You might also like

- EN Oil Supply and DemandDocument9 pagesEN Oil Supply and Demandtanyan.huangNo ratings yet

- Weiner 2003 NoteDocument23 pagesWeiner 2003 NoteMohit YadavNo ratings yet

- Oil's Endless Bid: Taming the Unreliable Price of Oil to Secure Our EconomyFrom EverandOil's Endless Bid: Taming the Unreliable Price of Oil to Secure Our EconomyNo ratings yet

- Oilprice ArticleDocument4 pagesOilprice ArticleGeorge OnyewuchiNo ratings yet

- Research Paper Oil PricesDocument5 pagesResearch Paper Oil Pricesfvfr9cg8100% (1)

- Energy Myths and Realities: Bringing Science to the Energy Policy DebateFrom EverandEnergy Myths and Realities: Bringing Science to the Energy Policy DebateRating: 4 out of 5 stars4/5 (4)

- Profiting from Oil Price Crashes Using Futures Market SignalsDocument34 pagesProfiting from Oil Price Crashes Using Futures Market Signalsasdf324342No ratings yet

- 6-26-12 Greed Is Good.Document4 pages6-26-12 Greed Is Good.The Gold SpeculatorNo ratings yet

- Pem-Web Oil Prices 2010Document5 pagesPem-Web Oil Prices 2010joescribd55No ratings yet

- Musings: Energy Stocks Have Mostly Trailed The Market This YearDocument10 pagesMusings: Energy Stocks Have Mostly Trailed The Market This YearMurugiah RamilaNo ratings yet

- Essay SampleDocument25 pagesEssay SampleLuis MartinezNo ratings yet

- Oil Price Research PaperDocument7 pagesOil Price Research Paperlrqylwznd100% (1)

- Arab Uprising and The International Oil MarketsDocument16 pagesArab Uprising and The International Oil MarketsgungorduyusufNo ratings yet

- Statistical Approach to Forecasting Crude Oil PricesDocument19 pagesStatistical Approach to Forecasting Crude Oil PricesHarshit Shah100% (1)

- The Growing Case For Commodities: Investment InsightsDocument3 pagesThe Growing Case For Commodities: Investment InsightsAnonymous Ht0MIJNo ratings yet

- Impact of U.S. Recession On India - An Empirical StudyDocument22 pagesImpact of U.S. Recession On India - An Empirical StudyashokdgaurNo ratings yet

- Literature Review On Oil PricesDocument6 pagesLiterature Review On Oil Pricesjicjtjxgf100% (1)

- Ici Research: PerspectiveDocument32 pagesIci Research: PerspectiveDavid LimNo ratings yet

- Shamik Bhose September Crude Oil ReportDocument8 pagesShamik Bhose September Crude Oil ReportshamikbhoseNo ratings yet

- The Impact of Oil Price Shocks On The U.S. Stock MarketDocument22 pagesThe Impact of Oil Price Shocks On The U.S. Stock MarketJacobo De Jesus Morales FontalvoNo ratings yet

- Journal of International Financial Markets, Institutions & MoneyDocument26 pagesJournal of International Financial Markets, Institutions & Moneysatrio pangestuNo ratings yet

- Understanding Shocks of Oil Prices: IJASCSE Vol 1 Issue 1 2012Document7 pagesUnderstanding Shocks of Oil Prices: IJASCSE Vol 1 Issue 1 2012IJASCSENo ratings yet

- Index Investment and Financialization of Commodities: Ke Tang and Wei XiongDocument46 pagesIndex Investment and Financialization of Commodities: Ke Tang and Wei Xiongmylife123No ratings yet

- World Oil Demand and The Effect On Oil Prices 3Document16 pagesWorld Oil Demand and The Effect On Oil Prices 3Bhanu MehraNo ratings yet

- Insight 68 A Comparative History of Oil and Gas Markets and Prices PDFDocument22 pagesInsight 68 A Comparative History of Oil and Gas Markets and Prices PDFManuel SantillanNo ratings yet

- Role of Speculators in Crude Oil Futures MarketsDocument40 pagesRole of Speculators in Crude Oil Futures MarketsoptisearchNo ratings yet

