You might also like

- Abs Cdos - A Primer: StrategyDocument28 pagesAbs Cdos - A Primer: StrategyjigarchhatrolaNo ratings yet

- The Securitization Markets Handbook: Structures and Dynamics of Mortgage- and Asset-backed SecuritiesFrom EverandThe Securitization Markets Handbook: Structures and Dynamics of Mortgage- and Asset-backed SecuritiesNo ratings yet

- The Mechanics of Securitization: A Practical Guide to Structuring and Closing Asset-Backed Security TransactionsFrom EverandThe Mechanics of Securitization: A Practical Guide to Structuring and Closing Asset-Backed Security TransactionsNo ratings yet

- Ginnie Mae 2007 Bank of America PrimerDocument37 pagesGinnie Mae 2007 Bank of America PrimerJylly Jakes100% (2)

- JPM MBS Primer PDFDocument68 pagesJPM MBS Primer PDFAndy LeungNo ratings yet

- (Bank of America) Hybrid ARM MBS - Valuation and Risk MeasuresDocument22 pages(Bank of America) Hybrid ARM MBS - Valuation and Risk Measures00aaNo ratings yet

- RMBS Trading Desk Strategy Guide to IO/PO SecuritiesDocument29 pagesRMBS Trading Desk Strategy Guide to IO/PO SecuritiesDimitri DelisNo ratings yet

- Barclays DUS Primer 3-9-2011Document11 pagesBarclays DUS Primer 3-9-2011pratikmhatre123No ratings yet

- Introduction To Specified Pool SectorDocument15 pagesIntroduction To Specified Pool Sectormoveld100% (2)

- Guide To European CMBSDocument53 pagesGuide To European CMBSUpendra Choudhary100% (1)

- RMBS Trading Desk Strategy on Agency ARM MBS PrepaymentsDocument11 pagesRMBS Trading Desk Strategy on Agency ARM MBS PrepaymentsJay KabNo ratings yet

- Nomura CDS Primer 12may04Document12 pagesNomura CDS Primer 12may04Ethan Sun100% (1)

- Forward Rate BiasDocument9 pagesForward Rate BiasHafsa Hina100% (2)

- Valuation of Inverse IOs and Other MBS DerivativesDocument12 pagesValuation of Inverse IOs and Other MBS DerivativesgoldboxNo ratings yet

- CMBS Special Topic: Outlook For The CMBS Market in 2011Document26 pagesCMBS Special Topic: Outlook For The CMBS Market in 2011Yihai YuNo ratings yet

- Explaining The Lehman Brothers Option Adjusted Spread of A Corporate Bond - Claus PedersenDocument20 pagesExplaining The Lehman Brothers Option Adjusted Spread of A Corporate Bond - Claus PedersentradingmycroftNo ratings yet

- Lehman Brothers NonAgency Hybrids A PrimerDocument16 pagesLehman Brothers NonAgency Hybrids A PrimerMatthew HartNo ratings yet

- Cds PrimerDocument15 pagesCds PrimerJay KabNo ratings yet

- No1 Rock-Bottom SpreadsDocument100 pagesNo1 Rock-Bottom Spreadsianseow100% (1)

- JP Morgan Fixed Income Correlation Trading Using SwaptionsDocument7 pagesJP Morgan Fixed Income Correlation Trading Using Swaptionscoolacl100% (2)

- (Lehman) O'Kane Turnbull (2003) Valuation of CDSDocument19 pages(Lehman) O'Kane Turnbull (2003) Valuation of CDSGabriel PangNo ratings yet

- JPM Bond CDS Basis Handb 2009-02-05 263815Document92 pagesJPM Bond CDS Basis Handb 2009-02-05 263815ccohen6410100% (1)

- JPM MBS PrimerDocument68 pagesJPM MBS PrimerJerry ChenNo ratings yet

- Valuation and Hedging of Inv Floaters PDFDocument4 pagesValuation and Hedging of Inv Floaters PDFtiwariaradNo ratings yet

- Outlook For The RMBS Market in 2007Document45 pagesOutlook For The RMBS Market in 2007Dimitri DelisNo ratings yet

- Asset Swaps to Z-spreads: An Introduction to Swaps, Present Values, and Z-SpreadsDocument20 pagesAsset Swaps to Z-spreads: An Introduction to Swaps, Present Values, and Z-SpreadsAudrey Lim100% (1)

