You might also like

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Financial Management: Liquidity DecisionsDocument10 pagesFinancial Management: Liquidity Decisionsaryanboxer786No ratings yet

- Financial management questions on liquidity decisions, dividend policy, doubling period, present value, operating leverage and financial leverageDocument13 pagesFinancial management questions on liquidity decisions, dividend policy, doubling period, present value, operating leverage and financial leverageSarlaJaiswalNo ratings yet

- Financial ManDocument12 pagesFinancial ManPeenal KumarNo ratings yet

- Financial Management Final Exam Solutions - F19401118 Jocelyn DarmawantyDocument11 pagesFinancial Management Final Exam Solutions - F19401118 Jocelyn DarmawantyJocelynNo ratings yet

- Financial ManagementDocument11 pagesFinancial ManagementMadhusudhan GowdaNo ratings yet

- Model PaperDocument19 pagesModel PaperInovacia CraftsNo ratings yet

- Corporate Finance SummaryDocument17 pagesCorporate Finance SummaryJessyNo ratings yet

- Master of Business Administration-MBA Semester 2 MB0045 - Financial Management - 4 Credits (Book ID: B1134) Assignment Set - 2 (60 Marks)Document13 pagesMaster of Business Administration-MBA Semester 2 MB0045 - Financial Management - 4 Credits (Book ID: B1134) Assignment Set - 2 (60 Marks)Maulik Parekh100% (1)

- Basic Concepts: Scope and Objectives of Financial ManagementDocument31 pagesBasic Concepts: Scope and Objectives of Financial Managementjosh1360No ratings yet

- Corporate Finance 2022 AnswerDocument11 pagesCorporate Finance 2022 AnswerSagar JindalNo ratings yet

- Facebook WhatsApp Acquisition ValuationDocument7 pagesFacebook WhatsApp Acquisition ValuationIcaii InfotechNo ratings yet

- FM II Ch-1Document13 pagesFM II Ch-1tame kibruNo ratings yet

- Financial Management-Mb0045: Assignment SetDocument11 pagesFinancial Management-Mb0045: Assignment SetARIANo ratings yet

- BB0011 Managing Financial Resources Set2Document24 pagesBB0011 Managing Financial Resources Set2prajnaprasadNo ratings yet

- mb0045 FinancialManagementDocument9 pagesmb0045 FinancialManagementSaravanan VelayuthamNo ratings yet

- Unit 7 Capital StructureDocument12 pagesUnit 7 Capital StructurepnkgoudNo ratings yet

- Financial Management Mb0045Document5 pagesFinancial Management Mb0045Anonymous UFaC3TyiNo ratings yet

- Financial Management in 40 CharactersDocument28 pagesFinancial Management in 40 CharactersSimon silaNo ratings yet

- Earnings ManagementDocument7 pagesEarnings ManagementTIONA WAMBA Jospeh HermanNo ratings yet

- Corporate Finance BasicDocument18 pagesCorporate Finance BasicDeep DasguptaNo ratings yet

- SLM Unit 07 Mbf201Document17 pagesSLM Unit 07 Mbf201Pankaj Kumar100% (1)

- LONG TERM INVESTMENT DECISIONS: TIME VALUE OF MONEY (TVM) REPORTDocument7 pagesLONG TERM INVESTMENT DECISIONS: TIME VALUE OF MONEY (TVM) REPORTMary Ann MarianoNo ratings yet

- Rate of Return InflationDocument12 pagesRate of Return InflationShreya SinglaNo ratings yet

- Financial Management Economics For Finance 1679035282Document135 pagesFinancial Management Economics For Finance 1679035282Alaka BelkudeNo ratings yet

- Capital Budgeting: - Vinamra NayakDocument14 pagesCapital Budgeting: - Vinamra NayakhridzenrichingNo ratings yet

- Leverage and Capital Structure AnalysisDocument12 pagesLeverage and Capital Structure AnalysispreetsinghjjjNo ratings yet

- Financial Leverage: Financial Leverage Formula Total Debt / Shareholder's EquityDocument9 pagesFinancial Leverage: Financial Leverage Formula Total Debt / Shareholder's EquityHarihara PuthiranNo ratings yet