- Brochure Commodities Investing 2009 08Document8 pagesBrochure Commodities Investing 2009 08Vishal MhaiskarNo ratings yet

- Daniel Ahn Speculation Commodity PricesDocument29 pagesDaniel Ahn Speculation Commodity PricesDan DickerNo ratings yet

- A Proposed Monetary Regime For Small Commodity-Exporters: Peg The Export Price ("PEP") Jeffrey Frankel Harpel Professor, Harvard UniversityDocument46 pagesA Proposed Monetary Regime For Small Commodity-Exporters: Peg The Export Price ("PEP") Jeffrey Frankel Harpel Professor, Harvard UniversityTriumph OkojieNo ratings yet

- Deutsche Bank An Investor Guide To Commodities April 2005Document70 pagesDeutsche Bank An Investor Guide To Commodities April 2005AlCapone1111No ratings yet

- 40 Years of Oil Price Surprises: Why Expectations Remain DifficultDocument23 pages40 Years of Oil Price Surprises: Why Expectations Remain DifficultJacobo De Jesus Morales FontalvoNo ratings yet

- Study of Fundamental Analysis For Crude Oil Futures PricesDocument27 pagesStudy of Fundamental Analysis For Crude Oil Futures PricessaminabatangiNo ratings yet

- The Drive Toward Biofuels: A Guide To Mandates, Supply and MarketingDocument4 pagesThe Drive Toward Biofuels: A Guide To Mandates, Supply and MarketingCota OilNo ratings yet

- Economic Theories AnalysisDocument6 pagesEconomic Theories AnalysisKennethNo ratings yet

- 4 Lindung Nilai BRDSRKN Pasar KomoditDocument55 pages4 Lindung Nilai BRDSRKN Pasar Komoditelizabeth karinaNo ratings yet

- Impact of Oil Prices On The Stock MarketDocument18 pagesImpact of Oil Prices On The Stock MarketDhruv AghiNo ratings yet

- Debt, Credit and Finance Capital by Plotkin and ScheuermanDocument8 pagesDebt, Credit and Finance Capital by Plotkin and Scheuermandennis ridenourNo ratings yet

- Delloite Oil and Gas Reality Check 2015 PDFDocument32 pagesDelloite Oil and Gas Reality Check 2015 PDFAzik KunouNo ratings yet

- The Stock Market Reaction To Oil Price ChangesDocument35 pagesThe Stock Market Reaction To Oil Price ChangesVincent FongNo ratings yet

- Oil Price DissertationDocument7 pagesOil Price DissertationDoMyPaperForMeUK100% (1)

- Oil Prices Term PaperDocument5 pagesOil Prices Term Papereeyjzkwgf100% (1)

- This Is No Time For Celebration, The Oil Rally Is Just Getting Started (Commodity - CL1 - COM) - Seeking AlphaDocument5 pagesThis Is No Time For Celebration, The Oil Rally Is Just Getting Started (Commodity - CL1 - COM) - Seeking AlphaMARIA BEATRIZ ABELENDANo ratings yet

- Definition of PetrodollarsDocument2 pagesDefinition of PetrodollarspaulicalejerNo ratings yet

- The U.S. Trade Deficit, The Dollar, and The Price of Oil: James K. JacksonDocument24 pagesThe U.S. Trade Deficit, The Dollar, and The Price of Oil: James K. JacksonMichael OzanianNo ratings yet

- WE ARE ON THE CUSP OF A GLOBAL ENERGY CRISISDocument27 pagesWE ARE ON THE CUSP OF A GLOBAL ENERGY CRISISYog MehtaNo ratings yet

- Financial Markets 150811Document6 pagesFinancial Markets 150811Jacques AboaNo ratings yet

- Speculation, Fundamentals and The Price of Crude OilDocument49 pagesSpeculation, Fundamentals and The Price of Crude OilNgwe Min TheinNo ratings yet

- Factiva 20180604 1444Document131 pagesFactiva 20180604 1444Lucas GodeiroNo ratings yet

- Petrobas ValuationDocument26 pagesPetrobas ValuationAditya KhannaNo ratings yet

