You might also like

- Economy of BangladeshDocument20 pagesEconomy of BangladeshYash ModiNo ratings yet

- Sehat Pharma Jin's Ratio AnalysisDocument50 pagesSehat Pharma Jin's Ratio AnalysisYash ModiNo ratings yet

- Partner Ship DeedDocument3 pagesPartner Ship DeedabhannanNo ratings yet

- Tata & Corus: Date - 24 July, 2011Document24 pagesTata & Corus: Date - 24 July, 2011Karan AhujaNo ratings yet

- Brand Integration Practices in Merger and AquisitionsDocument26 pagesBrand Integration Practices in Merger and AquisitionsValerica Morar DanNo ratings yet

- SuggestionDocument1 pageSuggestionYash ModiNo ratings yet

- NEW MBA Sem2 Detailed SyllabusDocument23 pagesNEW MBA Sem2 Detailed SyllabussuchipatelNo ratings yet

- ch-1-Intro-to-Lean Mfg.Document26 pagesch-1-Intro-to-Lean Mfg.Yash ModiNo ratings yet

- A Project Report Of: " Solar Summar Shirt "Document11 pagesA Project Report Of: " Solar Summar Shirt "Yash ModiNo ratings yet

- Project Report On Jyoti CNC PDFDocument79 pagesProject Report On Jyoti CNC PDFYash Modi100% (1)

- NdaDocument4 pagesNdajgurianaNo ratings yet

- AMUL Chocolate Marketing StrategiesDocument78 pagesAMUL Chocolate Marketing StrategiesDarshan Makwana100% (1)

- Project Report On Management Information SystemDocument11 pagesProject Report On Management Information SystemYash Modi0% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- STAFF INSTRUCTIONSDocument56 pagesSTAFF INSTRUCTIONSBatjargal EnkhbatNo ratings yet

- Hotel Duty Manager Job DescriptionDocument3 pagesHotel Duty Manager Job DescriptionHilje Kim0% (1)

- Greaves CottonDocument12 pagesGreaves CottonRevathy MenonNo ratings yet

- Somera ProjMgtExer3Document2 pagesSomera ProjMgtExer3john johnNo ratings yet

- Chithambara College Past Students Association AccountsDocument61 pagesChithambara College Past Students Association Accountsapi-140426513No ratings yet

- RPT Life Basic XDocument9 pagesRPT Life Basic XKhryz CallëjaNo ratings yet

- Industrial RelationsDocument20 pagesIndustrial RelationsankitakusNo ratings yet

- Employee Relations PRDocument12 pagesEmployee Relations PRNiharika SoniNo ratings yet

- Payroll Systems in EthiopiaDocument16 pagesPayroll Systems in EthiopiaMagarsaa Hirphaa100% (3)

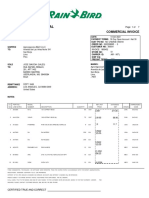

- Rain Bird International: 6991 E. Southpoint Road Tucson, AZ 85756 United States Fed Tax ID: 95-2402826Document7 pagesRain Bird International: 6991 E. Southpoint Road Tucson, AZ 85756 United States Fed Tax ID: 95-2402826Alejandra JamboNo ratings yet

- Rsik ManagementDocument221 pagesRsik ManagementNirmal ShresthaNo ratings yet

- Unit 1 Concept of Human Resources ManagementDocument2 pagesUnit 1 Concept of Human Resources ManagementPrajita ShresthaNo ratings yet

- Aus Tin 20104493Document166 pagesAus Tin 20104493david_llewellyn_smithNo ratings yet

- PM January 2021 Lecture 4 Worked Examples Questions (Drury (2012), P. 451, 17.17)Document6 pagesPM January 2021 Lecture 4 Worked Examples Questions (Drury (2012), P. 451, 17.17)KAY PHINE NGNo ratings yet

- IPCC SM Notes by CA Swapnil Patni Sir May 2019 PDFDocument77 pagesIPCC SM Notes by CA Swapnil Patni Sir May 2019 PDFBlSt SamarNo ratings yet

- Sample Questions For 2019-2020 Following Sample Questions Are Provided For The Benefits of Students. They Are Indicative OnlyDocument33 pagesSample Questions For 2019-2020 Following Sample Questions Are Provided For The Benefits of Students. They Are Indicative OnlyPrathamesh ChawanNo ratings yet

- FMar Financial Markets Formulas Rob NotesDocument8 pagesFMar Financial Markets Formulas Rob NotesEvelyn LabhananNo ratings yet

- Joint Venture AgreementDocument2 pagesJoint Venture Agreementpan RegisterNo ratings yet

- Exploring Social Origins in The Construction of ESDocument37 pagesExploring Social Origins in The Construction of ESFabioNo ratings yet

- Solved Twelve Accounting and Financial Services Professionals Opt To Form ADocument1 pageSolved Twelve Accounting and Financial Services Professionals Opt To Form AAnbu jaromiaNo ratings yet

- Materials Management Ec IVDocument92 pagesMaterials Management Ec IVshivashankaracharNo ratings yet

- FPC ManualDocument8 pagesFPC ManualAdnan KaraahmetovicNo ratings yet

- CBCS Guidelines For B.comh Sem VI Paper No - BCH 6.1 Auditing and Corporate GovernanceDocument2 pagesCBCS Guidelines For B.comh Sem VI Paper No - BCH 6.1 Auditing and Corporate GovernanceJoel DinicNo ratings yet

- Infosys Sourcing & Procurement - Fact Sheet: S2C R2I I2PDocument2 pagesInfosys Sourcing & Procurement - Fact Sheet: S2C R2I I2PGautam SinghalNo ratings yet

- PP Def MODocument16 pagesPP Def MOBayu Agung PrakosoNo ratings yet

- FINAL DRAFT BEC324 2021 Assignment 1Document10 pagesFINAL DRAFT BEC324 2021 Assignment 1stanely ndlovuNo ratings yet

- DividendDocument16 pagesDividendnideeshNo ratings yet

- F8 (AA) Kit - Que 81 Prancer ConstructionDocument2 pagesF8 (AA) Kit - Que 81 Prancer ConstructionChrisNo ratings yet

- I HG F Autumn 2018 ApplicationformDocument8 pagesI HG F Autumn 2018 ApplicationformSnzy DelNo ratings yet

- T7 TCS 【愛知】Bilingual Design Engineer PDFDocument3 pagesT7 TCS 【愛知】Bilingual Design Engineer PDFchutiyaNo ratings yet