You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Allahabad Bank's BaNCS24 Software Solution ReportDocument27 pagesAllahabad Bank's BaNCS24 Software Solution Reportsanchit_hNo ratings yet

- Core Banking Solutions: Andhra Pradesh Grameena Vikas Bank Head Office, WarangalDocument8 pagesCore Banking Solutions: Andhra Pradesh Grameena Vikas Bank Head Office, WarangalleenardniNo ratings yet

- CBS Navigation MenuDocument34 pagesCBS Navigation MenuShailaja Thakur67% (6)

- 01.13 ClearingDocument38 pages01.13 Clearingmevrick_guy0% (1)

- NPA Date Tracking and Interest CalculationDocument9 pagesNPA Date Tracking and Interest CalculationBaideheeNo ratings yet

- NPA BookletDocument13 pagesNPA BookletBaidehee100% (2)

- Npa Status Through Short Enquiry: Menu Navigation For Npa inDocument11 pagesNpa Status Through Short Enquiry: Menu Navigation For Npa inBaidehee0% (3)

- Deposit Accounts - Joint Accounts and NomineesDocument30 pagesDeposit Accounts - Joint Accounts and Nomineesmevrick_guyNo ratings yet

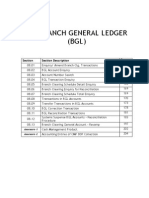

- 01 08-BGLDocument40 pages01 08-BGLmevrick_guy100% (2)

- Union Bank of India's Core Banking SystemDocument36 pagesUnion Bank of India's Core Banking SystemRakesh Prabhakar Shrivastava100% (2)

- GLIFDocument38 pagesGLIFTigmarashmi MahantaNo ratings yet

- 01.09-User System ManagementDocument12 pages01.09-User System Managementmevrick_guyNo ratings yet

- Transaction Processing: Cash, Cheques, TransfersDocument23 pagesTransaction Processing: Cash, Cheques, Transfersmevrick_guyNo ratings yet

- Core Banking SystemDocument37 pagesCore Banking Systemanilreddy143100% (2)

- 01 07-VpisDocument19 pages01 07-Vpishell_hello11No ratings yet

- Finacle CRMDocument12 pagesFinacle CRMNitika Gupta100% (1)

- FinacleDocument129 pagesFinacleShobhit Undefined Fundamentally89% (28)

- Core Banking System in SBIDocument4 pagesCore Banking System in SBINilesh Chandra Sinha92% (12)

- Finacle Version 10 User ManualDocument2 pagesFinacle Version 10 User ManualAkshay BhargavaNo ratings yet

- Opening of A Loan AccountDocument13 pagesOpening of A Loan Accountanilvaddi100% (2)

- 8 To 8 Functionality: Section Section DescriptionDocument7 pages8 To 8 Functionality: Section Section Descriptionmevrick_guyNo ratings yet

- Finacle Software User Manual PDFDocument4 pagesFinacle Software User Manual PDFAMARA JENA0% (7)

- Sfms-Neft 2011Document56 pagesSfms-Neft 2011VivekNo ratings yet

- Core BankingDocument12 pagesCore BankingPriyanka GovalkarNo ratings yet

- Workshop On FinacleDocument41 pagesWorkshop On Finaclemurali420100% (1)

- SBI Core BankingDocument47 pagesSBI Core Bankingsarthak_ganguly78% (9)

- 00.02-List of ChaptersDocument2 pages00.02-List of Chaptersashi9812No ratings yet

- Tcs Bancs On SbiDocument9 pagesTcs Bancs On SbiSushil GoyalNo ratings yet

- Core Banking Solution (Final)Document30 pagesCore Banking Solution (Final)prashant jha100% (1)

- Online Banking SystemDocument21 pagesOnline Banking Systemठाकुर हरिशंकर50% (2)

- 01.03-Deposit Accounts OpeningDocument38 pages01.03-Deposit Accounts Openingmevrick_guy0% (1)

- Rtgs-Neft 10xDocument13 pagesRtgs-Neft 10xDharmavir Singh GautamNo ratings yet

- Finacle 100 QueDocument13 pagesFinacle 100 QuesiddNo ratings yet

- TCS BaNCS End User Report User Manual Ver 2.0Document59 pagesTCS BaNCS End User Report User Manual Ver 2.0DJ MitchNo ratings yet

- 01.20 Government BusinessDocument48 pages01.20 Government Businessmevrick_guyNo ratings yet

- UPI PSP Apps Guide for Payment Service ProvidersDocument1 pageUPI PSP Apps Guide for Payment Service ProvidersAnonymous igVRM2mA6kNo ratings yet

- Core BankingDocument14 pagesCore Bankingpreethygopala75% (4)

- Finacle UsermanualDocument55 pagesFinacle UsermanualNareshaasatNo ratings yet

- User Manual: Intellect Core Banking System (CBS)Document50 pagesUser Manual: Intellect Core Banking System (CBS)tempo100% (5)

- Internet Banking SystemDocument11 pagesInternet Banking SystemKamal KishoreNo ratings yet

