You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Project ManagementDocument9 pagesProject ManagementNakul SainiNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Money ManagementDocument17 pagesMoney ManagementNakul Saini100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Case Study On Subprime CrisisDocument24 pagesCase Study On Subprime CrisisNakul SainiNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Nakul Presentation1Document28 pagesNakul Presentation1Nakul SainiNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- OCC Cases ConsultingDocument11 pagesOCC Cases ConsultingCritical LinksNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Sem-3 Pol SC - EC ApprovedDocument76 pagesSem-3 Pol SC - EC ApprovedKrishna SharmaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- FTCXSXSXSP - Seminar 8 - AnswersDocument4 pagesFTCXSXSXSP - Seminar 8 - AnswersLewis FergusonNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Handout Case ETGE IIDocument5 pagesHandout Case ETGE IIsdsdasdasdadsadsNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Unit 1: Financial ManagementDocument20 pagesUnit 1: Financial ManagementDisha SareenNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

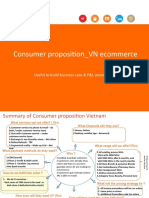

- Consumer Proposition - VN Ecommerce: Useful To Build Business Case & P&L AssumptionsDocument3 pagesConsumer Proposition - VN Ecommerce: Useful To Build Business Case & P&L AssumptionsvuquyhaiNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- CH 10Document34 pagesCH 10PetersonNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- LCM Accounting in P2PDocument4 pagesLCM Accounting in P2Pramthilak2007gmailcomNo ratings yet

- International Marketing Question BankDocument1 pageInternational Marketing Question BankKiara Mp50% (2)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hernandez Cristina - Student Activity Packet Investing UnitDocument23 pagesHernandez Cristina - Student Activity Packet Investing Unitapi-51266945050% (2)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- BoschDocument7 pagesBoschSayan MitraNo ratings yet

- Marketing Strategy Analysis: Biti's Hunter XDocument36 pagesMarketing Strategy Analysis: Biti's Hunter XHoàng Ngọc OanhNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- 00068767Document2 pages00068767Alsalam Yemen pharmaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Buying Decision Process in Rural Marketing PDFDocument14 pagesBuying Decision Process in Rural Marketing PDFShem W LyngdohNo ratings yet

- Cambridge International AS & A Level: ECONOMICS 9708/22Document4 pagesCambridge International AS & A Level: ECONOMICS 9708/22sharmat1963No ratings yet

- A Guide To Understanding Your Public Mutual Account StatementDocument2 pagesA Guide To Understanding Your Public Mutual Account StatementAbu AdilaNo ratings yet

- 1 Ass-2Document13 pages1 Ass-2Kim SooanNo ratings yet

- Engineering Economy TermsDocument4 pagesEngineering Economy TermsOgiNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Take Home ExamDocument6 pagesTake Home Examnadya bujangNo ratings yet

- Deeper Understanding, Faster Calc: SOA MFE and CAS Exam 3F: Yufeng Guo July 5, 2011Document23 pagesDeeper Understanding, Faster Calc: SOA MFE and CAS Exam 3F: Yufeng Guo July 5, 2011Amine HaririNo ratings yet

- Consolidated Bank (Ghana) Limited: Unaudited Summary Financial StatementsDocument2 pagesConsolidated Bank (Ghana) Limited: Unaudited Summary Financial StatementsFuaad DodooNo ratings yet

- A 4 Igcse School: Answer All QuestionsDocument4 pagesA 4 Igcse School: Answer All QuestionsAung Toe OONo ratings yet

- Constantinides 2006Document33 pagesConstantinides 2006Cristian ReyesNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Soal Kuis The Howell CorporationDocument4 pagesSoal Kuis The Howell CorporationTeukuFirhanNo ratings yet

- Marketing Strategies Currently Used by FabindiaDocument8 pagesMarketing Strategies Currently Used by FabindiaSimran singhNo ratings yet

- Review FinalDocument10 pagesReview FinalTj RodriguezNo ratings yet

- Need of Working Capital Adjustment in TPDocument7 pagesNeed of Working Capital Adjustment in TPmasanunNo ratings yet

- Sample Executive SummaryDocument40 pagesSample Executive SummaryRecca Hanabishi100% (3)

- Aaape9984b Q1 2023-24Document10 pagesAaape9984b Q1 2023-24Century Flour Mills Limited Head OfficeNo ratings yet

- Ch-5 - Identifying Market Segments, Targeting & PositioningDocument23 pagesCh-5 - Identifying Market Segments, Targeting & PositioningImran KhaliqNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)