- 2008 Bear Market Analysis Inv Perp 1969-2007Document5 pages2008 Bear Market Analysis Inv Perp 1969-2007arfwayarryNo ratings yet

- Understanding The Core Fundamentals For Trading OilDocument12 pagesUnderstanding The Core Fundamentals For Trading Oilhilquias otinielNo ratings yet

- How Are Oil Prices DeterminedDocument8 pagesHow Are Oil Prices DeterminedSumit SachdevaNo ratings yet

- Oil Shocks To Stock ReturnDocument46 pagesOil Shocks To Stock ReturnJose Mayer SinagaNo ratings yet

- Maize & Blue Fund - Economist Group - Sector Pitch - Underweight EnergyDocument19 pagesMaize & Blue Fund - Economist Group - Sector Pitch - Underweight EnergyNaufal SanaullahNo ratings yet

- Section: BS Accountancy - 2A: Types of Financial MarketsDocument2 pagesSection: BS Accountancy - 2A: Types of Financial MarketsChristian Paul GabrielNo ratings yet

- Dissertation Oil PricesDocument4 pagesDissertation Oil PricesDoMyCollegePaperForMeColumbia100% (1)

- What Explains The Growth in Commodity Derivatives?: Parantap Basu andDocument12 pagesWhat Explains The Growth in Commodity Derivatives?: Parantap Basu andFaisal JashimuddinNo ratings yet

- US Senate Approves Sweeping Tax Overhaul Financial Times 01.12.17Document2 pagesUS Senate Approves Sweeping Tax Overhaul Financial Times 01.12.17Alfredo Jalife RahmeNo ratings yet

- Republicans' Tax Reform Drive Hit by Deficit Projections Financial Times 01.12.17Document4 pagesRepublicans' Tax Reform Drive Hit by Deficit Projections Financial Times 01.12.17Alfredo Jalife RahmeNo ratings yet

- US Has A Fifth Ace in Its Poker Game With China Fuente Financial Times 07.11.17Document1 pageUS Has A Fifth Ace in Its Poker Game With China Fuente Financial Times 07.11.17Alfredo Jalife Rahme100% (1)

- America's 12 Demands To Iran Over Alleged Activity FT 21.05.18Document1 pageAmerica's 12 Demands To Iran Over Alleged Activity FT 21.05.18Alfredo Jalife RahmeNo ratings yet

- Mueller Charges Pitch US Towards Constitutional Crisis Financial TimesDocument3 pagesMueller Charges Pitch US Towards Constitutional Crisis Financial TimesAlfredo Jalife RahmeNo ratings yet

- Iraq's Seizure of Kirkuk Is Part of A Much Bigger Story Fuente Financial TimesDocument3 pagesIraq's Seizure of Kirkuk Is Part of A Much Bigger Story Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- China Sells First Dollar Bond in More Than A Decade Financial TimesDocument2 pagesChina Sells First Dollar Bond in More Than A Decade Financial TimesAlfredo Jalife RahmeNo ratings yet

- Lobbyist Podesta To Resign in Fallout From Mueller Action Financial TimesDocument2 pagesLobbyist Podesta To Resign in Fallout From Mueller Action Financial TimesAlfredo Jalife RahmeNo ratings yet

- Millions Mired in Poverty As US Upturn Passes Them By, Study Finds Fuente Financial TimesDocument5 pagesMillions Mired in Poverty As US Upturn Passes Them By, Study Finds Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- Trump Gives Glimpse of Indo-Pacific' Strategy To Counter China 10.11.17 Financial TimesDocument5 pagesTrump Gives Glimpse of Indo-Pacific' Strategy To Counter China 10.11.17 Financial TimesAlfredo Jalife RahmeNo ratings yet

- Tillerson Sees Closer India Ties As Foil Against China Fuente Financial TimesDocument3 pagesTillerson Sees Closer India Ties As Foil Against China Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- Chinese Property Boom Props Up Xi's Hopes For The Economy Financial TimesDocument8 pagesChinese Property Boom Props Up Xi's Hopes For The Economy Financial TimesAlfredo Jalife RahmeNo ratings yet