- Mobile Banking with WAPDocument46 pagesMobile Banking with WAPram73110No ratings yet

- Srs On Online Banking SystemDocument17 pagesSrs On Online Banking Systemshivasaxena9990% (1)

- Sr. No. Particulars AnnexureDocument18 pagesSr. No. Particulars AnnexureSrinivasan IyerNo ratings yet

- Finacle SettingDocument2 pagesFinacle Settingersukhdevchd2836No ratings yet

- Finacle Core Banking SolutionDocument8 pagesFinacle Core Banking SolutionInfosysNo ratings yet

- Bank Management System in VB 6Document30 pagesBank Management System in VB 6yusuf habibNo ratings yet

- 01.12 Posting RestrictionsDocument14 pages01.12 Posting Restrictionsmevrick_guyNo ratings yet

- Manage cash workflow and transactionsDocument21 pagesManage cash workflow and transactionsmevrick_guyNo ratings yet

- Signature Scanning and Verification in FinacleDocument5 pagesSignature Scanning and Verification in FinacleRahul Yadav70% (20)

- Srs For Bank Management SystemDocument40 pagesSrs For Bank Management SystemWWE OFFICAL MATCH CARDS.No ratings yet

- Core Banking ProjectDocument25 pagesCore Banking ProjectKamlesh Negi55% (11)

- LMSB1Document19 pagesLMSB1Manasa PNo ratings yet

- Cbi BankDocument81 pagesCbi BankVaibhavKamble100% (1)

- Online Banking System for Customer ManagementDocument52 pagesOnline Banking System for Customer ManagementDevesh Agnihotri100% (1)

- MCA Synopsis MCS-044Document92 pagesMCA Synopsis MCS-044BK Ravi Kumar43% (7)

- Study of Online Services Offered by BanksDocument34 pagesStudy of Online Services Offered by Bankssarvesh dhatrakNo ratings yet

- Bhushan Patil Bank Management SystemDocument56 pagesBhushan Patil Bank Management SystemPimpri39Abhishek GaikwadNo ratings yet

- Smart Home Automation Using AndroidDocument8 pagesSmart Home Automation Using Androidultimatekp144100% (1)

- Bill Summary - 121st - A - BillDocument1 pageBill Summary - 121st - A - BillShamal KambleNo ratings yet

- The Constitution of The United StatesDocument21 pagesThe Constitution of The United StatesJeff PrattNo ratings yet

- Oil CrisisDocument15 pagesOil CrisisArihant PawariyaNo ratings yet

- State by State Voucher ComparisonDocument11 pagesState by State Voucher ComparisonArihant PawariyaNo ratings yet

- Forex MarketDocument8 pagesForex MarketArihant PawariyaNo ratings yet

- Smart Homes For A Better Living Using BluetoothDocument4 pagesSmart Homes For A Better Living Using BluetoothInternational Journal of Research in Engineering and Technology100% (1)

- The Constitution of The United StatesDocument21 pagesThe Constitution of The United StatesJeff PrattNo ratings yet

- Android Home AppliDocument5 pagesAndroid Home AppliGaurav GaikwadNo ratings yet

- Data StructureDocument36 pagesData Structureapi-3853475No ratings yet

- Capital FlowDocument7 pagesCapital FlowArihant PawariyaNo ratings yet

- Chapter 0Document2 pagesChapter 0Arihant PawariyaNo ratings yet

- One Vs GroupDocument1 pageOne Vs GroupArihant PawariyaNo ratings yet

- High Capacity Colored Two Dimensional Codes: Antonio Grillo, Alessandro Lentini, Marco Querini and Giuseppe F. ItalianoDocument8 pagesHigh Capacity Colored Two Dimensional Codes: Antonio Grillo, Alessandro Lentini, Marco Querini and Giuseppe F. ItalianoArihant PawariyaNo ratings yet

- Best of Quora - 2012Document442 pagesBest of Quora - 2012Arda KutsalNo ratings yet

- Comparing AlgorithmsDocument38 pagesComparing AlgorithmsArihant PawariyaNo ratings yet

- Online Voting SystemDocument37 pagesOnline Voting SystemArihant Pawariya83% (6)

- 794713132491542Document6 pages794713132491542Arihant PawariyaNo ratings yet

- UPSC Civil Services Exam SyllabusDocument231 pagesUPSC Civil Services Exam Syllabusvssridhar99100% (1)

- Online Voting System GuideDocument20 pagesOnline Voting System GuideArihant PawariyaNo ratings yet

- Cs2352 PCD Unit1 NotesDocument11 pagesCs2352 PCD Unit1 NotesArihant PawariyaNo ratings yet

- UPSC Civil Services Exam SyllabusDocument231 pagesUPSC Civil Services Exam Syllabusvssridhar99100% (1)

- The No Child Left Behind Act of 2001 and The Pathways To College Network FrameworkDocument10 pagesThe No Child Left Behind Act of 2001 and The Pathways To College Network FrameworkArihant PawariyaNo ratings yet