- Class 23: Fixed Income, Interest Rate SwapsDocument21 pagesClass 23: Fixed Income, Interest Rate SwapsKarya BangunanNo ratings yet

- Repos A Deep Dive in The Collateral PoolDocument7 pagesRepos A Deep Dive in The Collateral PoolppateNo ratings yet

- Agencies JPMDocument18 pagesAgencies JPMbonefish212No ratings yet

- Constructing A Liability Hedging Portfolio PDFDocument24 pagesConstructing A Liability Hedging Portfolio PDFtachyon007_mechNo ratings yet

- Collateralized Mortgage Obligations: An Introduction To Sequentials, Pacs, Tacs, and VadmsDocument5 pagesCollateralized Mortgage Obligations: An Introduction To Sequentials, Pacs, Tacs, and Vadmsddelis77No ratings yet

- IR - Quant - 101105 - Is It Possible To Reconcile Caplet and Swaption MarketsDocument31 pagesIR - Quant - 101105 - Is It Possible To Reconcile Caplet and Swaption MarketsC W YongNo ratings yet

- Learning from interest rate implied volatilitiesDocument85 pagesLearning from interest rate implied volatilitiesbobmezzNo ratings yet

- Eric Sorensen - The Salomon Smith BaDocument188 pagesEric Sorensen - The Salomon Smith Bajbiddy789No ratings yet

- CMS Inverse FloatersDocument8 pagesCMS Inverse FloaterszdfgbsfdzcgbvdfcNo ratings yet

- (Lehman Brothers) Securitized Products Outlook 2007 - Bracing For A Credit DownturnDocument23 pages(Lehman Brothers) Securitized Products Outlook 2007 - Bracing For A Credit DownturnSiddhantNo ratings yet

- Hedging Illiquid AssetsDocument16 pagesHedging Illiquid Assetspenfoul29No ratings yet

- (Citibank) Using Asset Swap Spreads To Identify Goverment Bond Relative-ValueDocument12 pages(Citibank) Using Asset Swap Spreads To Identify Goverment Bond Relative-ValueMert Can GencNo ratings yet

- Yieldbook LMM Term ModelDocument20 pagesYieldbook LMM Term Modelphilline2009100% (1)

- Reverse Mortgage Primer - BOFA 2006Document24 pagesReverse Mortgage Primer - BOFA 2006ab3rdNo ratings yet

- Bank of America Trust IOPO MarketDocument29 pagesBank of America Trust IOPO Marketsss1453No ratings yet

- (Bank of America) Pricing Mortgage-Back SecuritiesDocument22 pages(Bank of America) Pricing Mortgage-Back Securitiesbhartia2512100% (4)

- Fixed Income Relative Value Analysis: A Practitioners Guide to the Theory, Tools, and TradesFrom EverandFixed Income Relative Value Analysis: A Practitioners Guide to the Theory, Tools, and TradesNo ratings yet

- Financial Soundness Indicators for Financial Sector Stability in Viet NamFrom EverandFinancial Soundness Indicators for Financial Sector Stability in Viet NamNo ratings yet

- Life Settlements and Longevity Structures: Pricing and Risk ManagementFrom EverandLife Settlements and Longevity Structures: Pricing and Risk ManagementNo ratings yet

- The Handbook of Convertible Bonds: Pricing, Strategies and Risk ManagementFrom EverandThe Handbook of Convertible Bonds: Pricing, Strategies and Risk ManagementNo ratings yet

- Trading the Fixed Income, Inflation and Credit Markets: A Relative Value GuideFrom EverandTrading the Fixed Income, Inflation and Credit Markets: A Relative Value GuideNo ratings yet

- The CME Group Risk Management Handbook: Products and ApplicationsFrom EverandThe CME Group Risk Management Handbook: Products and ApplicationsNo ratings yet

- Introduction to Fixed Income Analytics: Relative Value Analysis, Risk Measures and ValuationFrom EverandIntroduction to Fixed Income Analytics: Relative Value Analysis, Risk Measures and ValuationNo ratings yet

- Credit Securitisations and Derivatives: Challenges for the Global MarketsFrom EverandCredit Securitisations and Derivatives: Challenges for the Global MarketsNo ratings yet

- CLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketFrom EverandCLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketNo ratings yet

- Inside the Yield Book: The Classic That Created the Science of Bond AnalysisFrom EverandInside the Yield Book: The Classic That Created the Science of Bond AnalysisRating: 3 out of 5 stars3/5 (1)