- FM FormulasDocument13 pagesFM Formulassudhir.kochhar3530No ratings yet

- Corporate Finance Fundamentals ExplainedDocument26 pagesCorporate Finance Fundamentals ExplainedAkhilesh PanwarNo ratings yet

- Decision Areas in Financial ManagementDocument15 pagesDecision Areas in Financial ManagementSana Moid100% (3)

- Corporate Finance: by Shubha GaneshDocument63 pagesCorporate Finance: by Shubha Ganeshdeepikachandru24No ratings yet

- Classification of Financial Ratios On The Basis of FunctionDocument8 pagesClassification of Financial Ratios On The Basis of FunctionRagav AnNo ratings yet

- Master of Business Administration-MBA Semester 2 MB 0045/MBF 201 - FINANCIAL MANAGEMENT - 4 Credits (Book ID:B1628) Assignment Set - 1 (60 Marks)Document7 pagesMaster of Business Administration-MBA Semester 2 MB 0045/MBF 201 - FINANCIAL MANAGEMENT - 4 Credits (Book ID:B1628) Assignment Set - 1 (60 Marks)Vikas WaliaNo ratings yet

- ENTREPRENEURIAL FINANCE PART 1: TARGETS AND TIME VALUEDocument34 pagesENTREPRENEURIAL FINANCE PART 1: TARGETS AND TIME VALUEMohammed Awwal NdayakoNo ratings yet

- MODULE 5 CAPITAL STRUCTURE AND DIVIDEND DECISIONDocument19 pagesMODULE 5 CAPITAL STRUCTURE AND DIVIDEND DECISIONmuddiniNo ratings yet

- YeahDocument2 pagesYeahMoimen Dalinding UttoNo ratings yet

- Spontaneous FundsDocument5 pagesSpontaneous FundsTobelaNcube100% (2)

- Basic ConceptsDocument7 pagesBasic ConceptsBommana SanjanaNo ratings yet

- Long Term Financial Planning and Growth: Chapter FourDocument21 pagesLong Term Financial Planning and Growth: Chapter FourShourav Roy 1530951030No ratings yet

- B4U2mcs 035Document15 pagesB4U2mcs 035Ts'epo MochekeleNo ratings yet

- Capital Structure and LeverageDocument19 pagesCapital Structure and Leverageemon hossainNo ratings yet

- Leverage AnalysisDocument24 pagesLeverage AnalysisPrateek SharmaNo ratings yet

- Module 6 - EntrepDocument5 pagesModule 6 - EntrepLESLIE ANN ARGUELLESNo ratings yet

- MB0045 - Mba 2 SemDocument19 pagesMB0045 - Mba 2 SemacorneleoNo ratings yet

- Unit VDocument11 pagesUnit VKimberly SalazarNo ratings yet

- Financial Management: Unit III Financing DecisionsDocument19 pagesFinancial Management: Unit III Financing DecisionsSrinivasan KuppusamyNo ratings yet

- Notes For MBA 3Document213 pagesNotes For MBA 3Pramod VasudevNo ratings yet

- Corporate Finance DecisionsDocument17 pagesCorporate Finance DecisionsSahil SharmaNo ratings yet

- FM Intro and Financing Capital BudetingDocument54 pagesFM Intro and Financing Capital BudetingMusangabu EarnestNo ratings yet

- MB20202 Corporate Finance Unit I Study MaterialsDocument17 pagesMB20202 Corporate Finance Unit I Study MaterialsSarath kumar CNo ratings yet

- Interpretation of Financial Statements - Ratio AnalysisDocument10 pagesInterpretation of Financial Statements - Ratio AnalysisDeepalaxmi Bhat100% (1)

- CAPITAL STRUCTURE Risk Management LectureDocument41 pagesCAPITAL STRUCTURE Risk Management LectureJunior LemeNo ratings yet

- Answer 1 - (A)Document7 pagesAnswer 1 - (A)Bhawna TiwariNo ratings yet

- Advanced Financial MGMT Notes 1 To 30Document87 pagesAdvanced Financial MGMT Notes 1 To 30Sangeetha K SNo ratings yet

- FINANCIAL LEVERAGE AND RISKDocument31 pagesFINANCIAL LEVERAGE AND RISKFahadKhanNo ratings yet

- Corporate Finance MBA20022013Document244 pagesCorporate Finance MBA20022013Ibrahim ShareefNo ratings yet