- CornellsystemDocument1 pageCornellsystemapi-253788473No ratings yet

- Members of 16 Lok SabhaDocument62 pagesMembers of 16 Lok SabhaArihant PawariyaNo ratings yet

- Hobsbawm-The Age of EmpireDocument440 pagesHobsbawm-The Age of EmpireAnirban Paul100% (2)

- Kashmir Peace PollDocument149 pagesKashmir Peace PollArihant PawariyaNo ratings yet

- CornellsystemDocument1 pageCornellsystemapi-253788473No ratings yet

- International trade guide to letters of credit and financingDocument17 pagesInternational trade guide to letters of credit and financingSumayra RahmanNo ratings yet

- A Summary of Your Relationship/s With Us:: Alex PrabhuDocument11 pagesA Summary of Your Relationship/s With Us:: Alex PrabhuArvind HarikrishnanNo ratings yet

- Glossary of Financial Terms English Traditional ChineseDocument160 pagesGlossary of Financial Terms English Traditional ChinesehwmawNo ratings yet

- Mishkin 6ce TB Ch08Document29 pagesMishkin 6ce TB Ch08JaeDukAndrewSeoNo ratings yet

- BCCBDocument104 pagesBCCBPrashanth Gowda100% (3)

- HP Analyst ReportDocument11 pagesHP Analyst Reportjoycechan879827No ratings yet

- ICC Users Handbook For Documentary Credits Under UCP 600 PDFDocument10 pagesICC Users Handbook For Documentary Credits Under UCP 600 PDFnmhiri80% (10)

- A Study On Credit Management of Sahayogi Bikas Bank LTDDocument31 pagesA Study On Credit Management of Sahayogi Bikas Bank LTDShivam KarnNo ratings yet

- Habib and Padayachee - 2000 - Economic Policy and Power Relations in South AfricaDocument19 pagesHabib and Padayachee - 2000 - Economic Policy and Power Relations in South AfricaBasanda Nondlazi100% (1)

- Security DB by LinkedinDocument2 pagesSecurity DB by LinkedinNazim KhanNo ratings yet

- Format 1st Board of Trustees MeetingDocument6 pagesFormat 1st Board of Trustees MeetingemptyTV IndiaNo ratings yet

- Ific BankDocument95 pagesIfic BankAl AminNo ratings yet

- Sample MoaDocument7 pagesSample MoaKool GuyNo ratings yet

- Calculate Savings, Loans, Annuities and Present/Future ValuesDocument1 pageCalculate Savings, Loans, Annuities and Present/Future ValuesNaveed NawazNo ratings yet

- Sources of Business Finance ExplainedDocument39 pagesSources of Business Finance ExplainedCarry MinatiNo ratings yet

- Risk Management - Sample QuestionsDocument11 pagesRisk Management - Sample QuestionsSandeep Spartacus100% (1)

- A PROJECT REPORT ON HDFC BANK Submiited by Ankita SinghDocument29 pagesA PROJECT REPORT ON HDFC BANK Submiited by Ankita SinghBHRIGURASHAN 16588% (94)

- Navi Consumer Loans Case SubmissionDocument4 pagesNavi Consumer Loans Case SubmissionABHIRAM MOLUGUNo ratings yet

- NON COMPETE CLAUSE PLJ Volume 83 Number 2 - 04 - Charito R. Villena PDFDocument28 pagesNON COMPETE CLAUSE PLJ Volume 83 Number 2 - 04 - Charito R. Villena PDFHeart Lero100% (1)

- Summer Training Report On Mas FinanceDocument73 pagesSummer Training Report On Mas FinanceHimanshu Singh TanwarNo ratings yet

- The Legal Framework of The Philippine Banking System: Atty. Elmore O. CapuleDocument114 pagesThe Legal Framework of The Philippine Banking System: Atty. Elmore O. CapuleMakoy BixenmanNo ratings yet

- Small Scale IndustriesDocument28 pagesSmall Scale IndustriesMohit Gupta25% (4)

- Pre ClosestatementDocument2 pagesPre Closestatementkhurafaat inNo ratings yet

- LITERATURE REVIEW ON ASSET-LIABILITY MANAGEMENTDocument9 pagesLITERATURE REVIEW ON ASSET-LIABILITY MANAGEMENTAnkur Upadhyay0% (1)

- Form 3CBDocument12 pagesForm 3CBpriya sharmaNo ratings yet

- General Insurance-Big Benefit But OverburdenedDocument59 pagesGeneral Insurance-Big Benefit But OverburdenedChandra UddhatayudhaNo ratings yet

- Guide To Big Data For FinanceDocument14 pagesGuide To Big Data For FinancePedro Alam SargesNo ratings yet

- Ds Team D Group ProjectDocument57 pagesDs Team D Group ProjectRenuka Badhoria (HRM 21-23)No ratings yet

- Sewale Bitew PDFDocument84 pagesSewale Bitew PDFTILAHUNNo ratings yet

- PT Bank Rakyat Indonesia (Persero)Document380 pagesPT Bank Rakyat Indonesia (Persero)RyanSoetopoNo ratings yet

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)