You might also like

- Makerere University College of Business and Management Studies Master of Business AdministrationDocument15 pagesMakerere University College of Business and Management Studies Master of Business AdministrationDamulira DavidNo ratings yet

- Income Tax Guide UgandaDocument13 pagesIncome Tax Guide UgandaMoses LubangakeneNo ratings yet

- Accounting Rate of ReturnDocument3 pagesAccounting Rate of ReturnDeep Debnath100% (1)

- Chapter 5 - Globalization & SocietyDocument18 pagesChapter 5 - Globalization & SocietyAnonymous cwC8kTyNo ratings yet

- Net Present ValueDocument8 pagesNet Present ValueDagnachew Amare DagnachewNo ratings yet

- The Internal Environment Resources, Capabilities, and Core CompetenciesDocument41 pagesThe Internal Environment Resources, Capabilities, and Core CompetenciesMahmudur Rahman50% (4)

- Capital StructureDocument24 pagesCapital StructureSiddharth GautamNo ratings yet

- Investment Appraisal Techniques 2Document24 pagesInvestment Appraisal Techniques 2Jul 480wesh100% (1)

- Capital Budgeting FinalDocument78 pagesCapital Budgeting FinalHarnitNo ratings yet

- "Payback Period" Important in Capital Budgeting DecisionsDocument46 pages"Payback Period" Important in Capital Budgeting DecisionsNivesh Maheshwari88% (8)

- Risk and ReturnDocument31 pagesRisk and ReturnKhushbakht FarrukhNo ratings yet

- Buisness CycleDocument8 pagesBuisness CycleyagyatiwariNo ratings yet

- R30 Long Lived AssetsDocument33 pagesR30 Long Lived AssetsSiddhu Sai100% (1)

- Lesson: 7 Cost of CapitalDocument22 pagesLesson: 7 Cost of CapitalEshaan ChadhaNo ratings yet

- Taxation of Business IncomeDocument15 pagesTaxation of Business Incomekitderoger_391648570No ratings yet

- Introduction To Corporate GovernanceDocument26 pagesIntroduction To Corporate GovernanceLeah BallesterosNo ratings yet

- Time Value of MoneyDocument55 pagesTime Value of MoneySayoni GhoshNo ratings yet

- Case QuestionsDocument5 pagesCase QuestionsJohn Patrick Tolosa NavarroNo ratings yet

- Comparative Vs Competitive AdvantageDocument19 pagesComparative Vs Competitive AdvantageSuntari CakSoenNo ratings yet

- Portfolio Management-Module One Discussion - MandoDocument2 pagesPortfolio Management-Module One Discussion - MandoDavid Luko ChifwaloNo ratings yet

- Resume Journal A Study On Capital Budgeting Practices of Some Selected Companies in BangladeshDocument5 pagesResume Journal A Study On Capital Budgeting Practices of Some Selected Companies in Bangladeshfarah_pawestriNo ratings yet

- Financial Ratio AnalysisDocument4 pagesFinancial Ratio AnalysisJennineNo ratings yet

- Capital Structure Theories NotesDocument9 pagesCapital Structure Theories NotesSoumendra RoyNo ratings yet

- Chapter 2Document5 pagesChapter 2Sundaramani SaranNo ratings yet

- Autocratic ModelDocument5 pagesAutocratic ModelVenkatesh KesavanNo ratings yet

- Long Term Sources of FinanceDocument26 pagesLong Term Sources of FinancemustafakarimNo ratings yet

- Chapter-17-LBO MergerDocument69 pagesChapter-17-LBO MergerSami Jatt0% (1)

- Session11 - Bond Analysis Structure and ContentsDocument18 pagesSession11 - Bond Analysis Structure and ContentsJoe Garcia100% (1)

- Cost ConceptsDocument24 pagesCost ConceptsAshish MathewNo ratings yet

- Accounting Dissertation Proposal-Example 1Document24 pagesAccounting Dissertation Proposal-Example 1idkolaNo ratings yet

- BIF Capital StructureDocument13 pagesBIF Capital Structuresagar_funkNo ratings yet

- 13corporate Social Responsibility in International BusinessDocument23 pages13corporate Social Responsibility in International BusinessShruti SharmaNo ratings yet

- Ethical Behaviour in Business PDFDocument2 pagesEthical Behaviour in Business PDFChanceNo ratings yet