- KWARA STATE UNIVERSITY FINANCIAL STRUCTURE ASSIGNMENTDocument23 pagesKWARA STATE UNIVERSITY FINANCIAL STRUCTURE ASSIGNMENTQUADRI YUSUFNo ratings yet

- An Overview of Financial ManagementDocument46 pagesAn Overview of Financial ManagementKiran IfciNo ratings yet

- Mba105 - Managerial EconomicsDocument2 pagesMba105 - Managerial Economicsaryanboxer786No ratings yet

- Mba105 - Managerial EconomicsDocument2 pagesMba105 - Managerial Economicsaryanboxer786No ratings yet

- What Is A TextureDocument3 pagesWhat Is A Texturearyanboxer786No ratings yet

- Purpose of SkiviingDocument2 pagesPurpose of Skiviingaryanboxer786No ratings yet

- Syllabus For Testing of Footwear Materials & Complete FootwearDocument4 pagesSyllabus For Testing of Footwear Materials & Complete Footweararyanboxer786No ratings yet

- Candidates For Placenment: S.No. Name BatchDocument4 pagesCandidates For Placenment: S.No. Name Batcharyanboxer786No ratings yet

- Avaneesh SainiDocument3 pagesAvaneesh Sainiaryanboxer786No ratings yet

- AmitDocument2 pagesAmitaryanboxer786No ratings yet

- Syllabus For Testing of Footwear Materials & Complete FootwearDocument4 pagesSyllabus For Testing of Footwear Materials & Complete Footweararyanboxer786No ratings yet

- Two Year Diploma Cource In: Msme-Technology Development CenterDocument1 pageTwo Year Diploma Cource In: Msme-Technology Development Centeraryanboxer786No ratings yet

- SurjeetDocument5 pagesSurjeetaryanboxer786No ratings yet

- StructureDocument8 pagesStructurearyanboxer786No ratings yet

- LASTING TameemDocument40 pagesLASTING Tameemaryanboxer786100% (1)

- Inplant EditDocument23 pagesInplant Editaryanboxer786No ratings yet

- Clicking FAQDocument4 pagesClicking FAQaryanboxer786No ratings yet

- Closing FAQDocument5 pagesClosing FAQaryanboxer786No ratings yet

- Name Dipartment Mobile Raw MaterialDocument2 pagesName Dipartment Mobile Raw Materialaryanboxer786No ratings yet

- Lasting FAQDocument4 pagesLasting FAQaryanboxer786100% (1)

- CFTIDocument1 pageCFTIaryanboxer786No ratings yet

- U Lip MutualDocument87 pagesU Lip Mutualaryanboxer786No ratings yet

- 597183Document4 pages597183Tusharr AhujaNo ratings yet

- AbhishekDocument2 pagesAbhishekaryanboxer786No ratings yet

- MB0052 - Strategic Management and Business PolicyDocument6 pagesMB0052 - Strategic Management and Business Policyaryanboxer786No ratings yet

- PDFDocument44 pagesPDFaryanboxer786No ratings yet

- HasanDocument13 pagesHasanaryanboxer786No ratings yet

- MK0013Document7 pagesMK0013aryanboxer786No ratings yet

- CFTIDocument1 pageCFTIaryanboxer786No ratings yet

- MK0010-sales DistributionDocument10 pagesMK0010-sales Distributionaryanboxer786No ratings yet

- Technology Management PDFDocument2 pagesTechnology Management PDFaryanboxer786No ratings yet

- Management Information SystemDocument7 pagesManagement Information Systemaryanboxer786No ratings yet

- Financial Statements-Schedule-III - Companies Act, 2013 PDFDocument13 pagesFinancial Statements-Schedule-III - Companies Act, 2013 PDFCA Ujjwal KumarNo ratings yet

- Assignment Number 4Document8 pagesAssignment Number 4AsadNo ratings yet

- Share CapitalDocument58 pagesShare CapitalCyreene RodelasNo ratings yet

- Karvy Fraud Shivansh - 3438Document7 pagesKarvy Fraud Shivansh - 34383438SHIVANSH AggarwalNo ratings yet

- A Comparative Analysis On Public and Private Mutual FundsDocument72 pagesA Comparative Analysis On Public and Private Mutual FundsMadhuri Tripathi80% (5)

