You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Sample 20 Area 1 QDocument5 pagesSample 20 Area 1 QJoeFSabaterNo ratings yet

- ITSC Sample Minutes 2005-06-23mDocument1 pageITSC Sample Minutes 2005-06-23mJoeFSabaterNo ratings yet

- Ch6-2008 CISA ReviewCourseDocument58 pagesCh6-2008 CISA ReviewCourseJoeFSabaterNo ratings yet

- Isaca: The Recognized Global Leaders in IT Governance, Control, Security and AssuranceDocument60 pagesIsaca: The Recognized Global Leaders in IT Governance, Control, Security and AssuranceJoeFSabaterNo ratings yet

- ITGI Global Status Report 2003Document72 pagesITGI Global Status Report 2003JoeFSabaterNo ratings yet

- CISA Practice Questions IT GovernanceDocument4 pagesCISA Practice Questions IT GovernanceJoeFSabaterNo ratings yet

- Routing GambarDocument1 pageRouting GambarJoeFSabaterNo ratings yet

- Chapter 3 - Problems With AnswersDocument31 pagesChapter 3 - Problems With AnswersJoeFSabater100% (1)

- Practice Questions - CISA Area 1Document4 pagesPractice Questions - CISA Area 1JoeFSabaterNo ratings yet

- Business Continuity and Disaster Recovery PlansDocument10 pagesBusiness Continuity and Disaster Recovery PlansJoeFSabaterNo ratings yet

- IT Service Delivery 2008Document11 pagesIT Service Delivery 2008JoeFSabaterNo ratings yet

- IT Strategy CommitteeDocument2 pagesIT Strategy CommitteeJoeFSabaterNo ratings yet

- Routing GambarDocument1 pageRouting GambarJoeFSabaterNo ratings yet

- IT Governance 2008Document7 pagesIT Governance 2008JoeFSabaterNo ratings yet

- CISA Answers Chapter Gov and DelvryDocument2 pagesCISA Answers Chapter Gov and DelvryJoeFSabaterNo ratings yet

- ITSC Sample Minutes 2005-06-23mDocument1 pageITSC Sample Minutes 2005-06-23mJoeFSabaterNo ratings yet

- Question - Ch3 Part2Document4 pagesQuestion - Ch3 Part2JoeFSabaterNo ratings yet

- IT Strat Comm Sample MinutesDocument2 pagesIT Strat Comm Sample MinutesJoeFSabaterNo ratings yet

- Chapter 3 - Problems With AnswersDocument31 pagesChapter 3 - Problems With AnswersJoeFSabater100% (1)

- Chapter 3 Software Testing and Quality Assurance ReviewDocument9 pagesChapter 3 Software Testing and Quality Assurance ReviewJoeFSabaterNo ratings yet

- ITGI Global Status Report 2006Document48 pagesITGI Global Status Report 2006JoeFSabaterNo ratings yet

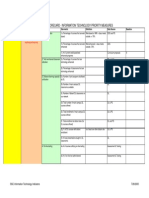

- Balanced Scorecard - Information Technology Priority MeasuresDocument3 pagesBalanced Scorecard - Information Technology Priority MeasuresJoeFSabaterNo ratings yet

- Spelling Bee Word List Grade 2-3 Revised January, 1990Document9 pagesSpelling Bee Word List Grade 2-3 Revised January, 1990travi95No ratings yet

- Mock ExamDocument2 pagesMock ExamJoeFSabaterNo ratings yet

- Manufacturing Financial CostingDocument15 pagesManufacturing Financial CostingJoeFSabaterNo ratings yet

- Brevet LessonsDocument13 pagesBrevet LessonsJoeFSabaterNo ratings yet

- Otoritas Jasa Keuangan ResearchDocument8 pagesOtoritas Jasa Keuangan ResearchJoeFSabaterNo ratings yet

- F3 ACCA Google Books Ch1 Then 8 9 11Document47 pagesF3 ACCA Google Books Ch1 Then 8 9 11JoeFSabaterNo ratings yet

- Corp Governance IndonesiaDocument16 pagesCorp Governance IndonesiaJoeFSabaterNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- GS Ep Cor 356Document7 pagesGS Ep Cor 356SangaranNo ratings yet

- Insulators and Circuit BreakersDocument29 pagesInsulators and Circuit Breakersdilja aravindanNo ratings yet