- CHAPTER 5.overview of Risk and ReturnDocument61 pagesCHAPTER 5.overview of Risk and ReturnDimple EstacioNo ratings yet

- Cost of CapitalDocument12 pagesCost of CapitalAbdii DhufeeraNo ratings yet

- Introduction To Credit ManagementDocument48 pagesIntroduction To Credit ManagementHakdog KaNo ratings yet

- Transfer PricingDocument37 pagesTransfer PricingVenn Bacus RabadonNo ratings yet

- Capital StructureDocument42 pagesCapital Structurevarsha raichalNo ratings yet

- Bond Yield and Price PDFDocument2 pagesBond Yield and Price PDFps12hayNo ratings yet

- Toyota Product RecallDocument1 pageToyota Product RecallJunegil FabularNo ratings yet

- Short Run Decision Making: Relevant CostingDocument47 pagesShort Run Decision Making: Relevant CostingSuptoNo ratings yet

- Forex - Problems in Exchange RateDocument26 pagesForex - Problems in Exchange Rateyawehnew23No ratings yet

- Mixed Cost High-Low Method ProblemDocument1 pageMixed Cost High-Low Method ProblemAnj HwanNo ratings yet

- Consolidated Financial StatementsDocument7 pagesConsolidated Financial StatementsParvez NahidNo ratings yet

- Responsibility Accounting and Transfer PricingDocument4 pagesResponsibility Accounting and Transfer PricingMerlita TuralbaNo ratings yet

- To Be An Observer in The Universe and Make A DifferenceDocument2 pagesTo Be An Observer in The Universe and Make A DifferenceShelly Mae SiguaNo ratings yet

- The Role of Finacial ManagementDocument25 pagesThe Role of Finacial Managementnitinvohra_capricorn100% (1)

- Analysis and Interpretation of FS-Part 1Document2 pagesAnalysis and Interpretation of FS-Part 1Rhea RamirezNo ratings yet

- Production TheoryDocument92 pagesProduction TheoryGoutam Reddy100% (3)

- Some Exercises On Capital Structure and Dividend PolicyDocument3 pagesSome Exercises On Capital Structure and Dividend PolicyAdi AliNo ratings yet

- Dividend PolicyDocument44 pagesDividend PolicyShahNawazNo ratings yet

- Differential Cost Analysis PDFDocument4 pagesDifferential Cost Analysis PDFVivienne Lei BolosNo ratings yet

- Leverage PPTDocument13 pagesLeverage PPTamdNo ratings yet

- ABC Costing Lecture NotesDocument12 pagesABC Costing Lecture NotesMickel AlexanderNo ratings yet

- Lesson 22 Capital Structure TheoriesDocument6 pagesLesson 22 Capital Structure TheoriesSana Ur Rehman100% (1)

- Interest Rates and Their Role in FinanceDocument17 pagesInterest Rates and Their Role in FinanceClyden Jaile RamirezNo ratings yet

- ADocument7 pagesATân NguyênNo ratings yet

- AssigmentDocument19 pagesAssigmentTân NguyênNo ratings yet

- Punjab Agricultural UniversityDocument6 pagesPunjab Agricultural UniversitySheetal NagpalNo ratings yet

- Ate Bec EssayDocument17 pagesAte Bec EssayMaria ClaraNo ratings yet

- Flexibility Business Performance P2.2Document23 pagesFlexibility Business Performance P2.2Kelly HermanNo ratings yet

- HNCD Business Unit Resource ListDocument52 pagesHNCD Business Unit Resource ListSwati RaghupatruniNo ratings yet

- HNCD Business Unit Resource ListDocument52 pagesHNCD Business Unit Resource ListSwati RaghupatruniNo ratings yet

- Questions-Training and Development ExamDocument9 pagesQuestions-Training and Development ExamKelly Herman100% (6)

- Contractual Liability and Tort Liability: Todea Al., Oroian I., L. HolonecDocument5 pagesContractual Liability and Tort Liability: Todea Al., Oroian I., L. HolonecMohammed Shah WasiimNo ratings yet

- Ch.12 - 13ed Fin Planning & ForecastingMasterDocument47 pagesCh.12 - 13ed Fin Planning & ForecastingMasterKelly HermanNo ratings yet

- Pearson BTEC Level 5 HND Diploma in Business Sample AssignmentDocument9 pagesPearson BTEC Level 5 HND Diploma in Business Sample AssignmentSanyam Tiwari50% (2)