- A. Mwamba Offering 1 PagerDocument1 pageA. Mwamba Offering 1 PagertonybainNo ratings yet

- GAAP Generally Accepted Accounting PrinciplesDocument45 pagesGAAP Generally Accepted Accounting PrinciplesDFW2030100% (1)

- Corporate Accounting Unit 1: Introduction: Mission Vision Core ValuesDocument52 pagesCorporate Accounting Unit 1: Introduction: Mission Vision Core ValuesMudra JainNo ratings yet

- NTPC Group crosses 3GW renewable energy capacity; FuelBuddy partners with IOCLDocument3 pagesNTPC Group crosses 3GW renewable energy capacity; FuelBuddy partners with IOCLLikhitha YerraNo ratings yet

- Performance of Mutual Fund Schemes in IndiaDocument8 pagesPerformance of Mutual Fund Schemes in IndiaPankaj GuravNo ratings yet

- DNO-SEODocument4 pagesDNO-SEOShakerMahmood0% (1)

- Mrss Outperforms 261Document16 pagesMrss Outperforms 261SiaNo ratings yet

- True / False Questions: Foreign Exchange RiskDocument44 pagesTrue / False Questions: Foreign Exchange Risklatifa hnNo ratings yet

- Exercise Answers - AcquisitionDocument26 pagesExercise Answers - AcquisitionJohn Philip L Concepcion100% (1)

- Nifty Weightage Understanding Its Significance in The Indian Stock MarketDocument23 pagesNifty Weightage Understanding Its Significance in The Indian Stock Marketmahedihasan141997No ratings yet

- BD Bank Balance Sheet AnalysisDocument46 pagesBD Bank Balance Sheet AnalysisSaiful Islam JewelNo ratings yet

- Investment Appraisal: Client: C. J. Chapman Password: Robin664 Investment Grade: Private Institutional Pages: 2Document2 pagesInvestment Appraisal: Client: C. J. Chapman Password: Robin664 Investment Grade: Private Institutional Pages: 2Leslie SargentNo ratings yet

- Outsource Partners InternationalDocument95 pagesOutsource Partners Internationalbharat100% (1)

- L1R41 - Annotated - LiveDocument52 pagesL1R41 - Annotated - LiveAlex PaulNo ratings yet

- Operating Leverage - A Framework For Anticipating Changes in Earnings PDFDocument26 pagesOperating Leverage - A Framework For Anticipating Changes in Earnings PDFScott JNo ratings yet

- Advac2 MidtermDocument5 pagesAdvac2 MidtermgeminailnaNo ratings yet

- Creditrisk Credit SuisseDocument92 pagesCreditrisk Credit SuisseAdarsh Kumar50% (6)

- Tether Gold WhitepaperDocument15 pagesTether Gold WhitepaperРуслан НовиковNo ratings yet

- MacKinlay - 1997 - Event Studies in Economics and FinanceDocument28 pagesMacKinlay - 1997 - Event Studies in Economics and FinanceGokulNo ratings yet

- Due - Diligence ChecklistDocument4 pagesDue - Diligence ChecklistAndrew D. WalcottNo ratings yet

- Assigment Mba-4 SEM Financial Derivatives (Kmbfm05) UNIT-1Document19 pagesAssigment Mba-4 SEM Financial Derivatives (Kmbfm05) UNIT-1Shalini ShekharNo ratings yet

- Deal Anlysis - Ultratch Cement - Jaypee GroupDocument29 pagesDeal Anlysis - Ultratch Cement - Jaypee GroupMukesh tiwariNo ratings yet

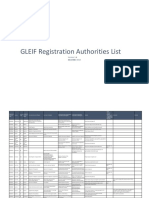

- GLEIF Registration Authorities List: 4 December 2018Document33 pagesGLEIF Registration Authorities List: 4 December 2018fhrjhaqobNo ratings yet

- Solution Manual For Accounting Information Systems 13th Edition Romney SteinbartDocument10 pagesSolution Manual For Accounting Information Systems 13th Edition Romney SteinbartErick Febrianto (Youtubers Cilik)No ratings yet

- UnionBank 2018 Annual Report Highlights Key DevelopmentsDocument295 pagesUnionBank 2018 Annual Report Highlights Key Developmentsnancy delos santosNo ratings yet

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)