You might also like

- Data Analysis TableDocument6 pagesData Analysis TableSahar GullNo ratings yet

- Final MKTNG MGT PrOjectDocument39 pagesFinal MKTNG MGT PrOjectSahar GullNo ratings yet

- BRM Research Proposal - Docx111Document38 pagesBRM Research Proposal - Docx111Sahar GullNo ratings yet

- List of Candidates for Combined Competitive Examination 2013Document355 pagesList of Candidates for Combined Competitive Examination 2013Sahar GullNo ratings yet

- Dessler 07Document10 pagesDessler 07Sahar GullNo ratings yet

- Student Text Messaging Survey ResultsDocument19 pagesStudent Text Messaging Survey ResultsSahar GullNo ratings yet

- Case Study 1Document3 pagesCase Study 1Sahar GullNo ratings yet

- HR Department in PTCLDocument30 pagesHR Department in PTCLOwais Yunus80% (10)

- Dessler 04Document12 pagesDessler 04Sahar GullNo ratings yet

- Dessler 07Document10 pagesDessler 07Sahar GullNo ratings yet

- Dessler 04Document12 pagesDessler 04Sahar GullNo ratings yet

- Chapter5recruiting 120614094444 Phpapp01Document34 pagesChapter5recruiting 120614094444 Phpapp01Sahar GullNo ratings yet

- Dessler 04Document12 pagesDessler 04Sahar GullNo ratings yet

- Dessler 07Document10 pagesDessler 07Sahar GullNo ratings yet

- Dessler 04Document12 pagesDessler 04Sahar GullNo ratings yet

- Chap 014Document45 pagesChap 014Sahar GullNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Section 2 RPNC180044Document12 pagesSection 2 RPNC180044pmcmbharat264No ratings yet

- FCA 2020 Third Quarter Results PresentationDocument33 pagesFCA 2020 Third Quarter Results PresentationSimon AlvarezNo ratings yet

- SSE Illustrative Financial StatementsDocument19 pagesSSE Illustrative Financial StatementsjointariqaslamNo ratings yet

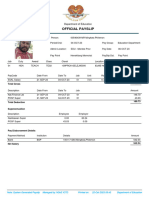

- Official Payslip: Department of EducationDocument1 pageOfficial Payslip: Department of Educationphillmingkwa2017No ratings yet

- Project WHEELS INDIADocument63 pagesProject WHEELS INDIAPriya MahiNo ratings yet

- Delta Star IncorporatedDocument4 pagesDelta Star IncorporatedJackson KhannaNo ratings yet

- The Accompanying Notes Are An Integral Part of The Financial StatementsDocument3 pagesThe Accompanying Notes Are An Integral Part of The Financial StatementsRavi BhartiaNo ratings yet

- GB935-A Business Metric Specifications-V7 1Document201 pagesGB935-A Business Metric Specifications-V7 1Jaime Wall100% (1)

- Income Tax Form 49ADocument4 pagesIncome Tax Form 49ArajkamalmauryaNo ratings yet

- Wall Street Playboys-Triangle Investing-Stocks, Real Estate and Crypto CurrenciesDocument139 pagesWall Street Playboys-Triangle Investing-Stocks, Real Estate and Crypto Currenciesboo100% (5)

- Airtel Financial Analysis and Ratio StudyDocument32 pagesAirtel Financial Analysis and Ratio StudyMohammad Anwar AliNo ratings yet

- BIR Form Certificate Tax WithheldDocument3 pagesBIR Form Certificate Tax WithheldErick Echual75% (4)

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 pagesNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarNo ratings yet

- Financial Notes by JMR SirDocument70 pagesFinancial Notes by JMR SirAlekhya ThirumaniNo ratings yet

- White Paper of AURICOINDocument29 pagesWhite Paper of AURICOINLuis Saul Castro GomezNo ratings yet

- AP Long Test 1 - CHANGES&ERROR, CASH ACCRUAL, SINGLE ENTRYDocument12 pagesAP Long Test 1 - CHANGES&ERROR, CASH ACCRUAL, SINGLE ENTRYjasfNo ratings yet

- Mitchell's Fruit Farm 2011 Final ProjectDocument43 pagesMitchell's Fruit Farm 2011 Final ProjectRahila Saeed0% (1)

- Chapter 9 Property, Plant and Equipment (Autosaved)Document22 pagesChapter 9 Property, Plant and Equipment (Autosaved)Ji BaltazarNo ratings yet

- Demand and Supply: Dr. Sanja Samirana PattnayakDocument51 pagesDemand and Supply: Dr. Sanja Samirana PattnayakSubhash MohanNo ratings yet

- WORKING CAP MGMT AND FIN STATEMNTS ANALYSIS PDF 8708Document12 pagesWORKING CAP MGMT AND FIN STATEMNTS ANALYSIS PDF 8708lena cpa0% (1)

- CocolifeDocument29 pagesCocolifeMarked ReverseNo ratings yet

- Management Accounting/Series-3-2007 (Code3023)Document15 pagesManagement Accounting/Series-3-2007 (Code3023)Hein Linn Kyaw100% (1)

- Fairview Park Master Plan 1999Document177 pagesFairview Park Master Plan 1999WestLifeNewspaperNo ratings yet

- DepreciationDocument8 pagesDepreciationanjalikapoorNo ratings yet

- Q5 Items of Gross IncomeDocument10 pagesQ5 Items of Gross IncomeNhaj0% (2)

- Hyperlink - Part 1 - RevisedDocument3 pagesHyperlink - Part 1 - RevisedAnonymous lJYeWYKVScNo ratings yet

- Business Valuation and Case Study at Petrom OMVDocument7 pagesBusiness Valuation and Case Study at Petrom OMVGrigoras Alexandru NicolaeNo ratings yet

- International Taxation ExamsDocument2 pagesInternational Taxation ExamsAnitaTanjungIINo ratings yet

- Trial Balance ReportDocument19 pagesTrial Balance ReportJeremy LunsodNo ratings yet

- The Strategy of International BusinessDocument68 pagesThe Strategy of International BusinessPrachi RajanNo ratings yet