- Tata Group's Global Expansion and Business StrategiesDocument23 pagesTata Group's Global Expansion and Business Strategiesvgl tamizhNo ratings yet

- Deed of Sale - Motor VehicleDocument4 pagesDeed of Sale - Motor Vehiclekyle domingoNo ratings yet

- BAM PPT 2011-09 Investor Day PDFDocument171 pagesBAM PPT 2011-09 Investor Day PDFRocco HuangNo ratings yet

- Chapter 7 - Cash BudgetDocument23 pagesChapter 7 - Cash BudgetMostafa KaghaNo ratings yet

- Business Case - Uganda Maize Export To South SudanDocument44 pagesBusiness Case - Uganda Maize Export To South SudanInfiniteKnowledge33% (3)

- Difference Between OS1 and OS2 Single Mode Fiber Cable - Fiber Optic Cabling SolutionsDocument2 pagesDifference Between OS1 and OS2 Single Mode Fiber Cable - Fiber Optic Cabling SolutionsDharma Teja TanetiNo ratings yet

- Denial and AR Basic Manual v2Document31 pagesDenial and AR Basic Manual v2Calvin PatrickNo ratings yet

- Supply Chain ManagementDocument30 pagesSupply Chain ManagementSanchit SinghalNo ratings yet

- CFEExam Prep CourseDocument28 pagesCFEExam Prep CourseM50% (4)

- 2022 Product Catalog WebDocument100 pages2022 Product Catalog WebEdinson Reyes ValderramaNo ratings yet

- Growatt SPF3000TL-HVM (2020)Document2 pagesGrowatt SPF3000TL-HVM (2020)RUNARUNNo ratings yet

- Server LogDocument5 pagesServer LogVlad CiubotariuNo ratings yet

- Ebook The Managers Guide To Effective Feedback by ImpraiseDocument30 pagesEbook The Managers Guide To Effective Feedback by ImpraiseDebarkaChakrabortyNo ratings yet

- Collaboration Live User Manual - 453562037721a - en - US PDFDocument32 pagesCollaboration Live User Manual - 453562037721a - en - US PDFIvan CvasniucNo ratings yet

- AnkitDocument24 pagesAnkitAnkit MalhotraNo ratings yet

- Logistic Regression to Predict Airline Customer Satisfaction (LRCSDocument20 pagesLogistic Regression to Predict Airline Customer Satisfaction (LRCSJenishNo ratings yet

- 2006-07 (Supercupa) AC Milan-FC SevillaDocument24 pages2006-07 (Supercupa) AC Milan-FC SevillavasiliscNo ratings yet

- Biggest Lessons of 20 Years InvestingDocument227 pagesBiggest Lessons of 20 Years InvestingRohi Shetty100% (5)

- Lec - Ray Theory TransmissionDocument27 pagesLec - Ray Theory TransmissionmathewNo ratings yet

- Organisation Study Report On Star PVC PipesDocument16 pagesOrganisation Study Report On Star PVC PipesViswa Keerthi100% (1)

- Dell 1000W UPS Spec SheetDocument1 pageDell 1000W UPS Spec SheetbobNo ratings yet

- BRD TemplateDocument4 pagesBRD TemplateTrang Nguyen0% (1)

- As 1769-1975 Welded Stainless Steel Tubes For Plumbing ApplicationsDocument6 pagesAs 1769-1975 Welded Stainless Steel Tubes For Plumbing ApplicationsSAI Global - APACNo ratings yet

- MSDS Summary: Discover HerbicideDocument6 pagesMSDS Summary: Discover HerbicideMishra KewalNo ratings yet

- Qatar Airways E-ticket Receipt for Travel from Baghdad to AthensDocument1 pageQatar Airways E-ticket Receipt for Travel from Baghdad to Athensمحمد الشريفي mohammed alshareefiNo ratings yet

- Weka Tutorial 2Document50 pagesWeka Tutorial 2Fikri FarisNo ratings yet

- Academy Broadcasting Services Managerial MapDocument1 pageAcademy Broadcasting Services Managerial MapAnthony WinklesonNo ratings yet

- Overall Dimensions and Mounting: Solar Water Pump Controller Mu - G3 Solar Mu - G5 Solar Mu - G7.5 Solar Mu - G10 SolarDocument2 pagesOverall Dimensions and Mounting: Solar Water Pump Controller Mu - G3 Solar Mu - G5 Solar Mu - G7.5 Solar Mu - G10 SolarVishak ThebossNo ratings yet