempengaruhi Perilaku Pemilih di Kabupaten Bone BolangoMuhammad Irfan BasriNo ratings yet

- John R. Van Wazer's concise overview of phosphorus compound nomenclatureDocument7 pagesJohn R. Van Wazer's concise overview of phosphorus compound nomenclatureFernanda Stuani PereiraNo ratings yet

- Signal WordsDocument2 pagesSignal WordsJaol1976No ratings yet

- University Students' Listening Behaviour of FM Radio Programmes in NigeriaDocument13 pagesUniversity Students' Listening Behaviour of FM Radio Programmes in NigeriaDE-CHOICE COMPUTER VENTURENo ratings yet

- Economic History Society, Wiley The Economic History ReviewDocument3 pagesEconomic History Society, Wiley The Economic History Reviewbiniyam.assefaNo ratings yet

- Assignment OUMH1203 English For Written Communication September 2023 SemesterDocument15 pagesAssignment OUMH1203 English For Written Communication September 2023 SemesterFaiz MufarNo ratings yet

- Lesson Plan 3Document6 pagesLesson Plan 3api-370683519No ratings yet

- Reducing Work Related Psychological Ill Health and Sickness AbsenceDocument15 pagesReducing Work Related Psychological Ill Health and Sickness AbsenceBM2062119PDPP Pang Kuok WeiNo ratings yet

- Ductile Brittle TransitionDocument7 pagesDuctile Brittle TransitionAndrea CalderaNo ratings yet

- Module 1-PRELIM: Southern Baptist College M'lang, CotabatoDocument11 pagesModule 1-PRELIM: Southern Baptist College M'lang, CotabatoVen TvNo ratings yet

- Configure Windows 10 for Aloha POSDocument7 pagesConfigure Windows 10 for Aloha POSBobbyMocorroNo ratings yet

- Experiment 5 ADHAVANDocument29 pagesExperiment 5 ADHAVANManoj Raj RajNo ratings yet

- Novel anti-tuberculosis strategies and nanotechnology-based therapies exploredDocument16 pagesNovel anti-tuberculosis strategies and nanotechnology-based therapies exploredArshia NazirNo ratings yet

- Engb546 NP RevisedDocument5 pagesEngb546 NP RevisedRafaelaNo ratings yet

- Absolute TowersDocument11 pagesAbsolute TowersSandi Harlan100% (1)

- Ass 3 MGT206 11.9.2020Document2 pagesAss 3 MGT206 11.9.2020Ashiqur RahmanNo ratings yet

- Chapter 2Document26 pagesChapter 2Dinindu Siriwardene100% (1)

- Chapter 2 Human Anatomy & Physiology (Marieb)Document3 pagesChapter 2 Human Anatomy & Physiology (Marieb)JayjayNo ratings yet

- DNS Mapping and Name ResolutionDocument5 pagesDNS Mapping and Name ResolutionAmit Rashmi SharmaNo ratings yet

- Leibniz Integral Rule - WikipediaDocument70 pagesLeibniz Integral Rule - WikipediaMannu Bhattacharya100% (1)