- Stanley Fischer, Fed Vice-Chair, On The Risky Business of Bank Reform, Fuente FTDocument7 pagesStanley Fischer, Fed Vice-Chair, On The Risky Business of Bank Reform, Fuente FTAlfredo Jalife Rahme100% (1)

- China Launches Renminbi-Denominated Gold Benchmark Fuente: Financial TimesDocument2 pagesChina Launches Renminbi-Denominated Gold Benchmark Fuente: Financial TimesAlfredo Jalife Rahme100% (1)

- The Influence of Stanley Fischer Larry Summers' Blog, Fuente Financial TimesDocument1 pageThe Influence of Stanley Fischer Larry Summers' Blog, Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- At Our Own Peril: DoD Risk Assessment in A Post-Primacy WorldDocument141 pagesAt Our Own Peril: DoD Risk Assessment in A Post-Primacy WorldAlfredo Jalife Rahme100% (2)

- François Hollande Calls On Europe To Stand Up To Donald Trump Fuente: Financial TimesDocument2 pagesFrançois Hollande Calls On Europe To Stand Up To Donald Trump Fuente: Financial TimesAlfredo Jalife RahmeNo ratings yet

- The Influence of Stanley Fischer Larry Summers' Blog, Fuente Financial TimesDocument1 pageThe Influence of Stanley Fischer Larry Summers' Blog, Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- Xi Jinping's Silk Road Is Under Threat From One-Way Traffic Fuente Financial TimesDocument3 pagesXi Jinping's Silk Road Is Under Threat From One-Way Traffic Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- China Lashes Out at US As Trump-Xi Honeymoon Ends Fuente Financial TimesDocument4 pagesChina Lashes Out at US As Trump-Xi Honeymoon Ends Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- John McCain Is One of The Few Who Can Stand Up To Donald TrumpDocument3 pagesJohn McCain Is One of The Few Who Can Stand Up To Donald TrumpAlfredo Jalife RahmeNo ratings yet

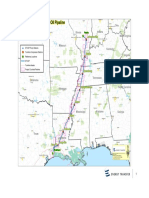

- Energy Transfer Crude Oil Company MapDocument1 pageEnergy Transfer Crude Oil Company MapAlfredo Jalife RahmeNo ratings yet

- Kremlin Says Trump and Putin To Collaborate On Isis Terrorism Fuente Financial TimesDocument2 pagesKremlin Says Trump and Putin To Collaborate On Isis Terrorism Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- China's Xi Hails Belt and Road As Project of The Century' Fuente FTDocument4 pagesChina's Xi Hails Belt and Road As Project of The Century' Fuente FTAlfredo Jalife RahmeNo ratings yet

- Trump Demands Solution To US Trade Deficits With China and Others 31.03.17Document4 pagesTrump Demands Solution To US Trade Deficits With China and Others 31.03.17Alfredo Jalife RahmeNo ratings yet

- Trump's $54 Billion Rounding Error Fuente Foreign AffairsDocument2 pagesTrump's $54 Billion Rounding Error Fuente Foreign AffairsAlfredo Jalife RahmeNo ratings yet

- Value of Stocks On S&P 500 Pushes Through $20tn For First TimeDocument4 pagesValue of Stocks On S&P 500 Pushes Through $20tn For First TimeAlfredo Jalife RahmeNo ratings yet

- Trump To Call Putin As He Considers Lifting Russia Sanctions Fuente Financial TimesDocument4 pagesTrump To Call Putin As He Considers Lifting Russia Sanctions Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- Trump Pulls US Out of Pacific Trade PactDocument3 pagesTrump Pulls US Out of Pacific Trade PactAlfredo Jalife RahmeNo ratings yet

- Trump Hands May Promise of Stronger' Special Relationship Fuente Financial TimesDocument4 pagesTrump Hands May Promise of Stronger' Special Relationship Fuente Financial TimesAlfredo Jalife RahmeNo ratings yet

- Mergers in PetroleumDocument263 pagesMergers in PetroleumJohn W. Paterson IV100% (1)

- Pngstat 1617Document224 pagesPngstat 1617numanNo ratings yet

- Wikborg Global Offshore Projects DEC15Document13 pagesWikborg Global Offshore Projects DEC15sam ignarskiNo ratings yet