- Loan Application Form and DocumentsDocument2 pagesLoan Application Form and DocumentsSoowhysoo Twoonel100% (2)

- Section "A" Very Short Answer Questions) (Attempt All Questions)Document5 pagesSection "A" Very Short Answer Questions) (Attempt All Questions)Ayusha TimalsinaNo ratings yet

- General Power Attorney 40 CharactersDocument2 pagesGeneral Power Attorney 40 CharactersJudy SyjucoNo ratings yet

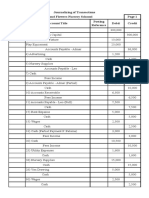

- Journalizing Transaction (Ezekiel Lapitan)Document3 pagesJournalizing Transaction (Ezekiel Lapitan)Ezekiel LapitanNo ratings yet

- Control of The Money SupplyDocument2 pagesControl of The Money SupplyMario SarayarNo ratings yet

- Metro-Score PPI: Customer Credit ReportDocument5 pagesMetro-Score PPI: Customer Credit ReportPastor Roy Onyancha CyberNo ratings yet

- These Materials Were Produced For Insidesherpa and To Be Used For Educational and Training Purposes OnlyDocument2 pagesThese Materials Were Produced For Insidesherpa and To Be Used For Educational and Training Purposes OnlyTech Dealer50% (2)

- A Comparative Study of Mutual Fund Schemes of State Bank of India and Unit Trust of IndiaDocument9 pagesA Comparative Study of Mutual Fund Schemes of State Bank of India and Unit Trust of IndiaAman WadhwaNo ratings yet

- Module-Intermediate Accounting 1-LM01-CP1 PDFDocument25 pagesModule-Intermediate Accounting 1-LM01-CP1 PDFNikka Rebaya100% (1)

- Instructions:: Please Read The Following Instructions Carefully Before Attempting Any QuestionDocument9 pagesInstructions:: Please Read The Following Instructions Carefully Before Attempting Any QuestionNumanNo ratings yet

- Internship Report: Janata Bank Limited and Its General Banking ActivitiesDocument54 pagesInternship Report: Janata Bank Limited and Its General Banking ActivitiesMehedi HasanNo ratings yet

- Pace 215-Project B-Demition 1Document6 pagesPace 215-Project B-Demition 1SELYN DEMITIONNo ratings yet

- CTTT - C5 (Eng)Document18 pagesCTTT - C5 (Eng)Tram AnhhNo ratings yet

- Calcutta TelephonesDocument3 pagesCalcutta TelephonessudipNo ratings yet

- Group 4 Assignment Campus Deli 1Document9 pagesGroup 4 Assignment Campus Deli 1namitasharma1512100% (4)

- Capitalization TableDocument10 pagesCapitalization TableDiego OssaNo ratings yet

- AccountingDocument290 pagesAccountingNibash KumuraNo ratings yet

- High Tire PerformanceDocument8 pagesHigh Tire PerformanceSofía MargaritaNo ratings yet

- AARON AIKENS - Oct 2019 PDFDocument6 pagesAARON AIKENS - Oct 2019 PDFbombie bomboxNo ratings yet

- Journal Ledger & Trial BalanceDocument32 pagesJournal Ledger & Trial BalanceMr. Demon ExtraNo ratings yet

- Exercise: The Market For Foreign Exchange: BMFM 33135 Oct 2020Document3 pagesExercise: The Market For Foreign Exchange: BMFM 33135 Oct 2020Sylvia GynNo ratings yet

- Banking-Industry Specific and Regional Economic Determinants of NPL - Evidence From US StateDocument3 pagesBanking-Industry Specific and Regional Economic Determinants of NPL - Evidence From US StateChinthaka PereraNo ratings yet

- April JuneDocument15 pagesApril JuneSanjivNo ratings yet

- 403 PPT-1Document14 pages403 PPT-1NikitaNo ratings yet

- Sunview 2023 Q2Document20 pagesSunview 2023 Q2Quint WongNo ratings yet

- Capital Budgeting PPT 1Document75 pagesCapital Budgeting PPT 1Sakshi SharmaNo ratings yet

- Understanding the Yield CurveDocument14 pagesUnderstanding the Yield CurveAmirNo ratings yet

- Multiple Choice Questions (MCQS) : InstructionsDocument5 pagesMultiple Choice Questions (MCQS) : InstructionsMubashir HussainNo ratings yet

- Damodaran - Trapped CashDocument5 pagesDamodaran - Trapped CashAparajita SharmaNo ratings yet