You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Battlemaxx WaiverDocument1 pageBattlemaxx WaiverPete DebonoNo ratings yet

- General Power of AttorneyDocument2 pagesGeneral Power of AttorneyDred OpleNo ratings yet

- Insurance SectorDocument40 pagesInsurance SectorRaunak ChaurasiaNo ratings yet

- Comparative Study of Loan and Advances AnalysisDocument102 pagesComparative Study of Loan and Advances AnalysisRavi Mori100% (2)

- The Role of Ceo in The Strategic PlanningDocument18 pagesThe Role of Ceo in The Strategic PlanningmanofhonourNo ratings yet

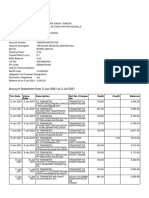

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurNo ratings yet

- Credit CardDocument15 pagesCredit Cardsrdagpnt100% (1)

- GK Bullet - SBI PO (Mains) II PDFDocument33 pagesGK Bullet - SBI PO (Mains) II PDFgaurav singhNo ratings yet

- Mande Morisho What Do You Know About Depository InstitutionsDocument2 pagesMande Morisho What Do You Know About Depository InstitutionsMand'e MorishoNo ratings yet

- 2020 MDCN Remita LicenseDocument1 page2020 MDCN Remita LicenseFavour MichaelNo ratings yet

- WithdrawnDocument1 pageWithdrawnchek86351No ratings yet

- Business Contacts OctoberDocument15 pagesBusiness Contacts OctoberDurban Chamber of Commerce and IndustryNo ratings yet

- PNB Retail Lending SchemesDocument6 pagesPNB Retail Lending Schemesanon_617153150No ratings yet

- Final Course Multiple Choice Questions Questions 17 and 35 Have Been Revised. Students Are Advised To Refer The Revised QuestionsDocument13 pagesFinal Course Multiple Choice Questions Questions 17 and 35 Have Been Revised. Students Are Advised To Refer The Revised QuestionsDiwakar GiriNo ratings yet

- PB 2019-035 Noodregeling Banco Del Orinoco ENG BDO 20190906Document1 pagePB 2019-035 Noodregeling Banco Del Orinoco ENG BDO 20190906Knipselkrant CuracaoNo ratings yet

- 100 MCQ NegoDocument12 pages100 MCQ NegoDaphneNo ratings yet

- IDA PT - Pos Indonesia (Persero) ID - Indonesia: Operator DetailsDocument5 pagesIDA PT - Pos Indonesia (Persero) ID - Indonesia: Operator DetailssocalopeNo ratings yet

- STARTRADE RO - Comisioane Si Taxe STARTRADE RO - Fees and CommissionsDocument3 pagesSTARTRADE RO - Comisioane Si Taxe STARTRADE RO - Fees and CommissionsAzi NuNo ratings yet

- BANK ACT 1864 (Original) Common-Law RemedyDocument4 pagesBANK ACT 1864 (Original) Common-Law Remedyin1or100% (1)

- Study On The Banking Services Provided by Uttarakhand Gramin BankDocument12 pagesStudy On The Banking Services Provided by Uttarakhand Gramin BankDivyansh KaushikNo ratings yet

- EcsmformDocument1 pageEcsmform0sandeepNo ratings yet

- Ixambee Monthly December CapsuleDocument48 pagesIxambee Monthly December CapsulejoydsNo ratings yet

- CE-2023 Challan FormDocument1 pageCE-2023 Challan FormAbdul RehmanNo ratings yet

- Annual Report - BPL LTD - FY - 2010-11Document40 pagesAnnual Report - BPL LTD - FY - 2010-11ksachchuNo ratings yet

- Effect of Electronic Banking On Financial Performance of Deposit Taking Micro Finance Institutions in Kisii TownDocument5 pagesEffect of Electronic Banking On Financial Performance of Deposit Taking Micro Finance Institutions in Kisii TownIOSRjournalNo ratings yet

- Questionnaire: Brand Loyalty and Relationship Marketing in State Bank of India's Banking System. IDocument6 pagesQuestionnaire: Brand Loyalty and Relationship Marketing in State Bank of India's Banking System. IAanand SharmaNo ratings yet

- FY19 Global MNC Plan FinalDocument21 pagesFY19 Global MNC Plan FinalMARTHA HDEZNo ratings yet

- Alice in Credit-Card Land - On ChargebacksDocument3 pagesAlice in Credit-Card Land - On ChargebacksFábio OliveiraNo ratings yet

- Easypaisa Money Transfer To Any Mobile NumberDocument2 pagesEasypaisa Money Transfer To Any Mobile NumberBryan WalkerNo ratings yet

- Alpha PDFDocument13 pagesAlpha PDFWARWICKJNo ratings yet