- Lecture Notes On Introduction To Oil and Gas Industry Jan2015Document10 pagesLecture Notes On Introduction To Oil and Gas Industry Jan2015Domo YhlNo ratings yet

- 2024 UAE Salary GuideDocument30 pages2024 UAE Salary Guideabdelrahman.m.youssefNo ratings yet

- Distribution of Key Natural ResourcesDocument23 pagesDistribution of Key Natural ResourcesSameer RajaNo ratings yet

- OECD and OPEC economic blocks reportDocument1 pageOECD and OPEC economic blocks reportSamiksha NaikNo ratings yet

- International Petroleum Agreements Evolve With Politics, Oil PricesDocument6 pagesInternational Petroleum Agreements Evolve With Politics, Oil PricesEmil İsmayilovNo ratings yet

- 6 - Globalisation and The NorthSouth DivideDocument17 pages6 - Globalisation and The NorthSouth DivideDeddy MurwantoNo ratings yet

- Chapter 4 GLOBAL INTERSTATE SYSTEM - AnnotatedDocument35 pagesChapter 4 GLOBAL INTERSTATE SYSTEM - AnnotatedMarianne Hope Villas100% (1)

- Global Strategy (Indian Equities - On Borrowed Time) 20211112 - 211113 - 201930Document14 pagesGlobal Strategy (Indian Equities - On Borrowed Time) 20211112 - 211113 - 201930Hardik ShahNo ratings yet

- Oil and Gas ReportDocument49 pagesOil and Gas ReportDapo Damilola Adebayo100% (1)

- Chapter 4 - A World of RegionsDocument37 pagesChapter 4 - A World of RegionsMila NacpilNo ratings yet

- In The Dark: The Hidden Climate Impacts of Energy Development On Public LandsDocument28 pagesIn The Dark: The Hidden Climate Impacts of Energy Development On Public LandsThe Wilderness SocietyNo ratings yet

- Midterm Contemporary Set ADocument2 pagesMidterm Contemporary Set AZamZamieNo ratings yet

- Oil Gas Guide 2019Document148 pagesOil Gas Guide 2019alex darmawanNo ratings yet

- Meed Year BookDocument158 pagesMeed Year BooksawkariqbalNo ratings yet

- The World Economy at The Beginning of The 21st Century.Document20 pagesThe World Economy at The Beginning of The 21st Century.Palaghian AdelinaNo ratings yet

- NewsDocument393 pagesNewsapi-3771259No ratings yet

- Kpds 2009 Mayıs IlkbaharDocument19 pagesKpds 2009 Mayıs IlkbaharDr. Hikmet ŞahinerNo ratings yet

- Oil Scams Guide PDFDocument46 pagesOil Scams Guide PDFarjunmadan1No ratings yet

- Cases. Lecture 02Document2 pagesCases. Lecture 02kezokal42No ratings yet

- Sustainable Energy and Resource ManagementDocument318 pagesSustainable Energy and Resource ManagementRajdeepSenNo ratings yet

- Oil and Gas AccountingDocument81 pagesOil and Gas Accountingmike8895100% (1)

- OPEC Governors - 6 July 2020Document1 pageOPEC Governors - 6 July 2020Djeloul AlgiersNo ratings yet

- AECOM-Hand BookDocument116 pagesAECOM-Hand BookVinod PSNo ratings yet

- Climate Report Saudi Arabia 2017Document5 pagesClimate Report Saudi Arabia 2017WellfroNo ratings yet

- Report On Covid-19 Business Opportunities & TrendsDocument65 pagesReport On Covid-19 Business Opportunities & TrendsPawan KumarNo ratings yet

- Part B Past Year Questions Ibm537Document10 pagesPart B Past Year Questions Ibm537adzwinj100% (1)

- Middle East Chronology - 1986-01-16 - 1986-04-15Document27 pagesMiddle East Chronology - 1986-01-16 - 1986-04-15rinaldofrancescaNo ratings yet

- 2023/2024 ASVAB For Dummies (+ 7 Practice Tests, Flashcards, & Videos Online)From Everand2023/2024 ASVAB For Dummies (+ 7 Practice Tests, Flashcards, & Videos Online)No ratings yet