- The Effects of IFRS Adoption On Taxation in NigeriDocument15 pagesThe Effects of IFRS Adoption On Taxation in NigeriJoseph OlugbamiNo ratings yet

- Name Suhail Abdul Rashid TankeDocument9 pagesName Suhail Abdul Rashid TankeIram ParkarNo ratings yet

- Cost Accounting 1 8 FinalDocument16 pagesCost Accounting 1 8 FinalAsdfghjkl LkjhgfdsaNo ratings yet

- Week 1-9 JSS3 AGRICDocument7 pagesWeek 1-9 JSS3 AGRICopeyemiquad123No ratings yet

- Annual Report - 2020 - Linde Bangladesh BOCDocument90 pagesAnnual Report - 2020 - Linde Bangladesh BOCAtiqul islamNo ratings yet

- IAS 16 PPE and IAS 40Document81 pagesIAS 16 PPE and IAS 40esulawyer2001No ratings yet

- Advanced Financial Management Test 1 May 2024 Solution 1701932012Document15 pagesAdvanced Financial Management Test 1 May 2024 Solution 1701932012shauryagupta20013007No ratings yet

- Assignment 2023 For BPOI - 105 (005) (DBPOFA Prog)Document1 pageAssignment 2023 For BPOI - 105 (005) (DBPOFA Prog)Pawar ComputerNo ratings yet

- Kotak Security Intenship ReportDocument34 pagesKotak Security Intenship ReportEk Deewana RajNo ratings yet

- Common Size Income StatementDocument7 pagesCommon Size Income StatementUSD 654No ratings yet

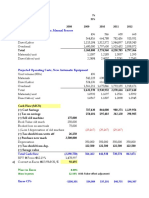

- Projected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Document4 pagesProjected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Cesar CameyNo ratings yet

- Ar 2010Document443 pagesAr 2010Dennis AngNo ratings yet

- Finance - WS2Document2 pagesFinance - WS2ElenaNo ratings yet

- Case Studies in Financial Management PDFDocument2 pagesCase Studies in Financial Management PDFGrand Overall100% (2)

- 3 Calculation of Daily Exchange PositionDocument10 pages3 Calculation of Daily Exchange PositionTalha AdilNo ratings yet

- BBA VI TH Sem Financial Institution & MarketsDocument2 pagesBBA VI TH Sem Financial Institution & MarketsJordan ThapaNo ratings yet

- WorkDocument52 pagesWorksara anjumNo ratings yet

- B Liquid Yield Option NoteDocument2 pagesB Liquid Yield Option NoteDanica BalinasNo ratings yet

- NUST Business School: Introduction To Operations Management - OTM 351 Assignment 3Document7 pagesNUST Business School: Introduction To Operations Management - OTM 351 Assignment 3Zainab AftabNo ratings yet

- Uts AKM IIIDocument2 pagesUts AKM IIISekar Wulan OktaviaNo ratings yet

- Jurnal Audit Laporan KeuanganDocument20 pagesJurnal Audit Laporan KeuanganSalmiNo ratings yet

- Butler Excel Sheets (Group 2)Document11 pagesButler Excel Sheets (Group 2)Nathan ClarkinNo ratings yet

- Pfrs For Smes Full PFRS: Same Same Same SameDocument14 pagesPfrs For Smes Full PFRS: Same Same Same SameAnthon GarciaNo ratings yet

- BFD Test 1 With Solution Jun 2023 ST AcademyDocument10 pagesBFD Test 1 With Solution Jun 2023 ST AcademyHassan AzamNo ratings yet

- Course Pack For AgBus 174 Investment Management Module 1Document31 pagesCourse Pack For AgBus 174 Investment Management Module 1Mark Ramon MatugasNo ratings yet

- Chapter 10Document13 pagesChapter 10Wasim Bin ArshadNo ratings yet

- DBB2104 Unit-08Document24 pagesDBB2104 Unit-08anamikarajendran441998No ratings yet

- Bram 2016Document270 pagesBram 2016Frederick SimanjuntakNo ratings yet

- Cost of Capital: Dr. A.N. SAHDocument41 pagesCost of Capital: Dr. A.N. SAHHARMANDEEP SINGHNo ratings yet

- Chapter 10 Part A and Part B ReviewDocument9 pagesChapter 10 Part A and Part B ReviewNhi HoNo ratings yet