- Outliers by Malcolm Gladwell - Book Summary: The Story of SuccessFrom EverandOutliers by Malcolm Gladwell - Book Summary: The Story of SuccessRating: 4.5 out of 5 stars4.5/5 (17)

- The PMP Project Management Professional Certification Exam Study Guide PMBOK Seventh 7th Edition: The Complete Exam Prep With Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First AttemptFrom EverandThe PMP Project Management Professional Certification Exam Study Guide PMBOK Seventh 7th Edition: The Complete Exam Prep With Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First AttemptNo ratings yet

- Auto Parts Storekeeper: Passbooks Study GuideFrom EverandAuto Parts Storekeeper: Passbooks Study GuideNo ratings yet

- Radiographic Testing: Theory, Formulas, Terminology, and Interviews Q&AFrom EverandRadiographic Testing: Theory, Formulas, Terminology, and Interviews Q&ANo ratings yet

- EMT (Emergency Medical Technician) Crash Course Book + OnlineFrom EverandEMT (Emergency Medical Technician) Crash Course Book + OnlineRating: 4.5 out of 5 stars4.5/5 (4)

- The NCLEX-RN Exam Study Guide: Premium Edition: Proven Methods to Pass the NCLEX-RN Examination with Confidence – Extensive Next Generation NCLEX (NGN) Practice Test Questions with AnswersFrom EverandThe NCLEX-RN Exam Study Guide: Premium Edition: Proven Methods to Pass the NCLEX-RN Examination with Confidence – Extensive Next Generation NCLEX (NGN) Practice Test Questions with AnswersNo ratings yet

- The Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsFrom EverandThe Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (76)

- ASE A1 Engine Repair Study Guide: Complete Review & Test Prep For The ASE A1 Engine Repair Exam: With Three Full-Length Practice Tests & AnswersFrom EverandASE A1 Engine Repair Study Guide: Complete Review & Test Prep For The ASE A1 Engine Repair Exam: With Three Full-Length Practice Tests & AnswersNo ratings yet

- Real Property, Law Essentials: Governing Law for Law School and Bar Exam PrepFrom EverandReal Property, Law Essentials: Governing Law for Law School and Bar Exam PrepNo ratings yet

- Programmer Aptitude Test (PAT): Passbooks Study GuideFrom EverandProgrammer Aptitude Test (PAT): Passbooks Study GuideNo ratings yet

- 2024 – 2025 FAA Drone License Exam Guide: A Simplified Approach to Passing the FAA Part 107 Drone License Exam at a sitting With Test Questions and AnswersFrom Everand2024 – 2025 FAA Drone License Exam Guide: A Simplified Approach to Passing the FAA Part 107 Drone License Exam at a sitting With Test Questions and AnswersNo ratings yet

- USMLE Step 1: Integrated Vignettes: Must-know, high-yield reviewFrom EverandUSMLE Step 1: Integrated Vignettes: Must-know, high-yield reviewRating: 4.5 out of 5 stars4.5/5 (7)

- EMT (Emergency Medical Technician) Crash Course with Online Practice Test, 2nd Edition: Get a Passing Score in Less TimeFrom EverandEMT (Emergency Medical Technician) Crash Course with Online Practice Test, 2nd Edition: Get a Passing Score in Less TimeRating: 3.5 out of 5 stars3.5/5 (3)

- Summary of Sapiens: A Brief History of Humankind By Yuval Noah HarariFrom EverandSummary of Sapiens: A Brief History of Humankind By Yuval Noah HarariRating: 1 out of 5 stars1/5 (3)

- Nursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASFrom EverandNursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASNo ratings yet

- Improve Your Global Business English: The Essential Toolkit for Writing and Communicating Across BordersFrom EverandImprove Your Global Business English: The Essential Toolkit for Writing and Communicating Across BordersRating: 4 out of 5 stars4/5 (14)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- PTCE - Pharmacy Technician Certification Exam Flashcard Book + OnlineFrom EverandPTCE - Pharmacy Technician Certification Exam Flashcard Book + OnlineNo ratings yet